- Domestic scrap demand thin, major grades witness limited trades

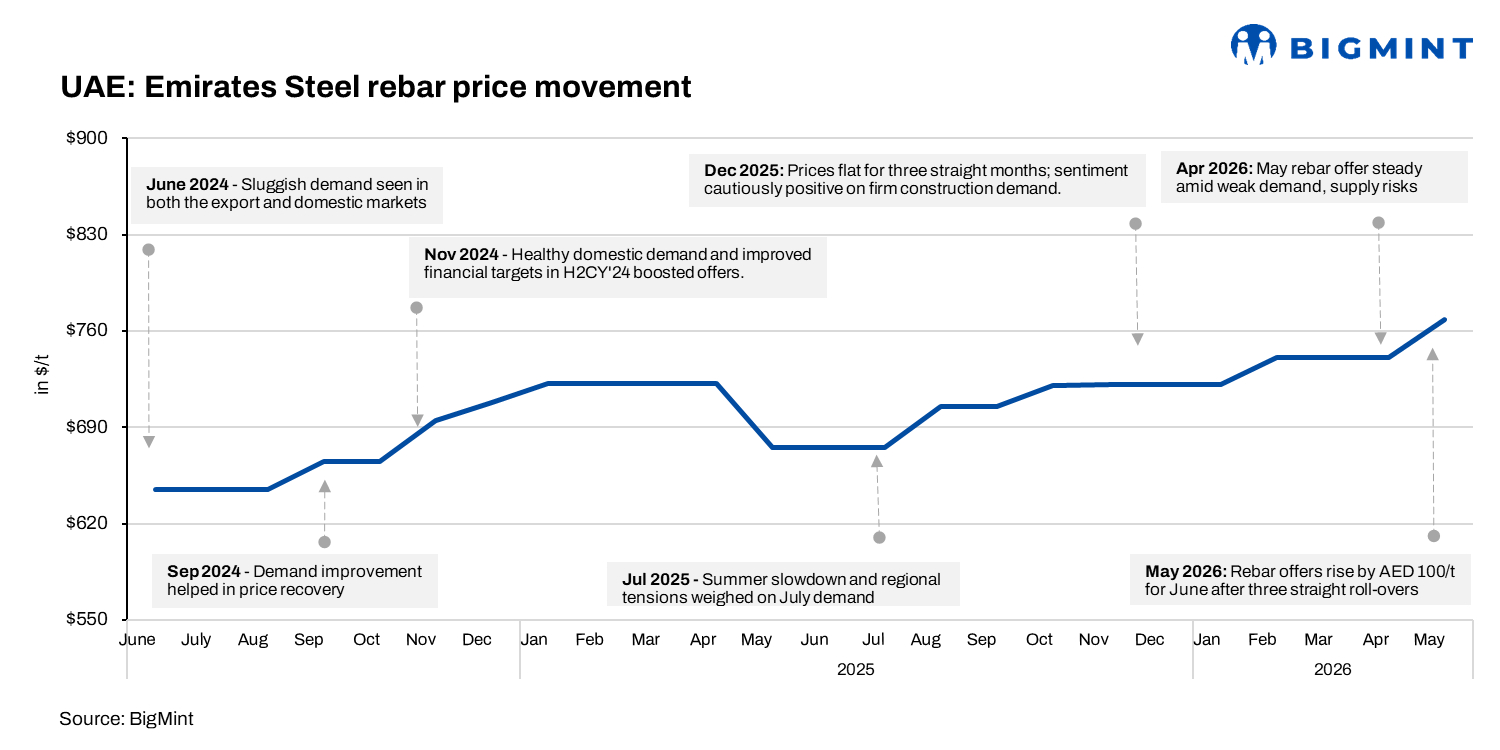

- EMSTEEL lifts June rebar prices after three consecutive roll-overs

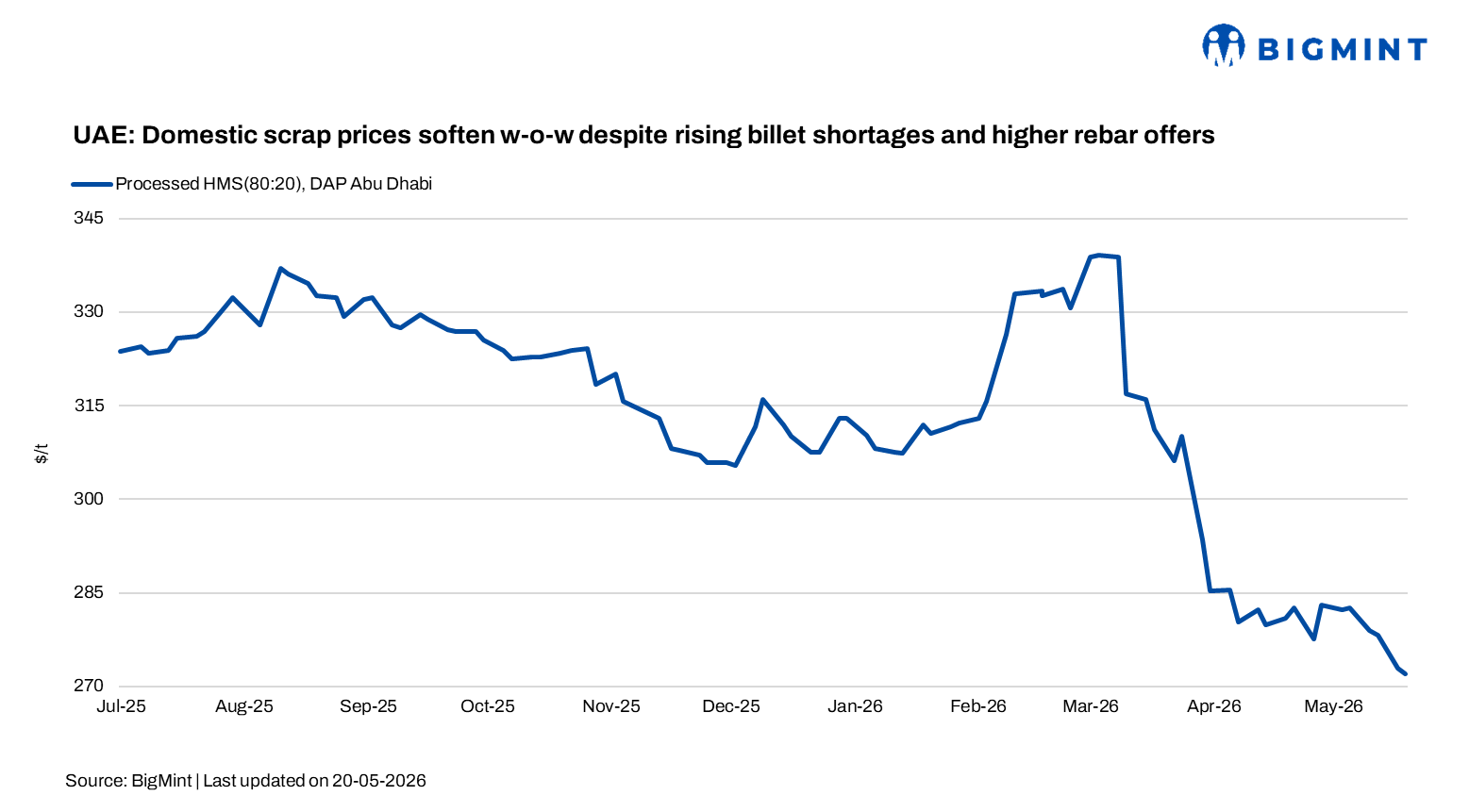

The UAE domestic scrap market remained soft in the week ending on 22 May as slow demand from major mills continued to weigh on fresh trades. On the other hand, elevated freight costs, and ongoing logistics disruptions continued to support finished steel prices across the Gulf region.

BigMint assessed HMS (80:20) processed at AED 1,000/t ($272/t) DAP Abu Dhabi, down sharply by AED 22/t ($6/t) w-o-w.

Processed HMS scrap was heard at AED 1,000-1,010/t ($270-273/t), while unprocessed PNS scrap stood at AED 1,000-1,020/t ($270-275/t). HMS 1 traded at AED 960-970/t ($259-262/t), HMS Super at AED 950-970/t ($257-262/t), and HMS (80:20) at AED 900-920/t ($243-248/t) DAP. LMS scrap remained lower at AED 750-770/t ($203-208/t).

Processed PNS and shredded scrap was heard at around AED 1,050/t ($284/t) DAP Abu Dhabi, while processed HMS traded at AED 1,000/t ($270/t). In the broader market, fabrication scrap traded at AED 1,050-1,100/t ($284-297/t) depending on quality and size, while HMS shredded scrap indications stood at AED 1,050-1,075/t ($284-290/t) DAP.

Market participants said processed and higher-grade scrap continues to command premiums as mills prioritise cleaner feedstock amid tight regional supply conditions and elevated replacement costs.

Billet shortages tighten regional steel supply

The UAE billet market also remained under pressure as regional supply chains continued to face disruption amid geopolitical uncertainty in the Middle East. Billet offers into the UAE were heard at around $530-550/t CFR depending on origin and logistics availability. However, traders said sourcing options remain limited due to ECAS certification requirements and freight-related disruptions.

An Indian billet cargo booked earlier by a UAE buyer was reportedly redirected to another GCC destination due to certification-related complications.

Market participants said mills and traders are increasingly focused on securing inventories amid uncertainty surrounding future arrivals and logistics stability. “We are trying to keep inventories high because nobody knows how long the Strait of Hormuz disruption will continue,” a Gulf market participant said.

Sources added that many UAE re-rollers continue to struggle to secure enough billet for June rolling schedules. “Most mills do not have enough billet for rolling,” a Gulf-based industry insider said.

Truck shortages across the GCC continue to delay cargo movements from Fujairah and Sohar ports into the UAE, while Omani ports are reportedly prioritising domestic industrial cargoes over regional steel shipments.

EMSTEEL raises June rebar prices

Against this backdrop, EMSTEEL increased its June domestic rebar prices by over AED 100/t ($27/t) after maintaining stable levels between March and May. The producer’s latest rebar offers are now at AED 2,821/t ($768/t) exw under 90-day LC terms, while additional discounts of around AED 65-75/t ($18-20/t) are reportedly available for large-volume buyers.

Market participants linked the increase to tightening billet availability, rising freight costs, and ongoing supply chain disruptions across the GCC, although the latest hike was still viewed as lower than earlier market expectations.

Market participants linked the increase to tightening billet availability, rising freight costs, and ongoing supply chain disruptions across the GCC, although the latest hike was still viewed as lower than earlier market expectations.

Outlook

The UAE steel and scrap market is expected to remain firm in the coming weeks as billet shortages, elevated freight costs, and logistics disruptions continue to pressure regional supply chains. However, cautious construction demand may continue to limit aggressive price increases despite tightening market fundamentals.

Leave a Reply