- Eid holidays and LC constraints continued restricting fresh imported scrap buying activity

- Stable domestic feedstock availability kept Bangladesh mills cautious on imported scrap bookings

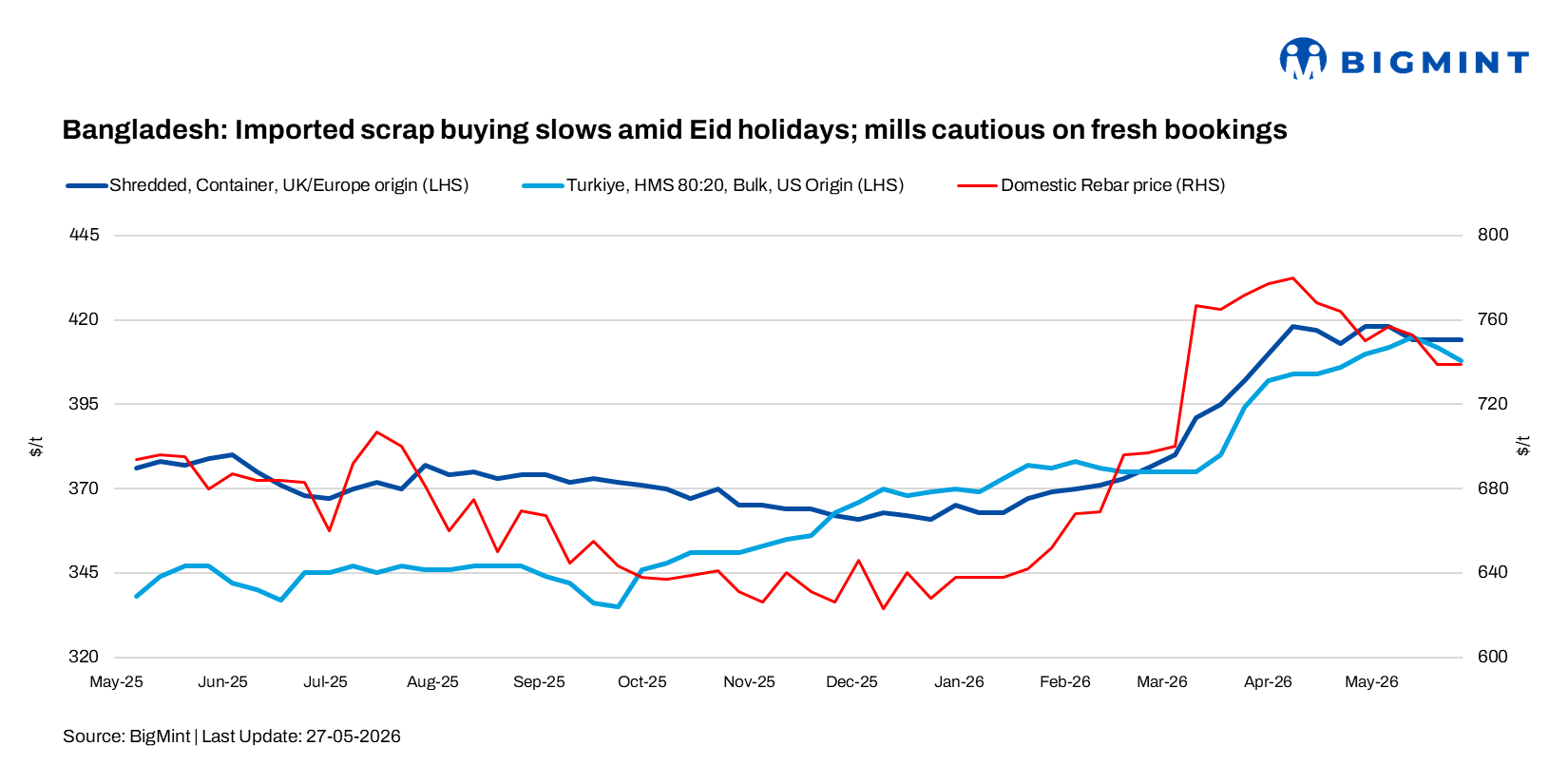

Imported ferrous scrap trading activity in Bangladesh remained subdued this week as market participants stayed cautious ahead of Eid holidays, while mills continued limiting fresh deep-sea bookings due to weak margins and tighter liquidity conditions.

Containerised shredded scrap offers were heard around $410/t CFR, while HMS offers were indicated near $385/t CFR. PNS scrap offers were reported within $400-405/t CFR Chattogram.

According to market participants, overall trading activity across both Bangladesh and Pakistan remained extremely slow amid the ongoing Eid holidays, with buyers largely refraining from aggressive import bookings.

A Dhaka-based mill source commented, “We haven’t purchased much imported scrap recently due to LC constraints, while our margins have become thinner because of rising production costs.”

Domestic steel market conditions remained relatively stable. Rebar prices in Dhaka were heard within BDT 82,000-84,000/t ($668-684/t) and in Chattogram at BDT 88,000-92,000/t ($717-750/t), while local scrap prices were reported near BDT 48,000-49,000/t ($391-399/t).

Industry sources noted that local mills continued operating smoothly with stable steel production, supported mainly by regular sponge iron and ferro-alloy supplies arriving from West Bengal. Domestic shipbreaking activity also remained active, helping maintain local scrap availability and reducing immediate dependence on imported material.

Market sentiment remained largely neutral-to-positive, although buyers continued adopting a cautious approach towards imported scrap procurement amid geopolitical uncertainties, currency pressure, and freight volatility.

Outlook

Imported scrap buying activity in Bangladesh is expected to remain slow in the coming days due to Eid holidays, cautious mill margins, and ongoing LC limitations. However, stable domestic steel production, active shipbreaking operations, and regular regional feedstock inflows are likely to continue supporting local raw material availability.

Leave a Reply