- Indonesia disruptions and sulphur costs lift sentiment

- China demand recovery supports near-term outlook

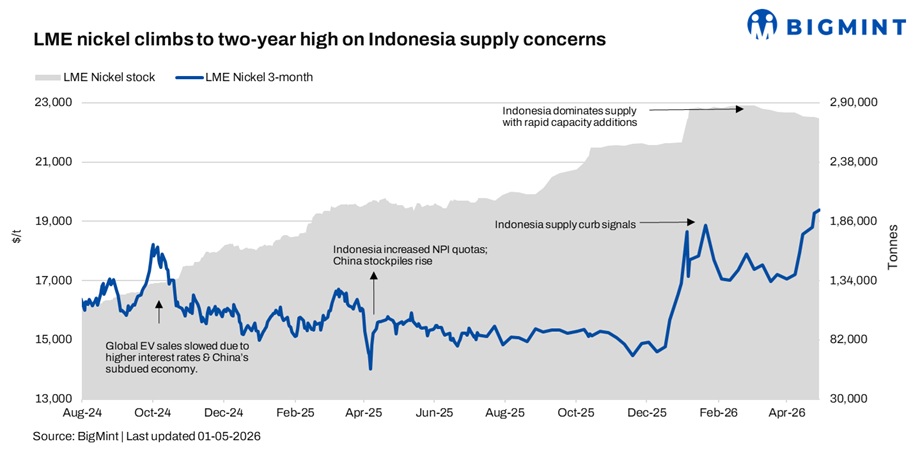

London Metal Exchange (LME) nickel futures extended gains for a fifth consecutive session in the week ended 1 May, with the three-month contract closing at $19,385/t, up 3.1% w-o-w from $18,800/t. Prices touched their highest level since May 2024, despite a firm US dollar, as tightening supply concerns outweighed macro pressure. LME inventories remained broadly stable at 276,396 t, suggesting balanced exchange stocks.

Indonesia remains key driver

The latest rally was primarily supported by Indonesia’s tighter mining quotas, ongoing ore supply disruptions, and rising sulphur costs affecting high-pressure acid leach (HPAL) producers. Market participants noted that tighter raw material availability and uncertainty over future policy direction continue to strengthen sentiment. Since the Iran conflict began, nickel prices have risen nearly 13.6%, also reflecting concerns over freight, energy and input costs.

Nickel Industries reported its strongest quarterly EBITDA since late 2023, while Harum Energy posted improved earnings as nickel offset weaker coal profits. Meanwhile, Sumitomo’s exit from Madagascar’s Ambatovy project highlighted challenges in global nickel operations outside Indonesia.

China adds momentum through cost pressures

China’s stainless steel futures climbed to multi-year highs ahead of the May Day holidays, driven by tighter scrap availability and a temporary output cut by a major nickel-cobalt producer. Stricter scrap invoicing controls have raised concerns over secondary raw material supply, prompting mills to increase reliance on nickel pig iron (NPI). As a result, NPI offers moved higher, lending further support to nickel sentiment.

However, physical stainless steel demand in China remained relatively subdued, with downstream buyers cautious at elevated futures levels. Market inventories declined only marginally, indicating that the recent rally has been led more by raw material cost escalation than strong end-user consumption.

Outlook

Nickel prices are expected to remain firm in the near term, supported by Indonesia-led supply constraints, rising production costs and recovering Chinese demand. However, gains may be capped by ample global inventories and broader macroeconomic uncertainty. Any easing in Indonesian mining policies or weaker stainless steel demand could trigger short-term corrections, while continued supply discipline may keep sentiment positive.

Leave a Reply