- Requirement-based procurement by buyers

- Bid-offer disparity widened further

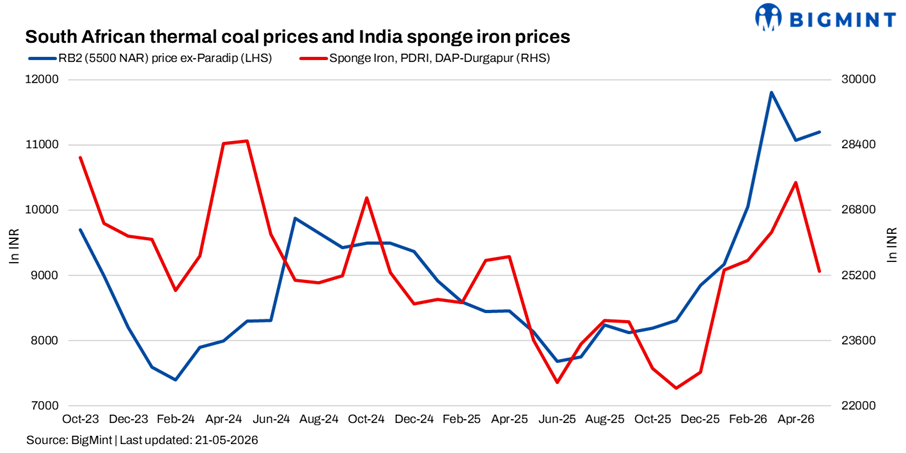

South African thermal coal sentiment at Indian ports remained subdued during the week ended 21 May as weak sponge iron demand, comfortable domestic coal availability pressuring imported coal trade. Although global coal indices and freight rates stayed firm, actual market activity remained extremely slow with very limited enquiries and widening bid-offer disparities across portside markets.

As per BigMint’s assessment, ex-Paradip RB2 (5,500 NAR) prices increased marginally by INR 100/t w-o-w to INR 11,400/t, while RB3 (4,800 NAR) prices also rose INR 100/t to around INR 9,800/t. However, participants stated that these price levels were largely non-workable for many buyers due to weak downstream steel and sponge iron economics.

Market participants indicated that FOB trade activity remained almost inactive amid elevated index levels and weak Indian buying interest. Offers for South African 5,500 NAR coal were heard around $96-97/t FOB, while 4,800 NAR cargoes were discussed near $77/t FOB. However, traders stated that actual buying interest remained negligible, particularly from central India markets.

Participants also noted that freight sentiment remained elevated despite slow physical activity. Freight from RBCT to Vizag for a 30,000 t cargo was heard around $23/t including DA charges, while Panamax freight levels were indicated near $24/t. Rising bunker prices continued supporting freight costs, further widening the gap between South African landed costs and Indian workable market levels.

Weak sponge iron market pressures coal demand

The sponge iron market continued remaining under pressure during the week despite a marginal improvement in trading volumes compared with previous subdued sessions. PDRI DAP-Durgapur prices declined sharply by INR 900/t w-o-w to INR 23,950/t amid cautious market sentiment.

Participants stated that procurement activity largely remained on immediate requirement-based, with sponge plants increasingly shifting towards domestic coal due to cheaper pricing and comfortable availability. Buyers continued avoiding aggressive imported coal purchases amid poor downstream visibility and expectations of subdued demand over the weeks.

Several traders stated that imported coal movement remained extremely slow at ports, with lower-priced cargoes witnessing selective movement while higher-priced material faced resistance. A trader deal for RB2 coal around INR 10,900/t ex-Mangalore was heard during the week, although participants noted that fresh replacement costs remained significantly higher due to shortage of quality RB2 cargoes at the port.

In addition to that increased crude oil prices started reflecting in the domestic market, logistics is the main concerned at portside, which has added cost.

Domestic coal prices decline further

Domestic coal continued exerting strong pressure on imported South African cargoes. BigMint assessed domestic 5,000 GCV coal prices lower by around INR 500/t w-o-w, while 4,500 GCV material declined around INR 200/t to nearly INR 4,100/t as on 19 May 2026.

At the same time, India’s thermal coal inventories at major ports declined 4.5% w-o-w in Week 20 to 15.16 mnt from 15.87 mnt in Week 19, indicating improved evacuation across key ports. However, overall inventory levels remained elevated and continued limiting urgency for fresh import bookings.

Market participants indicated that unless sponge iron and steel demand improve meaningfully, imported South African coal trade is likely to remain slow with buyers continuing cautious, requirement-based procurement strategies.

Outlook

South African coal sentiment is expected to remain subdued in the near term as weak sponge iron demand, and reasonable domestic coal availability. Although higher freight costs and firm FOB offers may continue supporting higher landed cost. Buyers are likely to maintain cautious approach, due to weak downstream steel margins and limited market visibility.

Leave a Reply