- Carrier surcharges, cargo front-loading support market outlook

- Shippers accelerate cargo flows ahead of US tariff changes in July

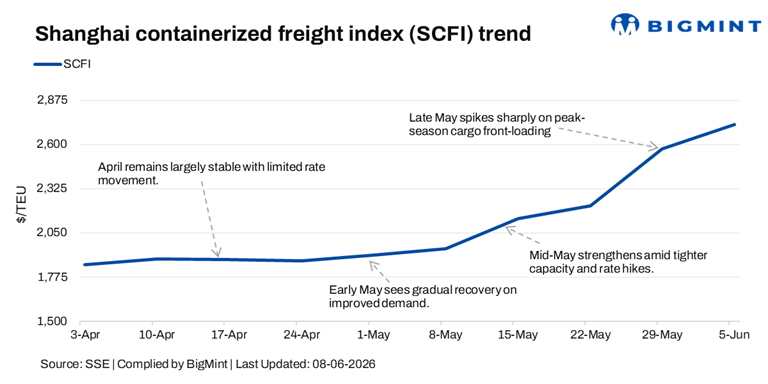

The Shanghai Containerized Freight Index (SCFI) surged 6% w-o-w to $2,726.5/twenty-foot equivalent unit (TEU) on 5 June 2026, extending its bullish momentum as freights increased across major East-West trade lanes.

The market was supported by an earlier-than-usual peak season, with shippers accelerating cargo movements ahead of potential US tariff changes in July and upcoming bunker fuel adjustments effective 1 July.

Strong booking activity enabled carriers to successfully implement higher freight all kinds (FAK) rates and peak season surcharges (PSS), resulting in notable rate increases on both Asia-Europe and Trans-Pacific routes.

Capacity tightness supports rates

Container market sentiment remained firmly positive as higher bunker prices, geopolitical tensions in the Middle East, and ongoing Red Sea disruptions continued to support freights. Longer transit times and elevated operating costs have tightened available capacity.

Despite improving freight fundamentals, market participants remain cautious over evolving geopolitical developments, fuel price volatility, and potential shifts in trade policies, which could influence cargo flows in the coming months.

Trade Lane-wise Sentiments

Outlook

BigMint expects the SCFI to remain on an upward trajectory in the coming week, supported by ongoing peak-season demand, further carrier surcharge implementation, and continued cargo frontloading across major East-West trade routes.

Looking ahead, additional PSS announcements, bunker adjustment-related shipment acceleration, and persistent geopolitical disruptions are also expected to maintain upward pressure on freight rates. While vessel capacity remains adequate overall, extended voyage routings and elevated operating costs are likely to keep market fundamentals firm in the near term.

Leave a Reply