- Ample domestic supply, cheaper sponge iron cap Indian demand

- Bangladesh remains slow amid liquidity challenges, high freights

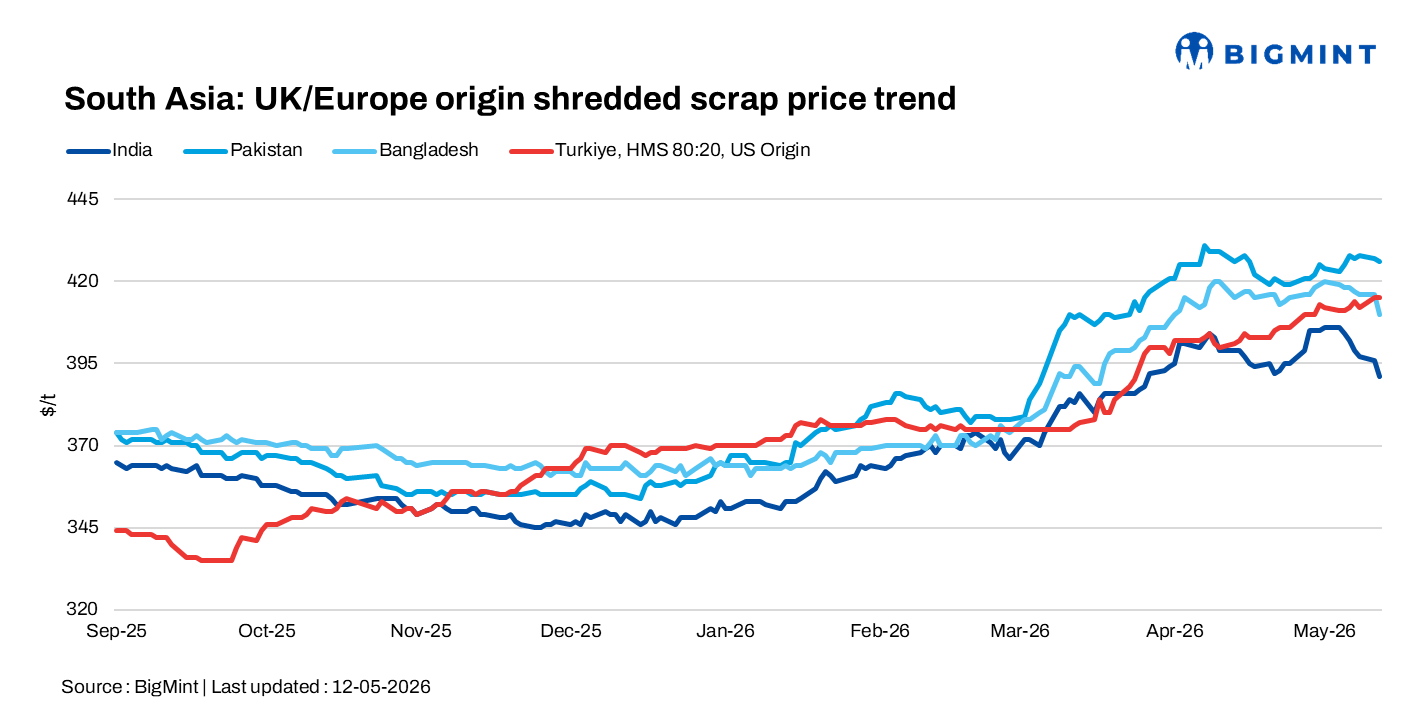

South Asian imported scrap markets remained largely weak d-o-d on 12 May 2026. Sentiment was weighed down by currency volatility, weak finished steel demand, tight liquidity conditions, elevated freight costs, and cautious mill buying, resulting in limited fresh bookings and subdued trading activity overall.

India: The imported containerised scrap market remained weak d-o-d, pressured by sharp INR depreciation and widening import parity. Domestic scrap availability and cheaper sponge iron continued to reduce import appetite.

The USD/INR exchange rate was near 95.90, further weakening buyer sentiment. UK/EU-origin HMS 80:20 offers were at around $360/t CFR, while shredded scrap saw negligible interest due to currency pressure.

Indicative Australian offers to Chennai were HMS 80:20 at $370-372/t, HMS 90:10 at $380-382/t, shredded at $390-392/t, and PNS at $400-402/t CFR. Freight rates from Melbourne remained high at $1,450-1,500/20ft.

Pakistan: The imported scrap market remained slow d-o-d, with weak finished steel demand and cautious sentiment keeping buyers inactive. Shredded scrap offers were heard at $428-435/t CFR Qasim, while bids stayed lower at $420-423/t CFR. Tradable levels were near $425/t CFR, with a UK-origin cargo reportedly concluded around $420/t CFR.

Local steel prices remained stable, with rebar at PKR 250,000-251,000/t ($897-901/t) and billet at PKR 215,000-218,000/t($772-783/t). Local scrap was heard at PKR 153,000-154,000/t ($549-553/t), while bala stood at PKR 192,000-200,000/t ($689-718/t).

Market activity remained subdued, with sales at 45-50% and capacity utilisation at 35-40%.

Bangladesh: Imported scrap market remained slow d-o-d due to weak steel demand, liquidity constraints, and letter of credit (LC)/payment delays. UK/EU-origin HMS 80:20 offers were heard at $385-390/t CFR, with no major trades concluded.

Indicative prices were as follows: HMS 80:20 at $384-385/t, HMS 90:10 at $392-395/t, shredded at $400-405/t, and PNS at $410-415/t CFR. Buyers preferred hand-loaded cargoes and US/Brazil/Africa-origin material due to quality preferences.

Some exporters shifted focus to Indonesia and Thailand, where shredded was around $390/t, HMS 90:10 at $375/t, and HMS 80:20 at $365/t CFR. High freight costs continued to limit imports.

Turkiye: The deep-sea imported scrap market remained stable d-o-d, but trading activity stayed limited due to weak rebar demand and squeezed mill margins. HMS 80:20 was assessed at $415/t CFR, unchanged d-o-d, with US and Northern EU-origin cargoes heard at $410-410/t CFR.

Mills remained cautious, buying on a hand-to-mouth basis amid weaker rebar prices and rising input costs. Limited cargo availability further restricted activity. Freight costs stayed high, while export rebar prices remained steady at $590/t FOB.

Leave a Reply