- Firm overseas offers pressure Indian import buyers

- Casting-grade tense scrap availability remains tight

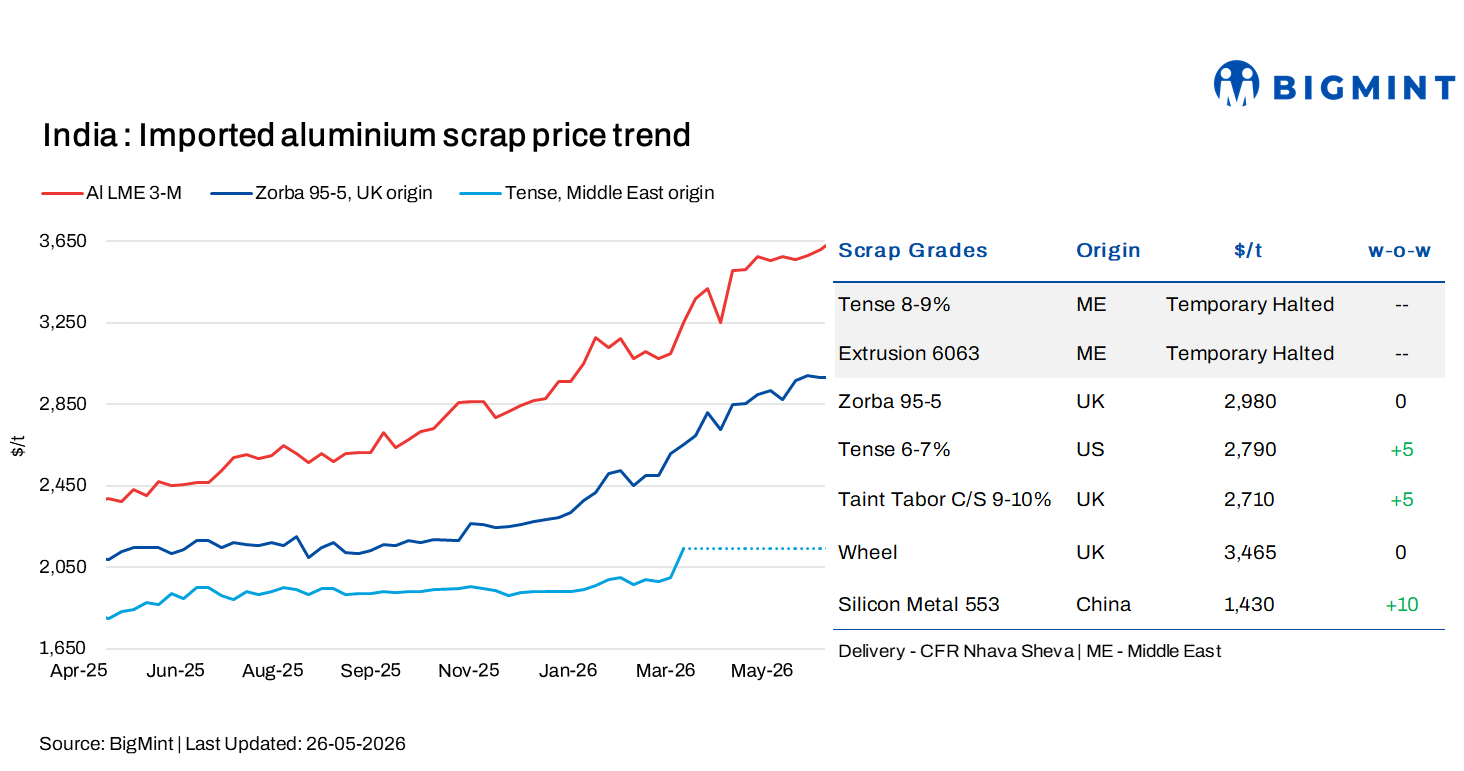

India’s imported aluminium scrap prices remained largely stable w-o-w as of 26 May 2026, despite higher London Metal Exchange (LME) aluminium prices and continued tightness in global scrap supply.

According to BigMint’s latest assessment for CFR Nhava Sheva deliveries, UK-origin zorba 95-5 scrap declined by $10/t w-o-w to $2,980/t from $2,990/t previously.

Meanwhile, US-origin tense 6-7% scrap increased by $5/t w-o-w to $2,790/t from $2,785/t last week.

LME aluminium rises w-o-w

Three-month aluminium prices on the London Metal Exchange (LME) traded higher w-o-w, closing at $3,656/t on 26 May 2026 against $3,612/t on 19 May 2026, up by $44/t.

LME aluminium prices remained firm w-o-w amid tightening ex-China supply conditions and continued inventory drawdowns, while concerns over Middle East trade disruptions and Strait of Hormuz navigation supported market sentiment.

Market sentiment improved following reports of a potential US-Iran ceasefire framework and 30-day negotiations, although hawkish US Fed commentary and a stronger dollar capped broader base metal gains.

Meanwhile, LME aluminium inventories declined by 1,100 t w-o-w to 339,475 t from 340,575 t over the same period.

Market scenario

Indian secondary aluminium buyers continued to face pressure from elevated scrap prices during the week, while deals, particularly from the US, remained subdued due to the Memorial Day long weekend. Although trading activity slowed, scrap prices continued to stay firm amid persistent supply tightness and ongoing logistical challenges.

Market participants noted that overseas suppliers largely maintained firm offers due to constrained availability, making imported material increasingly less competitive for Indian buyers. At the same time, resistance is gradually building among downstream consumers in India’s secondary aluminium and die-casting sectors, where rising raw material costs are becoming difficult to pass through.

Scrap remains expensive and demand continues to stay healthy, but buyers are turning cautious at higher price levels. Market participants indicated that any further increase in scrap prices could begin impacting alloy demand and squeezing margins across the value chain.

Import arrivals into India have also remained limited in recent weeks due to uncompetitive offers and elevated freight costs. Secondary alloy producers continue to grapple with tight raw material availability alongside rising logistics expenses, further pressuring production economics.

Supply conditions remain constrained globally, while freight continues to be a major concern for import dependent buyers.

On the domestic front, aluminium prices remained firm w-o-w, while scrap availability continued to stay tight across northern and southern India, particularly for casting-grade tense scrap amid ongoing supply constraints.

Chinese silicon prices

According to BigMint’s latest assessment, China-origin silicon metal 553 prices increased by $10/t w-o-w to $1,430/t on a CFR Mundra basis as of 26 May 2026, compared with $1,420/t last week, supported by relatively firm import offers and improved market sentiment.

Outlook

India’s imported aluminium scrap market is expected to remain firm in the near term amid tightening global scrap availability, elevated LME aluminium prices, constrained import arrivals, and continued freight challenges. Buyers are likely to remain cautious at higher price levels, while limited overseas supply may continue supporting firm import offers.

Leave a Reply