- Indonesian benchmarks rise, lifting Indian port prices

- Met coke market remains largely stable amid policy changes

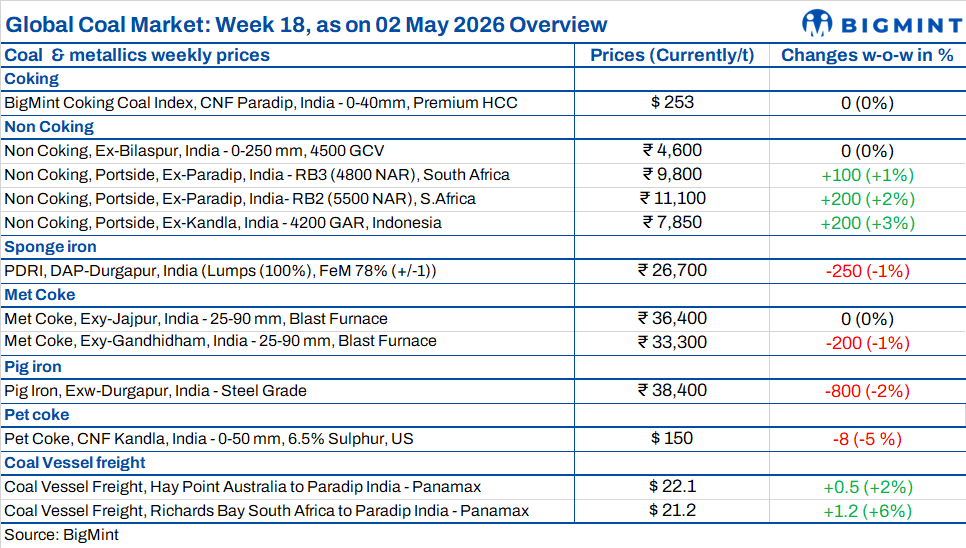

Indian and global coal markets witnessed mixed trends in the week ended 1 May 2026 amid shifting demand trends. While Indonesian portside prices rose on the back of supply tightness and seasonal demand, South African and domestic coal remained under pressure from thin demand.

Indonesian benchmarks, portside prices strengthen

Indonesia’s HBA coal benchmarks rose across all segments for early May 2026, supported by seasonal demand, tight spot supply, and steady Asian buying. The 6,322 GAR index increased 3% to $106.57/t, while 5,300 GAR rose 2.4% to $79.56/t. Lower grades outperformed, with 4,100 GAR up 5.3% to $55.66/t and 3,400 GAR up 1.2% to $38.76/t. Reflecting this, Indian portside Indonesian coal prices also rose by INR 200-400/t across all grades, majorly driven by rupee depreciation (95/USD), higher offers, and freight costs, while demand from Morbi’s ceramic units also improved. However, ample inventories and cautious buying limited further upside.

South African thermal coal shows mixed trend amid weak demand

South African non-coking coal prices at Indian ports showed mixed trends w-o-w, with ex-Paradip and ex-Vizag RB2 (5,500 NAR) rising INR 200/t to INR 11,000/t, while RB3 (4,800 NAR) eased to INR 9,750/t. The increase in RB2 was driven by higher FOB offers ($95-96/t), rising freight ($23/t) due to firm bunker prices, and rupee depreciation beyond 95/USD, increasing landed costs. However, demand remained weak as sponge iron (PDRI) prices fell by INR 100-250/t, compressing margins. Lower domestic coal prices (down up to INR 700/t), ample inventories (14.6 mnt), and slow cargo movement kept buyers cautious and limited trade activity.

Stable domestic coal prices amid weak auction demand despite lower output

Domestic thermal coal prices remained stable w-o-w, with 4,500 GCV at INR 4,600/t and 5,000 GCV at INR 6,250/t ex-Bilaspur. Coal India Limited (CIL) reported muted participation in its April Single Window Mode Agnostic (SWMA) e-auction, allocating only 11.77 mnt out of 30.55 mnt (39%) despite a strong 51% premium, reflecting cautious buying amid ample supply and weak downstream demand. Meanwhile, April production declined to 56.1 mnt, down 9.7% y-o-y and 33.6% m-o-m, due to post-March output normalisation and fewer working days, though dispatches remained stable, indicating steady consumption trends.

Over 3 mnt of US coal en route to India; demand supported by petcoke shift

Over 3.1 mnt of US NAPP and ILB coal is en route to India, with FOB Baltimore prices at $93-94/t and CFR India around $135-140/t, while buyers target $130/t. Strong retail lifting (107,000 t/week) and three weeks of stock drawdowns at Kandla and Tuna reflect steady demand. Cement producers are shifting from petcoke ($158/t) to cheaper coal, supporting offtake. However, rising arrivals and potential monsoon-led slowdown may pressure prices.

Met coke market remains largely stable amid policy changes

India’s met coke market remains largely stable with cautious sentiment after the DGTR (Directorate General of Trade Remedies) proposed lower anti-dumping duties of $42.95-128.8/t. BigMint learnt that imported Indonesian met coke offers have risen about $10/t, with BigMint’s assessment of BF-grade coke at $291/t CFR India rising by $2/t, keeping import parity firm. Domestic prices stayed stable at INR 36,400/t (east) and INR 33,500/t (west), supported by firm coking coal costs at $231/t FOB. However, falling pig iron prices (INR 900/t) and weak steel demand weighed on sentiment. Rising import enquiries, adequate domestic supply, and policy uncertainty kept buyers cautious, limiting sharp price movement and sustaining a narrow trading range.

Petcoke prices decline as coal substitution weakens demand

Global petcoke prices remained under pressure as Indian cement producers shifted to cheaper thermal coal, reducing demand. CFR India 6.5% petcoke declined to $156/t ($4/t m-o-m), with deals reported near $140-145/t. US Gulf Coast 4.5% petcoke fell sharply by $10.2/t to $112/t, reversing a prolonged rally. India’s petcoke imports dropped 44% y-o-y in Q1CY’26, reflecting weak buying interest. High freight costs and availability of cheaper coal alternatives further weighed on sentiment. Nayara Energy Ltd (NEL) has raised its petcoke price to INR 21,000/t effective 1 May 2026, marking a cumulative increase of INR 2,330/t from INR 18,670/t on 1 April (after an interim hike to INR 19,670/t on 16 April). The sharp upward revision is primarily driven by tightening global market conditions amid escalating US-Iran tensions.

Freight market mixed, cost pressures persist

Dry bulk coal freights to India showed mixed trends w-o-w, with Panamax rates firm on tight tonnage and active Australian fixtures, while Supramax softened due to weak Asian cargo demand and ample vessel supply. Bunker prices rose $16/t to $779/t, tracking higher Brent crude oil at $111.08/bbl ($6.55), adding cost pressure. The Baltic Index gained 13 points to 2,686, indicating mild recovery. Market sentiment remained cautious amid limited enquiries and geopolitical uncertainty.

Leave a Reply