- Tight Indonesian supply and rupee weakness supported higher Indian coal prices

- RKAB quota uncertainty kept market sentiment cautious

Indian portside prices of Indonesian-origin thermal coal witnessed a sharp week-on-week increase as of 8 May 2026, with gains of INR 200-400/t recorded across major grades. The uptrend was primarily driven by the continued depreciation of the Indian Rupee against the US Dollar, with the exchange rate hovering near record lows of around INR 95/USD, significantly inflating import costs.

Additionally, a sudden revival in Chinese buying interest tightened spot cargo availability in the Indonesian market, further supporting prices. According to BigMint data, Indonesia’s total thermal coal bulk exports stood at 28.6 million tonnes (mnt) in April 2026, of which exports to China reached 5.8 mnt, rising sharply by 28.5% month-on-month, highlighting stronger Chinese procurement activity and intensifying competition for cargoes.

Higher prices across key coal grades

Portside prices increased across all major Indonesian coal grades amid firm replacement costs and improved buying activity. High-grade 5,000 GAR coal prices rose by around INR 200/t week-on-week to INR 10,300/t at Kandla and INR 10,200/t at Visakhapatnam, supported by better offtake interest from industrial consumers.

Mid-grade 4,200 GAR coal prices increased by around INR 100/t to INR 7,950/t at Kandla and INR 7,850/t at Visakhapatnam, reflecting relatively balanced demand-supply conditions. Meanwhile, lower-grade 3,400 GAR coal registered the steepest increase, rising by around INR 350/t to nearly INR 5,850/t at Navlakhi amid tighter cargo availability and improved regional demand.

A market participant indicated that the Indonesian coal market has strengthened recently, driven mainly by rupee depreciation, which increased import costs and improved seller realizations. Earlier, weak demand and landed costs of MIFA material at around INR 5,100-5,200/t had squeezed trader margins, but the recent price rise has improved profitability. Sentiment was further supported by the expected closure of Magdalla port after 15 May, tightening near-term supply availability and raising logistical concerns, while limited High GAR cargo availability enabled importers to secure better margins, further supporting prices.

Port inventories remain comfortable despite price rise

India’s non-coking coal inventories at major ports increased by 3.7% w-o-w during Week 18, rising to 15.14 mnt from 14.6 mnt in Week 17, indicating continued cargo inflows despite subdued downstream demand. The inventory build-up reflects moderate evacuation levels and adequate near-term supply availability, which partially capped aggressive buying activity in the domestic market.

Thermal power plant stocks stay broadly adequate

Coal inventories at Indian thermal power plants remained largely stable at 53.7 mnt as of 7 May, equivalent to around 17 days of consumption, suggesting an overall comfortable supply position. However, inventory distribution remained uneven, with nearly 17 plants operating at critical stock levels, including facilities dependent on domestic coal, imported coal, and washery rejects. This highlights persistent regional supply imbalances despite healthy aggregate stock levels.

Global market strength and freight trends influence sentiment

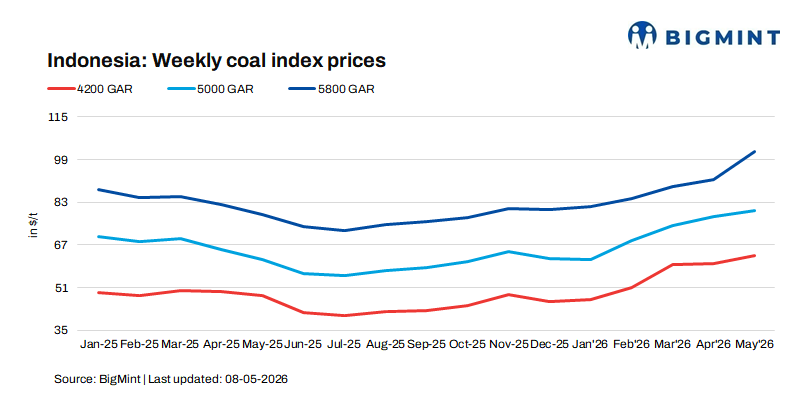

International coal markets continued to show firm undertones, supported by stronger Asian demand and relatively tighter spot availability in Indonesia. Prices for 5,800 GAR coal surged sharply by around $8-9/t week-on-week, while 4,200 GAR coal prices increased by around $1-2/t and 3,400 GAR coal gained approximately $2-2.5/t.

On the freight front, Supramax freight rates from East Kalimantan to Navlakhi declined by around $1.1/t w-o-w to nearly $19.4/t, offering partial cost relief to importers. However, the impact of lower freight was largely offset by higher FOB coal prices and rupee depreciation.

Indonesian supply tightness continues amid RKAB uncertainty

Supply tightness in the Indonesian thermal coal market persisted across all calorific value segments as miners continued prioritising Domestic Market Obligation (DMO) commitments while awaiting clarity on mid-year RKAB production quota approvals. Most June- and July-loading cargoes have already been committed, with September laycan cargoes gradually emerging in the market.

However, despite tight supply conditions, spot prices for mid- and low-CV coal have recently shown signs of consolidation rather than aggressive upward movement. Wide bid-offer spreads continue to dominate trading activity, reflecting contrasting expectations between buyers and sellers. While sellers expect ongoing supply tightness to support prices, buyers remain cautious amid expectations that higher production quotas could eventually improve cargo availability and soften prices.

At the same time, financial sentiment in the high-CV coal market has turned slightly cautious following the recent rally. Flattening FOB forward curves, easing LNG market concerns, stable low-CV prices, and resistance to higher offer levels have contributed to a more balanced near-term market tone.

Outlook

Indian portside Indonesian thermal coal prices are expected to remain upside in the near term, supported by rupee weakness, tighter Indonesian spot availability, and sustained Chinese buying interest. Market direction in the coming weeks will largely depend on Indonesia’s RKAB quota decisions, Chinese import demand trends, and currency movements. Any increase in Indonesian production quotas could ease supply tightness and moderate price momentum going forward.

Leave a Reply