- BDI eases marginally as Capesize rates remain under pressure

- Smaller bulk carriers exhibit resilience amid balanced market conditions

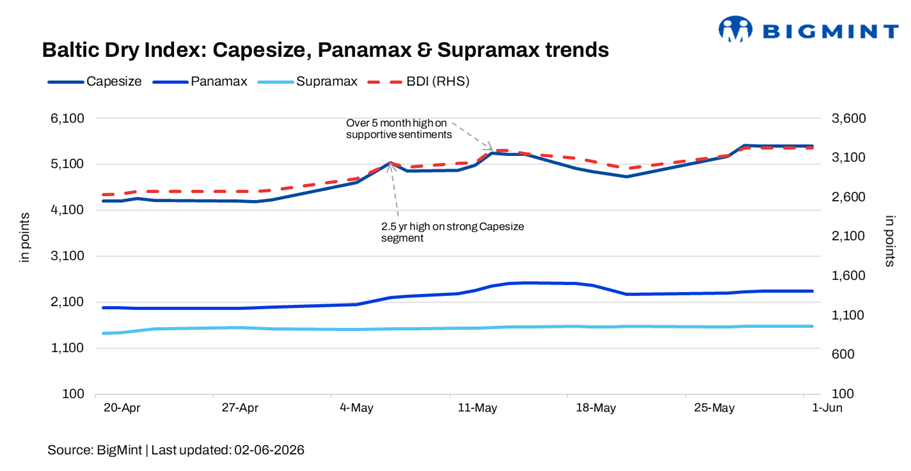

The Baltic Exchange’s Dry Bulk Index (BDI) edged down marginally by 0.06% (2 points) to 3,222 points on 1 June 2026 against 29 May, indicating a largely stable dry bulk market with mixed sentiment across vessel segments.

Segment-wise trends

- Capesize: The Capesize index declined by 0.13% (7 points) to 5,496 points, reflecting a slightly softer sentiment amid cautious chartering activity and easing momentum in key iron ore trades.

- Panamax: The Panamax index increased by 0.04% (1 point) to 2,344 points, indicating a stable-to-firm sentiment supported by steady grain and coal cargo movements.

- Supramax: The Supramax index rose by 0.06% (1 point) to 1,570 points, suggesting a marginally positive sentiment as regional cargo enquiries provided limited support despite abundant vessel availability.

Freight Sentiment

Capesize freight sentiment remained cautiously weak, with rates experiencing slight pressure due to balanced vessel supply and demand conditions. While iron ore shipments continued to support the market, limited fresh fixtures and restrained chartering activity prevented stronger rate gains.

Smaller segment freight sentiment was stable with a mild positive bias, supported by gradual improvement in regional cargo enquiries. However, ample tonnage availability and slow fixture finalizations continued to cap significant upside in freight rates.

Outlook

The Baltic index is expected to remain mixed in the near term. Capesize rates may continue to face pressure unless fresh iron ore demand emerges, while Panamax and Supramax segments are likely to remain relatively stable, supported by steady agricultural and minor bulk cargo movements.

Overall market direction will depend on cargo volumes, vessel supply dynamics, and commodity trade flows in the coming weeks.

Leave a Reply