- Prices tumble as steel demand weakens sharply

- Rebar prices decrease by INR 1,700/t w-o-w

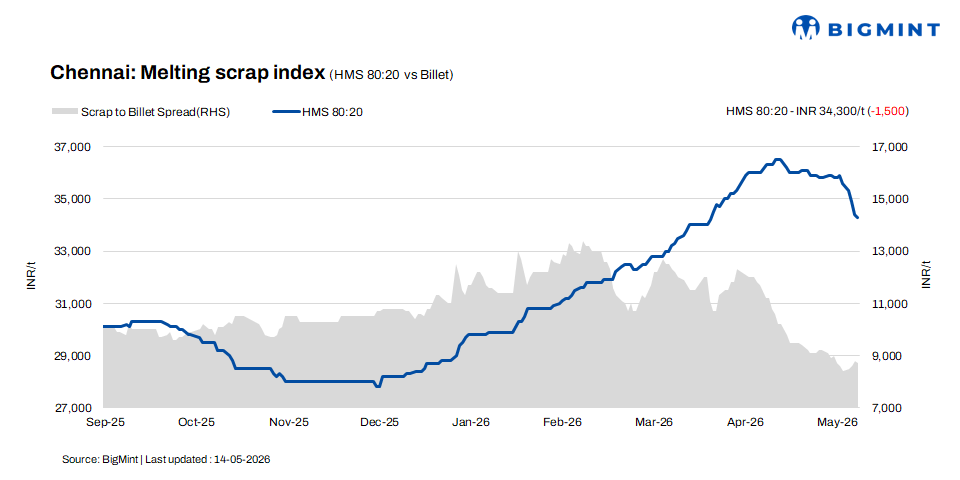

According to BigMint’s latest assessment, HMS (80:20) scrap prices in Chennai declined sharply by INR 1,500/t w-o-w to INR 34,400/t, while fell by INR 100/t on a daily basis. In the semi-finished segment, billet prices dropped by INR 200/t d-o-d to INR 43,000/t, registering a weekly decline of INR 1,500/t, reflecting weak market sentiment.

Similarly, in the finished steel segment, rebar prices fell by INR 1,700/t w-o-w to INR 49,500/t, with a further daily decline of INR 200/t. The sharp correction across steel and scrap segments indicates subdued demand, cautious buying activity, and increasing pressure on market prices.

Imported and domestic price trends

Market participants reported that Australia-origin shredded scrap was offered at $390-395/t CFR Chennai, while HMS (80:20) was quoted at $370-375/t CFR. Despite the ongoing shortage of scrap in the domestic market, buying interest for imported material remained limited.

Market sources indicated that higher dollar rates have increased the landed cost of imported scrap, making domestic scrap offers comparatively more cost-effective for buyers. As a result, mills are showing limited interest in fresh import bookings and are continuing to rely largely on domestic procurement to meet near-term requirements.

In the domestic market, HMS (80:20) scrap prices were quoted at INR 34,000-34,500/t for spot deals with immediate payment. Meanwhile, transactions on extended credit terms were concluded at higher levels of INR 34,500-35,000/t.

Overall, trading activity remained largely concentrated within the INR 34,000-35,000/t range, with price variations mainly influenced by payment terms and mill-specific volume requirements. Market participants continued to follow a cautious procurement approach, while transactions were largely need-based amid fluctuating steel demand conditions.

Buyer-supplier sentiments

According to a mill source, sponge iron merchant sellers are continuously lowering their offer prices, although buyers are still reluctant to procure material amid weak sentiment. Meanwhile, billet demand remains sluggish, pressured by slow finished steel demand in the market.

Additionally, integrated mills have started offering billets in the market, adding further supply pressure amid weaker consumption trends. On the rebar side, demand remains poor due to the peak summer season and slower construction activity. As a result, mills are currently maintaining around 40% higher inventory than their regular stock levels, indicating sluggish material movement and cautious buying sentiment.

A market participant noted that HMS (80:20) scrap prices are currently ranging between INR 34,000-35,000/t, depending on payment terms and procurement volumes. Labour shortages caused by extreme summer weather continue to disrupt scrap processing operations, resulting in limited material availability in the market. On the demand side, the ongoing decline in billet and rebar prices has forced buyers to push for lower scrap procurement rates to maintain conversion costs and operating margins.

Regional comparison

In the western India based Jalna market, billet prices inched up by INR 100/t to INR 42,500/t. Meanwhile, rebar prices remained stable at INR 47,700/t, while HMS (80:20) scrap prices were unchanged at INR 34,500/t.

Market participants noted that rebar demand has weakened over the past couple of weeks, leading to price corrections in the finished steel segment. However, despite softer steel demand, a mild shortage of scrap continues to persist in the market, supporting firmer scrap procurement prices by mills in recent days. The limited availability of scrap has helped maintain stability in raw material pricing despite weak downstream demand.

Outlook

The Chennai scrap market is likely to witness a stable-to-slightly soft trend, as subdued finished steel demand continues to pressure sentiment. At the same time, limited domestic scrap availability and lower imported scrap bookings are expected to support prices. Overall, price fluctuations are expected within the INR +/- 200-500/t range.

Leave a Reply