- Primary rebar trade prices drop INR 300/t ($3/t)

- Rising stock levels pile pressure on IF rebar prices

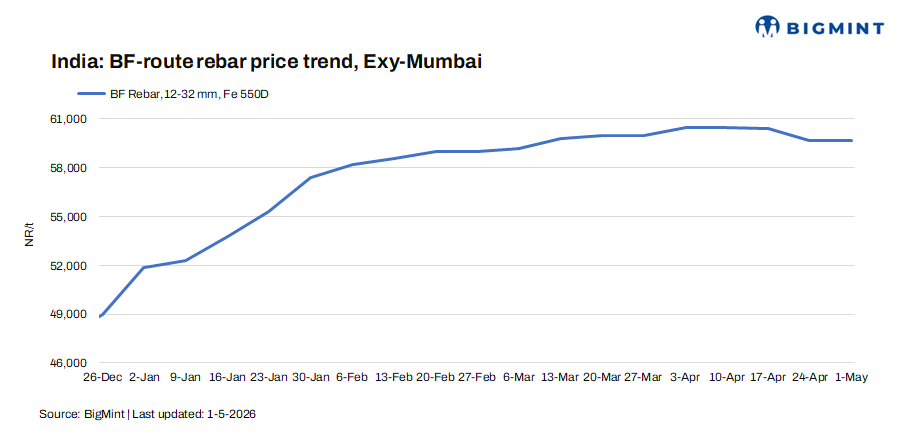

Indian primary steelmakers have rolled over rebar list prices for early-May 2026 dispatches over end-April price tags, sources informed BigMint. Post-revision, list prices stood at INR 59,000-60,000/t ($620-630/t) on landed basis.

Trade-level BF-rebar prices (distributor to dealer) dropped by INR 300/t ($3/t) to INR 59,400/t ($624/t) exy-Mumbai, as per BigMint’s assessment on 5 May. Market sentiments remained subdued last month. Buying activity slowed noticeably, with participants limiting purchases to immediate requirements. They reported comfortable inventory levels, supported by weaker material offtake toward the end of the month. In response to subdued demand, mills extended price support on list prices to stabilise the market.

In the projects segment, prices opened at around INR 58,500-59,000/t ($615-625/t) FOR basis. In the projects segment, demand conditions were relatively weak, with limited inquiries and slower procurement cycles. Construction activity was impacted by election-related labour shortages, leading to execution delays and deferred material purchases. Additionally, price volatility and overall market uncertainty prompted buyers to adopt a cautious approach.

Rebar inventories at tier-1 mills rose by over 40% m-o-m in early-May, as per sources.

Factors driving the market

1. IF-rebar trade prices decline m-o-m: Induction Furnace (IF) rebar trade prices declined across major markets in April amid weak demand conditions. After a steady start, sluggish finished steel demand led mills to cut list prices and offer discounts to clear inventories. While dispatches remained decent, rising stock levels around 10-12 days by early May kept pressure on prices. IF-rebar trade prices dropped by INR 4,200/t ($44/t) m-o-m to INR 49,200/t ($517/t) exw-Mumbai as of 2 May.

The blast furnace (BF) to IF rebar price spread in Mumbai widened to around INR 10,500-11,000/t ($110-116/t) this week. IF rebar continues to dominate the Indian market, accounting for an estimated 65-70% share.

2. Raw material prices show mixed trends m-o-m: Prices of major raw materials used in the BF route showed mixed trends last month. BigMint’s Odisha iron ore fines (Fe 62%) index dropped m-o-m by INR 87/t ($1/t) to INR 5,725/t ($60/t) ex-mines in April.

BigMint’s premium hard coking coal (PHCC) index rose $5/t to $255/t CNF Paradip in April.

3. Property registrations drop m-o-m: Property registrations in Mumbai, the country’s largest real estate market, dropped by 13% m-o-m to 13,864 units in April as against 15,983 units in March, as per data released by Knight Frank India. Likewise, monthly registrations were up 14% as against 12,142 units reported in March last year.

Property registrations declined m-o-m due to seasonal moderation after strong year-end closures. Despite this dip, Mumbai’s residential demand remains resilient, with stable buyer confidence and only marginal softening in ticket sizes reflected in near-flat stamp duty collections.

Outlook

Trade prices may remain under mild pressure due to weak demand and cautious buying. Mills may offer price support in coming days to stabilise prices and prevent further downside amid subdued market sentiment.

Leave a Reply