- Export centralisation raises supply uncertainty

- Lower quotas tighten export availability

Indonesia’s proposed coal export agency is increasingly emerging as one of the most consequential – and least understood – risks to seaborne thermal coal markets. While much of the debate has focused on whether the new state-controlled mechanism will function efficiently, the more important question may be different: does it even need to fail to disrupt trade?

The answer is likely no.

Indonesia’s plan to centralise commodity exports through a new state-controlled platform, Danantara Sumber Daya, has introduced fresh uncertainty into a market already grappling with Chinese mine safety inspections, geopolitical disruptions and tightening prompt supply. Even if implemented smoothly, the transition itself risks creating delays, contracting hesitation and operational friction across one of the world’s most important thermal coal supply chains.

The scale of what Indonesia is attempting

Coal buyers and producers are awaiting implementation details expected over the coming weeks, but the policy direction already marks a structural shift in how Indonesian coal reaches global markets.

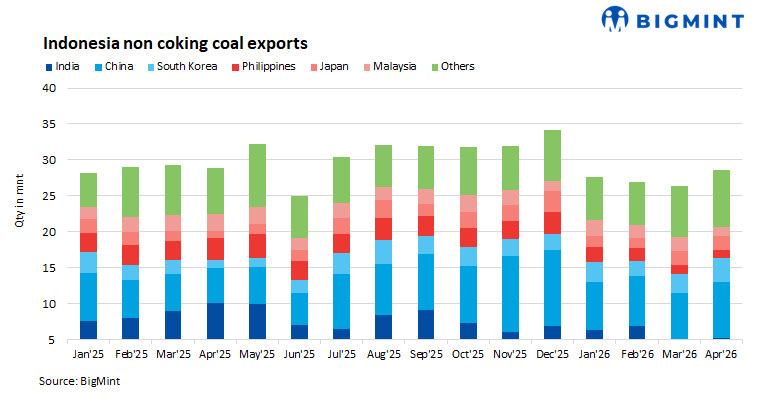

Historically, Indonesian coal exports have operated through a fragmented ecosystem involving miners, traders, barging operators, surveyors, vessel schedulers and end-users across Asia. The proposed framework would centralise a much larger portion of export administration under state oversight.

The challenge lies not merely in governance – but in scale and timing.

Indonesia’s state-linked coal company PT Bukit Asam (PTBA) historically handled only a relatively small share of the country’s coal movement. The new framework, however, could potentially oversee a much larger share of export activity at a time when Indonesia is simultaneously attempting to restrain coal production.

Production caps could make disruption more meaningful

The agency is not emerging in isolation.

Indonesia is simultaneously pursuing tighter control over coal production through lower output quotas in 2026. If production is held near 600 mnt, while domestic market obligation (DMO) requirements absorb roughly 250 mnt, export availability may be closer to 350 mnt, significantly lower than historical levels.

This changes the market equation materially.

The issue is no longer simply who signs export documentation. The bigger concern is whether a smaller exportable coal pool is now being routed through a more centralised approval and logistics framework. For buyers in India, China and Southeast Asia, that combination raises the risk of delayed cargoes, lower optionality and greater competition for prompt Indonesian tonnes.

Why disruption may occur even if the agency functions well

The market’s initial reaction has framed the issue too narrowly: either the agency works or it fails.

But coal markets are vulnerable not only to outright disruption, but also to uncertainty.

The mere existence of a new export approval structure can alter buyer behaviour, slow contract negotiations and complicate supply planning – particularly for utilities and industrial consumers dependent on stable Indonesian supply.

Three channels of disruption are already visible.

International buyers entering medium- or long-term contracts now face questions around cargo allocation, documentation, payment channels and scheduling certainty. Even without outright supply loss, hesitation alone could temporarily tighten prompt cargo availability.

The policy contradiction markets are struggling to understand

Part of the market’s discomfort stems from inconsistent policy logic.

The Indonesian government has linked tighter commodity oversight to concerns over export revenue leakage and under-invoicing. Yet oil and gas exports have reportedly been exempted in order to preserve “investment certainty”, while coal has not.

For market participants, this raises an obvious question: if investment certainty matters for hydrocarbons, why should coal be treated differently?

Coal procurement depends heavily on predictability. Even modest disruptions in documentation, cargo nominations, payment processing or scheduling can translate into demurrage costs, replacement fuel purchases and procurement uncertainty for utilities.

Why this matters for global thermal coal

Indonesia remains the dominant supplier of low- and medium-calorific value thermal coal, particularly 3,400-4,200 GAR material, to key importers including India, China and Southeast Asia.

Any slowdown in contracting activity or export movement could tighten prompt supply availability, especially because exportable tonnes may already be lower under a stricter production regime.

That creates an opening for competing exporters.

Russian coal may increasingly benefit as buyers seek alternatives to Indonesian policy uncertainty, while Australian coal could regain market share despite a premium, particularly among buyers prioritising reliability over outright price.

What the market should watch

Three questions will likely determine whether this becomes a manageable transition or a structural supply risk:

- Will existing offtake contracts be grandfathered?

- Will the agency function as an administrative clearing platform or a commercial trading body?

- Can vessel scheduling, payments and cargo documentation transition without delays?

The answers will shape procurement behaviour through the second half of 2026.

The state of play

Coal markets are accustomed to disruptions from floods, mine accidents and geopolitics. Indonesia’s proposed export overhaul presents a different type of challenge – one rooted in administration, execution and uncertainty.

Unlike a flood or export ban, the disruption here may be gradual and difficult to measure. But that may also make it more persistent.

BigMint assessment: Indonesia’s export transition does not need to fail to tighten coal markets. A smaller exportable pool combined with greater administrative centralisation could increase friction across the seaborne market, supporting thermal coal prices and shifting buyer preference toward supply certainty rather than simply lowest cost.

Leave a Reply