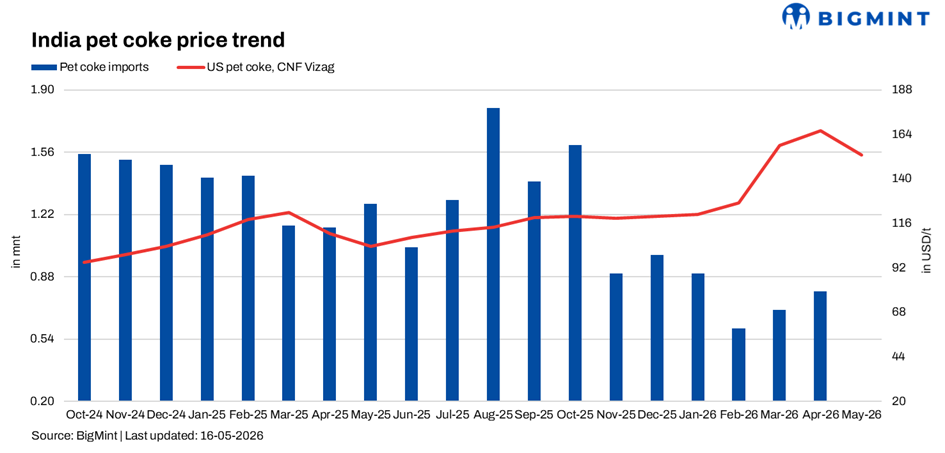

- High-sulphur petcoke prices into India fall for 3rd consecutive week

- Weaker cement demand, price drop expectations keep buyers away

Global fuel-grade petroleum coke (petcoke) prices continued to soften this week, with mid- and high-sulphur grades under pressure as buyers in key importing markets, particularly India and Turkiye, increasingly turned to thermal coal as a cheaper alternative.

Despite a decline in seaborne petcoke prices, Indian cement makers remained reluctant buyers, citing a wide price gap with coal, weaker cement market conditions, and expectations of further price corrections.

Global petcoke prices soften across major markets

Fuel-grade petcoke prices weakened across most key regions, particularly for high-sulphur grades used in cement manufacturing.

High-sulphur petcoke prices into India have now declined for a third consecutive week, reflecting weaker buying appetite and increasing competition from thermal coal.

India: Coal continues to displace petcoke

India remains the key swing market for fuel-grade petcoke, but current procurement patterns suggest cement producers are continuing to shift away from imported coke in favour of coal.

Market checks with Indian cement buyers indicate little urgency to purchase imported petcoke despite lower offers.

A leading cement producer indicated that buying activity remains muted because of ample fuel coverage and competitive domestic sourcing opportunities. Another buyer noted that the market continues to wait for lower domestic petcoke prices before returning to imports.

Several buyers also reported weak cement demand conditions and lower kiln fuel requirements, reducing immediate procurement urgency.

Indicative market feedback from 15 May suggested imported petcoke levels around $145-150/t CFR, with some buyers indicating limited willingness to purchase even at these levels because of better coal economics.

One southern India cement producer indicated there remains a “huge gap” between coal and petcoke pricing, keeping the company away from the market. Another large buyer said it continues to consume petcoke inventory accumulated during December-January rather than purchasing fresh cargoes.

US NAPP coal remains the preferred alternative

The biggest challenge for petcoke demand in India continues to be competition from high-calorific-value US Northern Appalachian (NAPP) coal, alongside Russian and domestic coal.

Offers for US NAPP 6,900 NAR coal into India’s west coast were heard in the low-to-mid $130s/t CFR range, materially below imported petcoke prices. Traders holding prompt cargoes at Indian ports were reportedly willing to discuss even lower levels for quick placement.

At current price levels, many cement buyers view coal as more economical, particularly after adjusting for duties and operational flexibility.

Market participants said buyers are increasingly preferring US NAPP coal for high-CV kiln requirements, Russian coal where competitively priced, and domestic Indian coal, particularly given rupee-denominated pricing and plentiful availability ahead of the monsoon.

One buyer said there were currently “no buyers for petcoke”, with most market participants focused on coal because of abundant availability and expectations of softer fuel demand during the monsoon period.

Middle East supply disruptions offer limited support

Supply disruptions in the Middle East continue to provide some underlying support to petcoke markets.

Cargo availability from Saudi Arabia’s Satorp refinery remains constrained due to disruptions to shipping through the Strait of Hormuz, while lower refinery runs at some facilities have also reduced output. At the same time, stocks of Saudi-origin 8.5% sulphur petcoke have reportedly been building in some locations because of logistical bottlenecks.

In India, market participants reported discussions around Saudi and Oman-origin cargoes at $140-143/t CFR, although confirmed deal activity remained limited.

Still, supply-side tightness has so far failed to offset the demand weakness caused by coal competition.

Outlook

BigMint expects petcoke prices to soften further in coming weeks, particularly if US Gulf Coast values continue to decline and demand remains weak.

However, the key determinant for India’s buying appetite is likely to remain the spread between petcoke and coal.

Unless imported petcoke becomes materially more competitive relative to US NAPP coal and domestic coal, cement makers are expected to continue limiting purchases and rely on coal-heavy fuel mixes through the monsoon period.

For now, the imported petcoke market appears to be in a wait-and-watch phase, with sellers lowering offers but buyers remaining reluctant to return in meaningful volumes.

Leave a Reply