- Firm global coke and coal prices support the market

- Cautious domestic demand limits price gains

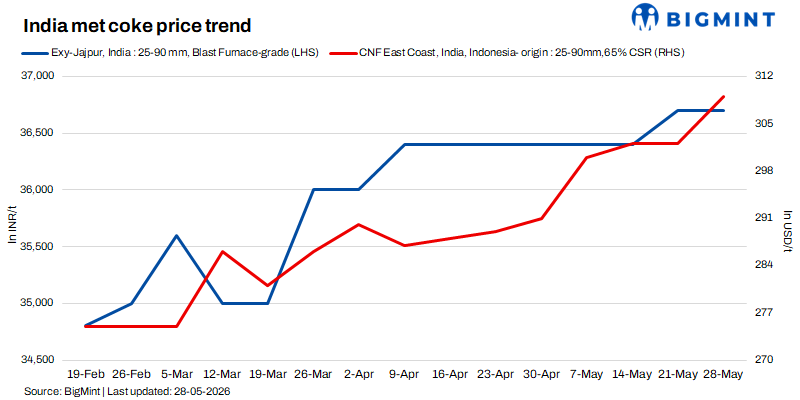

The met coke market witnessed improved sentiment in the week ended 28 May, underpinned by rising international coke prices. As per BigMint’s assessment of Indonesian-origin BF-grade coke (65/63 CSR) was assessed at approximately $309/t CFR India, up by $7/t w-o-w.

The increase was primarily driven by firmer FOB offers from Indonesian suppliers, higher freight rates, and strengthening sentiment across the global coking coal value chain.

Trade sources reported the booking of two vessels totaling around 55,000 tonnes at $275-276/t FOB Indonesia, with one cargo reportedly earmarked for the Indian market. Market participants also indicated that Indonesian producers have raised their offer levels to around $290/t FOB for end-July to August shipments.

The upward revision in offers follows tightening coking coal fundamentals after recent mining disruptions in China and sustained firmness in global metallurgical coal prices, which have elevated production costs and strengthened seller confidence.

Domestic coke prices remain stable amid balanced market fundamentals

Despite the rise in international prices, India’s domestic blast furnace (BF)-grade metallurgical coke market remained largely stable as of 28 May 2026. Balanced supply-demand conditions, comfortable inventory levels, and steady material availability across major consumption centres helped maintain price stability during the week.

In the eastern region, BF-grade coke prices were unchanged at INR 36,700/t ex-Jajpur, while prices in western India remained steady at INR 33,500/t ex-Gandhidham. The stability reflects consistent trade activity and the absence of any major supply-side disruptions.

Similarly, foundry-grade (+90 mm) coke prices were assessed unchanged at INR 36,400/t ex-Rajkot, supported by stable procurement from the casting and foundry sector. Overall, adequate domestic availability and cautious buying interest continued to offset the bullish cues emerging from the international market.

Firm coking coal market continues to provide cost support

The global coking coal market remained resilient, providing sustained cost support to coke producers. Australian premium hard coking coal (PHCC) prices remained stable at $241/t FOB Australia as of 28 May 2026.

In China, coking coal prices maintained a firm trajectory, supported by production disruptions, stricter mine safety inspections, and ongoing supply constraints in major mining regions such as Shanxi and Shaanxi. Demand-side fundamentals also remained supportive, with stable coke plant operations, low raw material inventories, and high blast furnace utilization rates encouraging steady procurement activity. Expectations of further coke price increases in China continue to underpin bullish sentiment across the metallurgical coke value chain.

Pig iron market reflects cautious downstream buying

While steel production levels remain largely stable, downstream buying sentiment in the pig iron market showed signs of caution. Steel-grade pig iron prices in Durgapur declined marginally by INR 350/t w-o-w to INR 38,100/t ex-works.

This softer sentiment was further reflected in SAIL Rourkela’s latest auction, where only 1,600 tonnes out of the offered 5,000 tonnes were booked at an average price of INR 37,550/t ex-works. The auction witnessed a decline of INR 200/t compared to the previous sale on 21 May, when 4,500 tonnes were successfully booked at INR 37,750/t ex-works. The lower booking volume and softer bids indicate buyers’ cautious stance amid uncertain steel market margins and adequate inventory positions.

Outlook

Indian met coke prices are likely to remain firm, supported by rising global coke prices and strong coking coal costs. However, ample domestic supply, competitive imports, and cautious downstream demand may limit significant price increases. Market direction will depend on developments in China, import costs, and steel sector demand.

Leave a Reply