- Temporary, operational disruptions lead to decline

- Strong prices and H2 ramp-up to support recovery, margins

Glencore reported a q-o-q decline in coal production in Q1 2026, primarily attributable to planned operational activities and temporary disruptions, including mine sequencing, longwall transitions, and weather-related impacts. Despite this moderation in output, underlying market fundamentals remained supportive, with stable demand conditions and firm coal prices continuing to underpin the company’s earnings outlook.

Sequential decline across coal segments

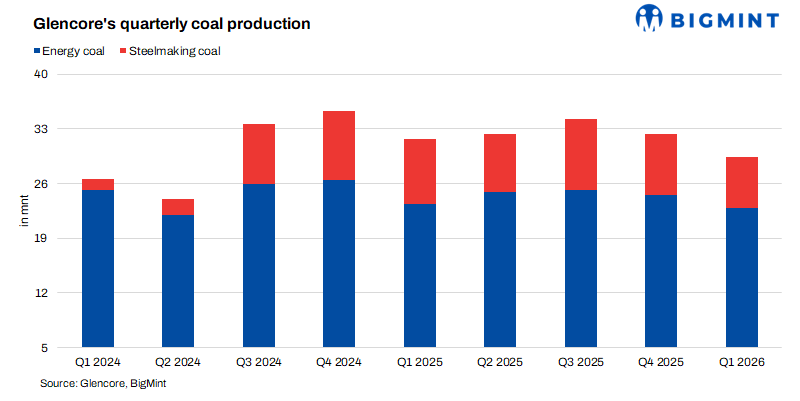

Total coal production stood at 29.4 million tonnes (mnt) in Q1 2026, marking a 9% drop from 32.3 mnt in Q4 2025. The decline was visible across both key segments:

Steelmaking coal: Fell to 6.5 mnt, down 17% q-o-q (vs 7.8 mnt in Q4 2025)

Energy coal: Declined to 22.9 mnt, down 7% q-o-q (vs 24.5 mnt in Q4 2025)

This indicates a broad-based but controlled moderation, rather than a structural slowdown.

Key factors behind decline

The q-o-q softness was largely operational and temporary, driven by:

- Mine sequencing in Canada (EVR): Lower yields due to pit transitions

- Planned longwall moves in Australia (Oaky Creek, Ulan): Temporary production disruptions

- Weather-related impacts in Queensland: Affecting Australian metallurgical coal output

- Cerrejón output strategy: Continued disciplined production cuts

These factors point to intentional or cyclical constraints, not demand weakness.

Regional trends highlight mixed performance

Australian thermal coal operations demonstrated relative resilience during the quarter, primarily supported by lower strip ratios, which improved mining efficiency and helped sustain output levels, thereby partially offsetting declines in other regions.

In contrast, the Cerrejón operations in Colombia continued to weigh on overall production, reflecting structurally lower output following previously implemented production cuts. Meanwhile, Canadian steelmaking coal operations experienced a decline in volumes due to ongoing pit sequencing activities, which affected yield profiles and, in turn, reduced overall metallurgical coal production.

Operational strategy signals H2 rebound

A key takeaway is Glencore’s clear production weighting toward H2 2026, suggesting that:

- Deferred volumes from Q1 will materialize later in the year

- Improved pit access, longwall completion, and strip ratios will lift output

- Coal production guidance remains unchanged, reinforcing confidence in recovery

Market context remains supportive

Despite a decline in production volumes during Q1, the approximately 22% year-to-date increase in energy coal prices provides a significant counterbalance to rising operational costs, particularly those related to diesel consumption and logistics. This price strength enhances revenue realization per tonne, enabling Glencore to absorb cost pressures more effectively. As a result, even with lower output levels, overall margins are expected to remain supported, limiting the financial impact of temporary production disruptions.

The Q1 2026 performance reflects a temporary, timing-led moderation in output rather than any weakening of underlying fundamentals. Supported by stable demand conditions, firm commodity prices, and a clearly defined H2 production ramp-up, Glencore remains well-positioned to recover volumes and maintain profitability through the remainder of 2026.

Leave a Reply