- Freight costs and raw material shortages support prices

- Weak downstream demand limits aggressive billet buying

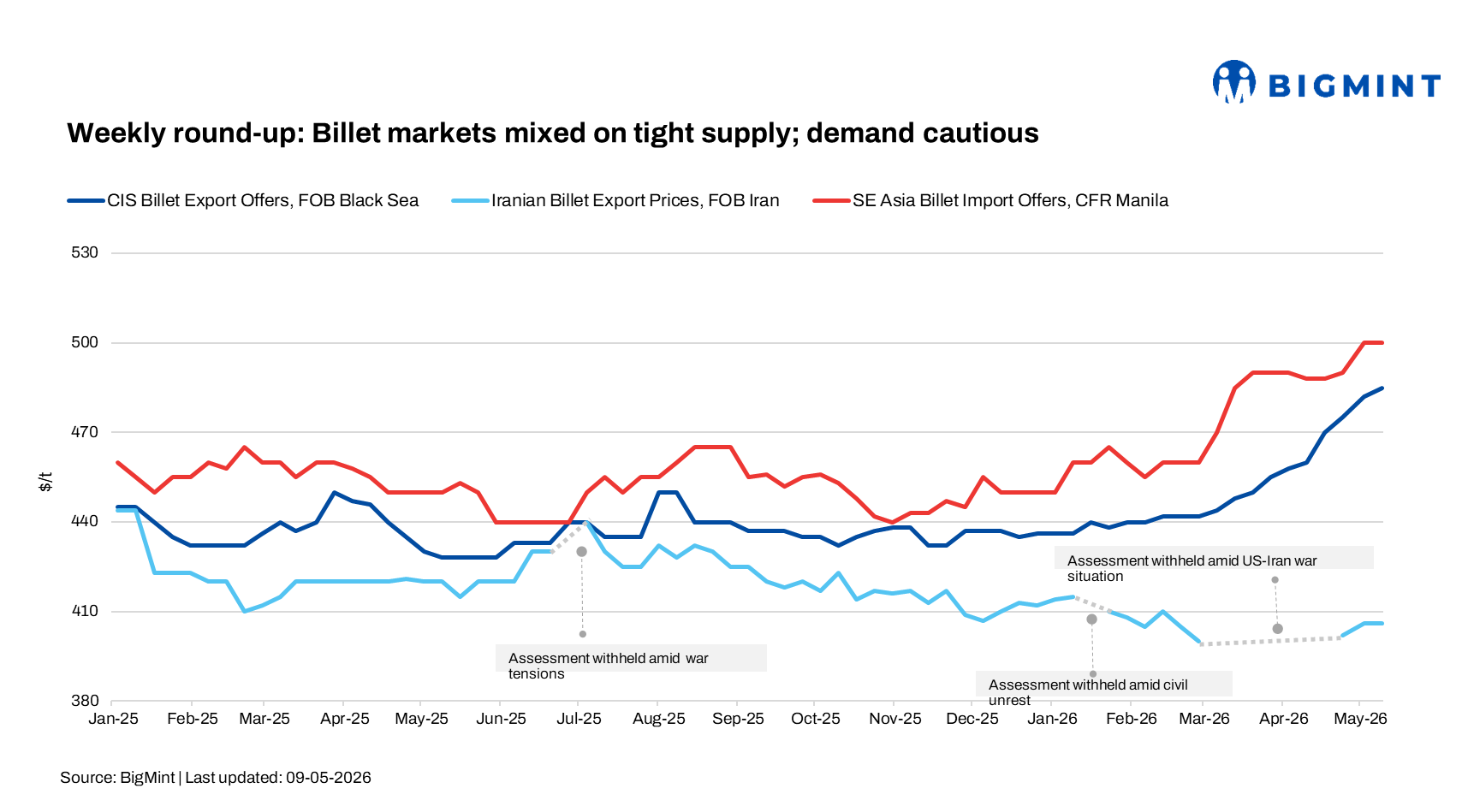

Global billet markets showed mixed trends during the week, with support mainly coming from supply-side constraints rather than demand recovery. The CIS/Black Sea region led gains on firmer seller control, stronger currency sentiment, and improved June booking interest.

Asia turned cautiously firmer after China reopened post-holidays, while Middle East markets were split-stable in Egypt but stronger in Saudi Arabia due to tightening semis availability and rising input costs. Overall, weak downstream steel demand continued to limit aggressive buying despite firm cost support.

Asian billet market

Asian billet and rebar markets ended the week slightly firmer, though trading remained thin. Early-week activity was subdued due to China’s holidays and lack of futures guidance, keeping buyers cautious across Southeast Asia.

Post-holiday, Chinese billet prices rose w-o-w, supported by improved sentiment, stronger futures in early sessions, and firmer raw material costs. Tangshan billet was assessed around RMB 3,100/t ($456/t), while export offers increased to $480-485/t FOB China. Inventory drawdowns and better physical steel sales added support, although rebar futures softened late in the week due to weak demand.

India is expected to re-emerge as an opportunistic billet supplier to GCC and Southeast Asian markets amid the continued absence of Iranian exports due to war-related disruptions. Supporting this trend, Rashtriya Ispat Nigam Limited (RINL) concluded a 30,000 t export tender for CONCAST billet on 8 May 2026 at around $480/t amid firm global sentiment and tightening regional supply.

In Southeast Asia, import billet indications were around $500/t CFR, remained same due to specification changes rather than fundamentals. Buying interest remained limited with no major spot deals reported. Overall sentiment improved modestly, but weak end-user demand capped gains.

CIS billet market

The CIS billet market strengthened during the week, driven by improved exporter confidence, firmer currency trends, and tighter availability from key suppliers. Russian square billet offers moved higher to $485-490/t FOB Black Sea, compared with $475-485/t a week earlier. Some mills were also targeting $495-500/t FOB for June production and early July shipments, reflecting bullish near-term expectations.

Turkiye remained a key demand center, with Russian billet heard at $505-510/t CFR Bartin, equivalent to $485/t FOB Black Sea. Meanwhile, billet export prices from Turkiye were heard around $535/t FOB for 3SP/equivalent grade material.

Donbas-origin material was reported at $500-505/t CFR, while Ukrainian offers remained higher at around $540/t CFR. Compared to prior ex-CIS levels of $495-500/t CFR, the market clearly shifted upward during the week.

Trading activity also improved, with multiple deals reported in Turkiye. Small parcels of 3,000-5,000 t were concluded at $498-500/t CFR, while a larger 17,000-19,000 t cargo was booked at similar levels, reinforcing market acceptance of higher pricing.

Middle East market

Middle East long steel markets showed a mixed but generally firm undertone, with contrasting dynamics between Egypt and Saudi Arabia.

In Egypt, the market remained largely stable as weak downstream demand offset rising production costs. Billet prices also remained steady at EGP 34,000-34,500/t ($655-654/t) EXW.

Despite recent gas price increases, subdued consumption and cautious buying behavior prevented any meaningful price hikes. Export rebar offers were unchanged at $610-620/t FOB, reflecting limited international competitiveness pressure.

In contrast, Saudi Arabia continued to strengthen, supported by tight semis availability and rising input costs. Rebar offers from Hadeed were heard at SAR 2,900-3,000/t ($773-800/t) delivered, while other mills targeted SAR 2,800-3,000/t ($745-800/t) delivered.

Billet offers increased to $545-565/t CFR amid limited availability of billets and direct reduced iron constrained rolling operations, leading mills to compete more aggressively for raw materials, including scrap cargoes.

Overall, Egypt remained stable under demand pressure, while Saudi Arabia maintained a bullish tone driven by supply-side tightness and cost inflation.

Outlook

Global billet markets are expected to remain supported in the upcoming days, underpinned by firm raw material costs, tight semis availability, and elevated freight rates. CIS and Middle East regions are likely to maintain firmer tones due to supply constraints, while Asian markets may see limited upside given cautious downstream steel demand.

However, buying activity in rebar markets is expected to stay subdued, restricting aggressive billet restocking. Price movements are likely to remain gradual across regions, with sentiment largely driven by supply-side dynamics rather than demand recovery.

Leave a Reply