- Need-based procurement continues at elevated prices

- Supply pressure emerges after late-week stock increase

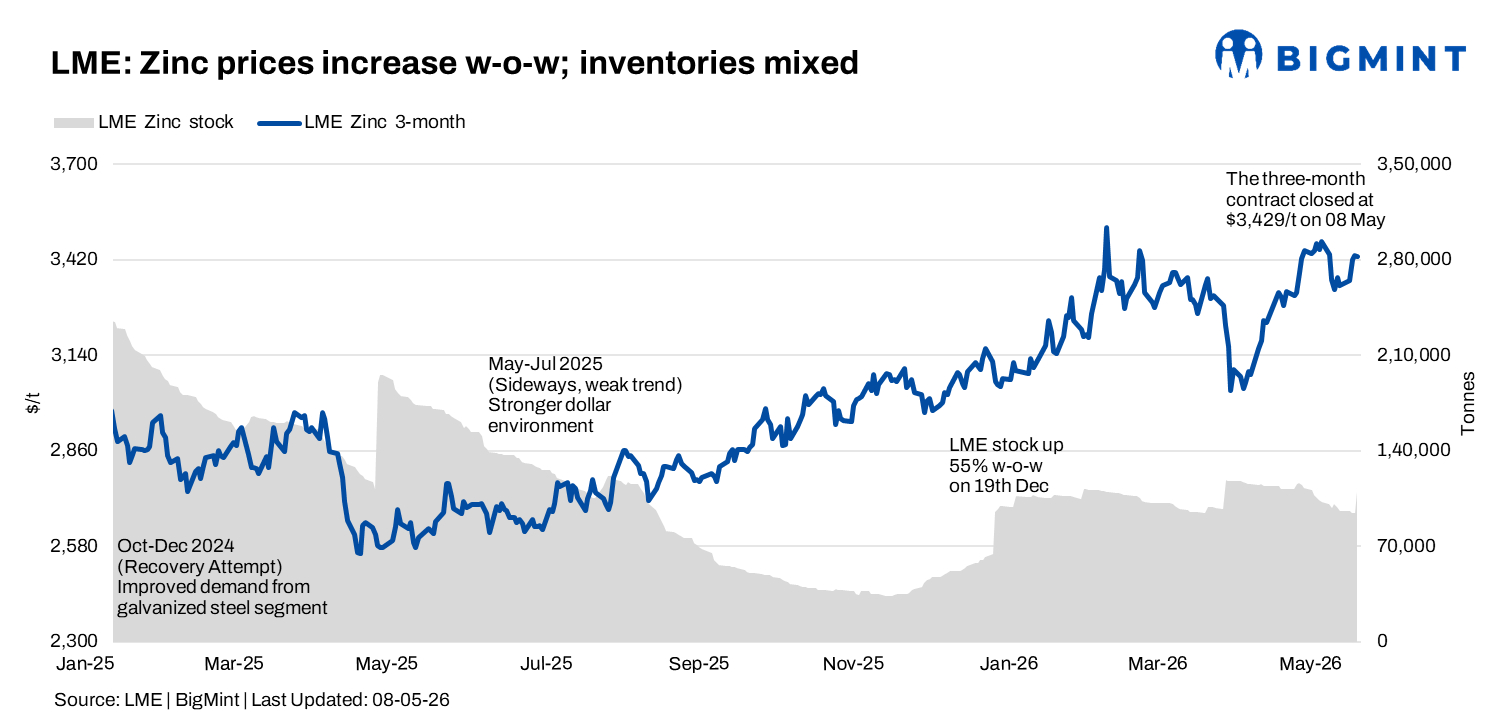

London Metal Exchange (LME) zinc prices maintained their upward momentum in the week ended 8 May 2026, supported by steady buying interest and firm market sentiment. Prices remained higher on a w-o-w basis despite a sharp increase in exchange inventories towards the end of the week. Market participants largely continued with cautious, need-based procurement amid elevated prices and mixed supply signals.

Price trends

LME zinc prices opened the week on a relatively stable note, with cash prices at $3,348/t on 5 May after closing at $3,349/t on 1 May.

Prices strengthened sharply during the mid-week sessions, rising to $3,402/t on 6 May and further to a weekly high of $3,425/t on 7 May amid firm buying interest and continued inventory drawdowns.

However, prices eased marginally towards the end of the week, with cash settlement closing at $3,417/t on 8 May following a substantial increase in warehouse inventories.

On a w-o-w basis, LME zinc cash prices increased by around 2%, reflecting sustained positive sentiment despite emerging supply-side pressure late in the week.

The three-month contract followed a similar trend, increasing from $3,343/t on 1 May to $3,429/t on 8 May, indicating stable forward market sentiment.

Inventory analysis

LME zinc inventories initially remained stable at 96,250 t on both 1 May and 5 May before declining steadily to 94,800 t on 6 May and 94,425 t on 7 May.

However, inventories rose sharply to 110,600 t on 8 May, marking a significant stock build of over 16,000 t d-o-d and reversing the earlier tightening trend observed during the week.

The sudden increase in visible stocks weighed slightly on market sentiment towards the close of the week, although prices largely remained resilient amid continued underlying demand support.

MCX zinc trends (4-8 May)

On the Multi Commodity Exchange (MCX), zinc futures largely mirrored global trends and traded within a firm range during the week.

The May contract opened at INR 343.05/kg on 4 May and strengthened steadily through the week, reaching a weekly high of INR 349.95/kg on 6 May before closing at INR 348.20/kg on 8 May.

Open interest fluctuated during the week and declined from 2,199 lots on 4 May to 1,989 lots on 8 May, indicating likely short covering and cautious fresh participation at higher levels.

Trading volumes remained moderate to healthy, while domestic buying activity continued to be primarily need-based amid elevated prices.

SHFE zinc trend

On the Shanghai Futures Exchange (SHFE), zinc prices displayed a mixed but largely stable trend during the week following the Labour Day holiday on 4th and 5th May.

Prices remained steady at $3,421/t on 6 May before declining to $3,390/t on 7 May. However, the market recovered sharply towards the end of the week, closing at $3,456/t on 8 May.

The overall movement suggests balanced demand conditions in China, with mild volatility but continued support from broader global zinc market sentiment.

Outlook

In the near term, LME zinc prices are expected to remain supported by steady underlying demand and firm broader market sentiment.

However, the sharp rise in exchange inventories towards the end of the week may limit aggressive upside momentum and could trigger cautious buying behaviour in the near term.

Prices are likely to find support in the $3,380-3,400/t range, while resistance is seen around $3,450-3,480/t.

Leave a Reply