- Indonesia delays royalty hike amid logistics disruptions

- Philippine ore supply rebounds after rainy season

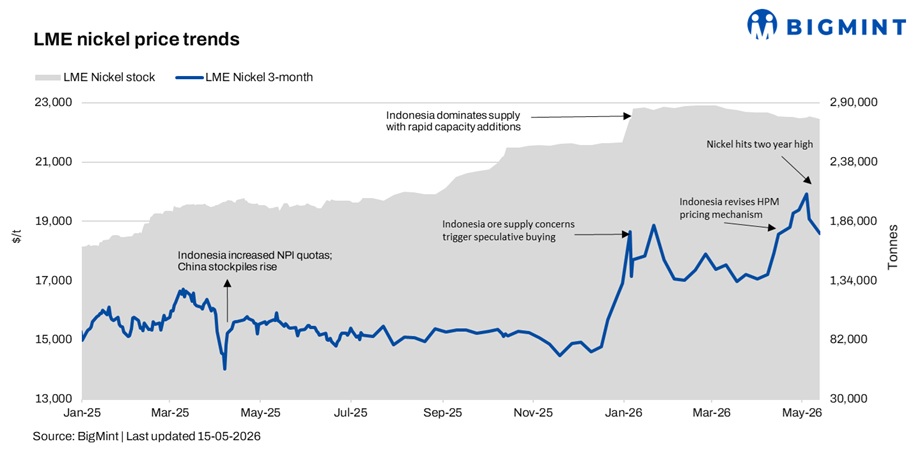

London Metal Exchange (LME) nickel futures declined by 2.6% w-o-w during the week ended 15 May, following the recent sharp rally, with the three-month nickel contract closing at $18,580/t, down from $19,385/t. Meanwhile, LME warehouse inventories remained broadly stable at 275,778 t compared with 277,788 t last week, indicating relatively balanced exchange stock levels.

Market sentiment weakened during the week after Indonesia’s Ministry of Mines postponed its proposed increase in mineral royalties and export tariffs. The move partially reversed earlier bullish expectations linked to higher export taxes and rising Indonesian nickel production costs.

Philippine ore supply improves post-rainy season

At the same time, improving nickel ore supply from the Philippines added further pressure to prices. Market participants noted that the end of the rainy season in the Philippines has significantly improved mining activity and ore shipments, leading to softer ore prices and reduced cost support for nickel pig iron (NPI) producers.

Macro uncertainty weakens commodity sentiment

Macroeconomic sentiment also remained cautious. Ongoing US-Iran negotiations showed little progress, while stronger-than-expected US economic data reduced expectations of near-term interest rate cuts by the US Federal Reserve, pushing rate cut expectations further towards 2027 and weighing on broader commodity markets.

Flooding disrupts Indonesia’s nickel ore logistics

Indonesia’s nickel sector also continued to face operational challenges after heavy rainfall and flooding in Southeast Sulawesi disrupted key nickel ore transportation routes near Kendari. Although NPI smelter operations remained largely unaffected, damaged roads and logistical congestion slowed ore movement, tightening short-term raw material flows to smelters.

Rising sulphur prices increase processing costs

Meanwhile, rising sulphur prices following continued disruption in the Strait of Hormuz have increased additional cost pressure on Indonesia’s nickel industry, which relies heavily on Gulf sulphur imports for nickel processing operations.

Supply chain disruptions and tightening raw material availability are gradually reshaping expectations for the global nickel market, with some market participants increasingly expecting slower Indonesian output growth and a potential shift towards tighter global nickel balances by 2026.

Outlook

The global nickel market is expected to remain volatile in the near term as participants monitor Indonesian policy developments, Philippine ore supply recovery, geopolitical risks, and macroeconomic trends. While easing ore supply may pressure prices in the short term, logistical disruptions and rising processing costs could continue to provide underlying support to the market.

Leave a Reply