- Strong regional demand continues to drive bullish momentum

- Indonesian export reform uncertainty encourages forward buying

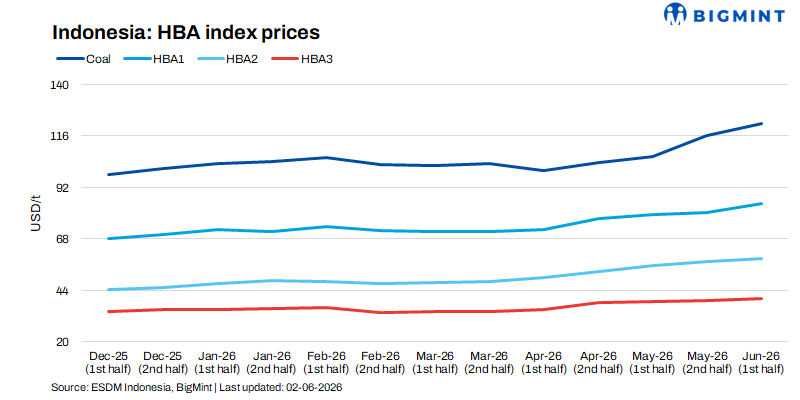

Indonesia’s Harga Batubara Acuan (HBA) thermal coal benchmarks recorded broad-based gains across all calorific value (CV) categories during the first half of June 2026, supported by tightening spot availability, resilient regional demand, and growing procurement activity from utilities and industrial consumers across Asia.

The continued upward trajectory in benchmark prices reflects improving market sentiment, firm replacement costs, and increasing concerns over future coal availability amid evolving Indonesian export regulations.

High-CV coal segment strengthens on supply tightness

The benchmark HBA price for 6,322 kcal/kg GAR coal increased by nearly 5% to $121.83/t in H1 of June from the second half of May, reaching its highest level in nearly a year. The rise was supported by tight spot availability, steady utility demand, elevated replacement costs, and continued procurement activity amid concerns over future supply availability.

Mid-CV coal hits record high on strong utility demand

The HBA-I benchmark (5,300 kcal/kg GAR) rose by around 5% to $84.53/t, reaching a record high since its introduction. The increase was driven by strong demand from utilities and industrial consumers seeking a cost-effective balance between fuel efficiency and procurement costs, making mid-CV coal an attractive alternative to higher-CV grades amid rising energy expenses.

Lower-CV coal segments continue to outperform

The HBA-II benchmark (4,100 kcal/kg GAR) rose by 2% to $58.81/t, while the HBA-III benchmark (3,400 kcal/kg GAR) increased by 2.5% to $40.32/t, with both indices reaching record highs. The gains were driven by robust demand across South and Southeast Asia, where lower-CV coal remains a cost-effective fuel option for power generation and industrial consumption. Strong affordability, ample blending opportunities, and sustained buying interest from price-sensitive consumers continued to support the upward momentum.

Export reform uncertainty supports market sentiment

Market sentiment has been further supported by Indonesia’s proposed coal export reforms, which aim to centralise export activities through State-Owned Enterprises (BUMN) from 1 January 2027. Under the proposed framework, private miners will no longer be permitted to export coal directly, with all export-related processes to be managed through designated BUMN entities. While the policy is not expected to affect near-term coal availability, concerns over potential implementation challenges and future export procedures have prompted buyers to secure volumes in advance, lending additional support to prices.

Key market drivers

Several factors continue to support the strength of Indonesian thermal coal prices:

- Tight spot coal availability across key Indonesian producing regions.

- Firm demand from utilities and industrial consumers across Asia.

- Rising replacement costs due to higher international coal indices and freight rates.

- Strong preference for lower-CV coal driven by affordability and fuel cost optimisation.

- Growing uncertainty surrounding Indonesia’s upcoming coal export framework and its potential implications for trade flows.

Outlook

Indonesian thermal coal prices are expected to remain supported by tight supply, steady demand, and pre-emptive buying ahead of export reforms. Lower- and mid-CV grades are likely to remain resilient, while policy uncertainty may provide additional support to market sentiment. However, future price trends will depend on demand, export availability, freight costs, and regulatory clarity.

Leave a Reply