- Subdued demand, falling imports in China drag prices lower

- Weak demand growth to push market to slight surplus in 2026

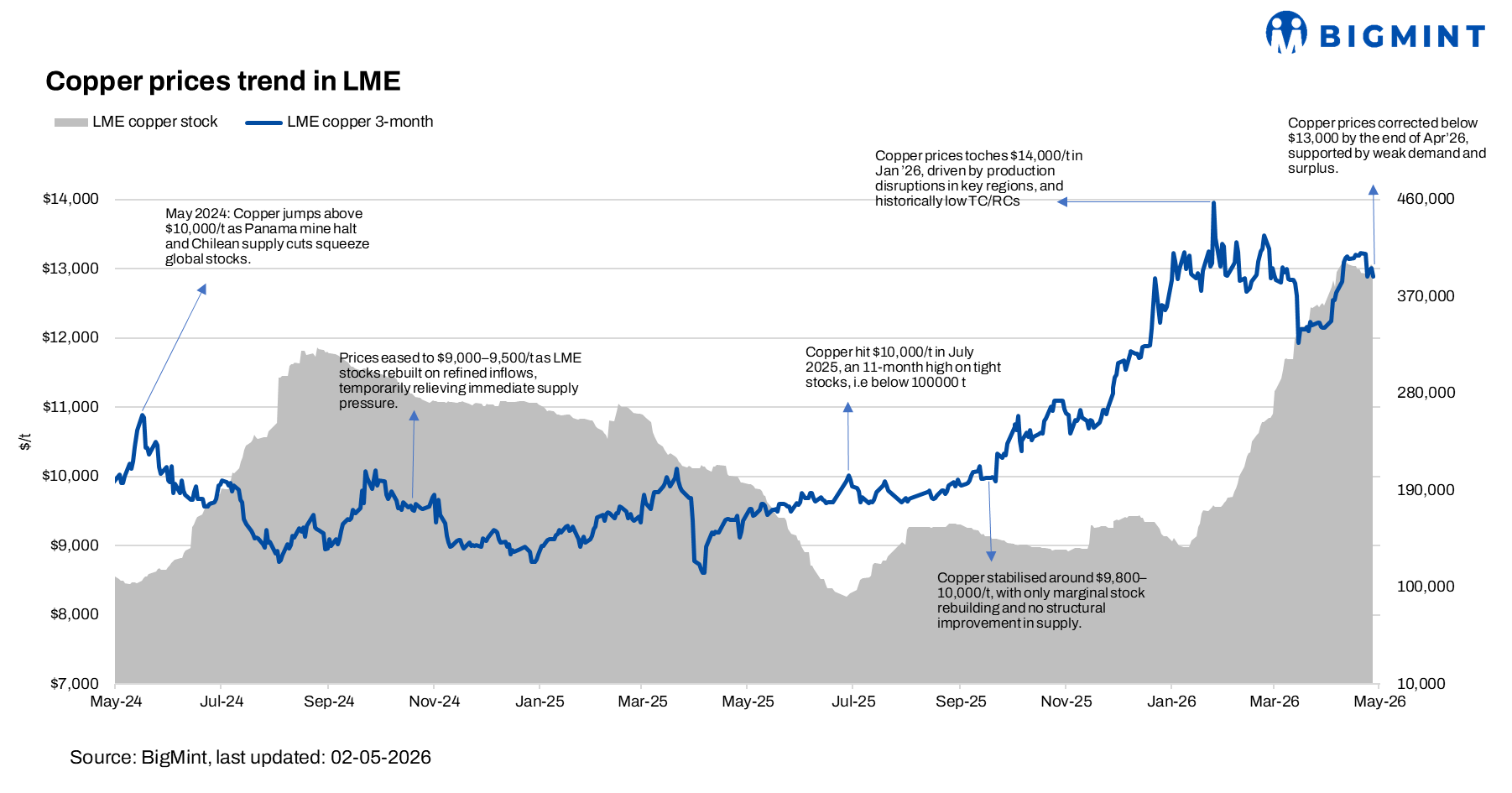

Copper prices on the London Metal Exchange (LME) declined by about $300/tonne (t) (2.3%) to $12,900/t on 01 May (as recorded at 11:40 IST) from $13,200/t a week ago, reflecting a cautious, bearish trend amid persistent demand weakness despite ongoing supply-side risks.

Prices trended lower through the week, pressured by weak consumption signals from China, where strong refined output and falling imports pointed to subdued buying interest. The global refined copper market remained in a surplus of around 276,000 t as of February, with expectations that the oversupply will persist through 2027, further weighing on market sentiment.

However, the downside was partly cushioned by supply-side concerns linked to geopolitical tensions around the Strait of Hormuz and friction between the United States and Iran, which disrupted sulphur supply chains and raised sulphuric acid costs.

Additionally, potential production risks in the Democratic Republic of Congo, with a possible decline of around 125,000 t by 2026, provided underlying support. Overall, demand weakness and elevated inventories outweighed supply risks, resulting in a net price decline during the week.

China’s May Day holiday period (May 1-5) typically creates short-term volatility in copper markets, with pre-holiday restocking offering limited support to prices, while subdued trading activity and weak underlying demand during the holiday period contribute to downward pressure.

Japan’s update

Japan’s copper fabrication sector continued its recovery momentum in FY’25, with downstream production reaching around 0.67 million tonnes (mnt), up 4% y-o-y, marking the second consecutive year of growth, primarily driven by strong demand for copper bars, which rose 7.3% y-o-y, reflecting increased usage in high-performance computing and advanced electronics.

The outlook remains supported by capacity expansions from Mitsui Mining and Smelting and higher upstream output from Sumitomo Metal Mining, reinforcing a steady growth trajectory led by technology-driven demand.

India’s update

India’s copper scrap market remained firm, supported by steady demand from recyclers and secondary manufacturers amid tight availability, particularly in premium grades. Supply constraints were exacerbated by limited container availability from the Middle East, diversion of quality scrap to Far East markets, and ongoing quality-related scrutiny in imports, which delayed clearances.

On the imports side, EU-origin brass honey scrap was assessed at around 59.5% of 3M LME, but higher costs and cautious buying limited fresh bookings. Overall, tight supply, elevated processing costs, and weak demand conditions kept market activity restrained.

Outlook

Copper’s outlook remains finely balanced, with market direction dependent on whether supply constraints or demand weakness intensify faster. According to the International Copper Study Group (ICSG), limited mine supply growth and tight concentrate availability are expected to keep refined production growth subdued at around 0.4%.

However, demand growth has been revised down to 1.6% amid geopolitical and macroeconomic uncertainties. As a result, the market is now expected to shift to a marginal surplus of around 96,000 t in 2026, indicating a delicate balance that is likely to keep prices volatile and uncertain in the near term.

Leave a Reply