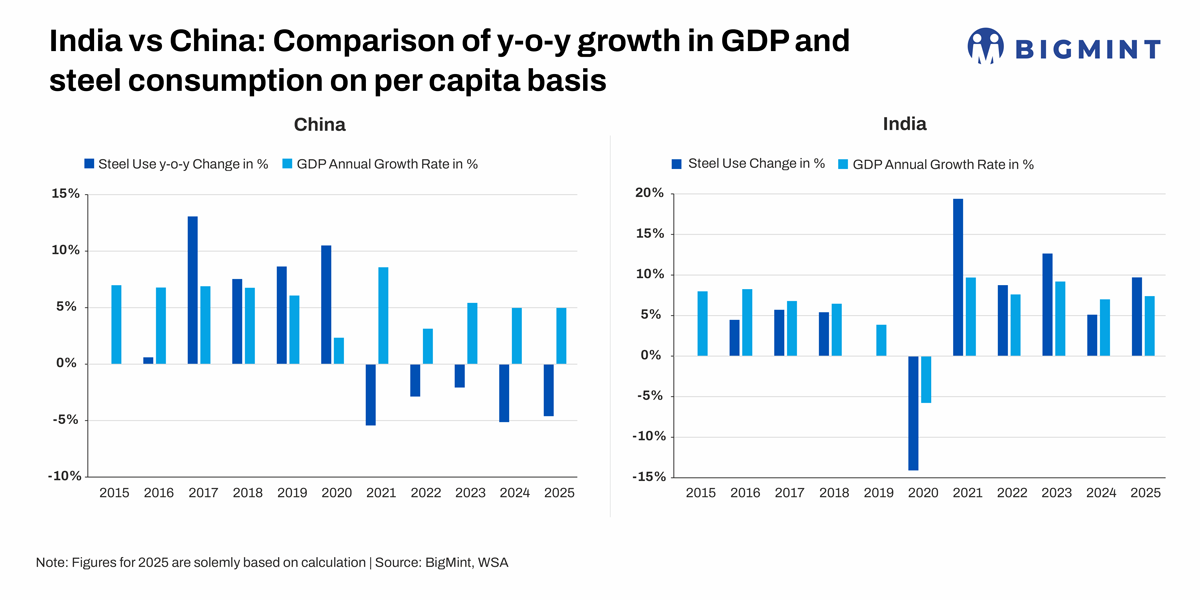

- Indian, Chinese per capita GDP rates surge by 70% over 2015-25

- India’s per capita steel use rises 69% from 2015, China’s up only 20%

Data Deep Dive: For decades, China defined the global steel supercycle. Now, as Chinese steel demand slows after years of infrastructure and property-led expansion, attention is shifting to India as the next potential engine of global steel demand growth.

With India now the world’s second-largest crude steel producer and among the fastest-growing major economies, its steel sector is increasingly being viewed through the same lens once applied to China during the early 2000s. The question now is whether India can drive a global steel supercycle similar to the one China fuelled during its peak industrial expansion.

Similar economic foundations support India-China comparisons

In terms of economic profiles, India and China had broadly similar trajectories during the 1990s, with per capita gross domestic product (GDP) at around $300. However, China’s economic reforms in the 1980s, centred on industrialisation, exports, manufacturing, and infrastructure, accelerated growth sharply over the next few decades, lifting per capita GDP to nearly $14,000 by 2025.

India liberalised its economy later and followed a slower, services-led expansion path. As a result, its per capita GDP stood at around $2,675 in 2025. Yet the pace of growth between India and China has narrowed considerably over the past decade. Between 2015 and 2025, both countries recorded GDP growth of roughly 71%.

India’s crude steel production is also accelerating rapidly, reaching China’s pace. Since 2000, China’s crude steel production has increased at a compound annual growth rate (CAGR) of 11.2% to 1,065 mnt in 2020. Similarly, in the past five years, India’s crude steel production has recorded a CAGR of 10.5%.

Moreover, India currently has a population of comparable scale to China, a large infrastructure deficit, and ambitions to expand manufacturing under initiatives such as Make in India. The presence of several such similarities makes comparisons with China reasonable.

India’s trajectory also differs from developed economies where steel demand has largely decoupled from GDP growth. In countries such as the US, Japan, Germany, and France, further economic growth no longer significantly increases steel consumption because infrastructure and industrial capacity are already mature. India, however, is still in an infrastructure build-out phase where economic growth directly supports steel demand expansion.

India’s steel demand has substantial room to grow

India is currently in the middle of a prolonged infrastructure and industrial expansion cycle. Public capital expenditure has increased sharply from INR 2 lakh crore in FY’15 to a budgeted INR 12.2 lakh crore in FY’27, driven by spending on roads, railways, housing, and renewable energy and urban infrastructure.

As a result, India’s per capita steel consumption increased by 69% between 2015 and 2025 to 113 kg. However, despite this growth, India remains significantly underpenetrated in steel consumption. Even if the country achieves its National Steel Policy target of 160 kg per capita consumption by 2030-31, it would still remain below the 2024 global average of 215 kg.

To illustrate, China’s per capita steel consumption stood around five times higher, at 600 kg in 2025, despite consumption slowing significantly following the 2020 real estate downturn. India’s 2030-31 consumption will also be much lower than the US’s 275 kg, Japan’s 440 kg, South Korea’s 901 kg, Italy’s 420 kg, etc. in 2025. This indicates significant long-term headroom for India’s demand growth.

Infrastructure, public investment to boost steel demand

India’s steel demand growth is closely linked to infrastructure and investment activity. Infrastructure and construction account for roughly 60-70% of domestic steel demand, making public investment a major demand driver.

India has also entered a more investment-intensive growth phase post-pandemic. In terms of percentage of GDP, gross fixed capital formation has remained around 30-31% of GDP during 2021-2024, according to World Bank data. This is above the global average of roughly 26% and significantly higher than the US and EU at around 22%. However, it still remains below China’s 38-42% during 2003-2024.

This gap partly explains why India’s steel intensity remains lower than China’s. A smaller share of economic output is still being channelled into fixed asset creation and industrial capacity expansion.

But China’s steel supercycle was faster, more concentrated

Between 2000 and 2020, China’s share of global steel demand increased from roughly 18% to more than 50%, reshaping global commodity and raw material markets.

This is because China’s steel demand growth between 2000 and 2020 was faster and more expansive in scale than anything seen before. Massive urban migration, debt-driven property expansion, export manufacturing, and state-led infrastructure investment pushed per capita steel consumption above 500-600 kg during the peak years.

However, China’s growth model became increasingly dependent on debt and real estate. Building construction accounted for 42% share of steel demand by 2011, while local government financing vehicles supported large-scale infrastructure spending.

As the property bubble burst in 2020, steel demand plateaued despite continued GDP growth. This indicates that China has passed its peak steel intensity phase, with Wood Mackenzie forecasting that its share in global steel demand is set to fall from 49% in 2024 to 31% by 2050.

Will India be able to drive the next steel supercycle?

If India maintains a 9-10% CAGR from 2025, crude steel production could theoretically exceed one billion tonnes before 2050. However, one billion tonnes seems excessively ambitious considering that the government had earlier specified a target of achieving 500 mnt of steel production capacity by 2047.

India’s growth trajectory is unlikely to replicate China’s exactly. China’s steel boom was fuelled by extremely high investment intensity, rapid urbanisation, and debt-funded property expansion, the latter of which ultimately turned unsustainable. India’s model is more fiscally constrained and consumption-led.

India’s infrastructure expansion, by contrast, remains gradual and constrained by bureaucratic red tape, land acquisition challenges, and slower project execution. Additionally, India’s manufacturing share of GDP at 13-16% over 2014-2024 also remains below China’s over 30% during 2005-2014, though this has steadily receded since then to 25% in 2024.

Moreover, China’s much faster urbanisation rate — averaging 7.3% growth per decade against India’s 2.7% — supported stronger growth in steel-intensive sectors such as infrastructure, housing and manufacturing. World Bank data also shows that India’s urban population reached 37% of the total in 2024 versus China’s 66%.

In India, manufacturing growth is still uneven, logistics and energy costs remain high, and steel demand continues to depend heavily on public capex. India also remains reliant on imported coking coal, exposing producers to volatility in global raw material markets.

Additionally, global demand conditions are weaker today than during China’s rise. China industrialised during peak globalisation, when export markets expanded rapidly and Western economies absorbed massive volumes of manufactured goods. India faces a slower and more protectionist world.

Decarbonisation constraints are also far tighter now. China built much of its steel base before emissions became central to industrial policy. India will need to scale while simultaneously reducing carbon intensity, which increases capital requirements.

Therefore, India can become the world’s largest source of incremental steel demand growth over the next two decades. However, China will probably remain the largest steel producer globally for many years because its installed capacity base is enormous. Nonetheless, future net additions to global steel demand are increasingly expected to come from India as Chinese consumption stabilises or declines.

This transition is already visible in global industry strategy. Iron ore miners, metallurgical coal suppliers, equipment manufacturers, and steel technology providers are increasingly positioning India as the primary long-term growth market because China’s expansion cycle has largely peaked.

BIFW 2026

How will India’s GDP growth shape its steel demand trajectory by 2030? How will the decoupling of China’s steel consumption from its GDP growth impact global steel consumption and trade? Tap into these insights and more at BigMint India Ferrous Week, to be held over 19-21 August at JW Marriott, Kolkata.

Leave a Reply