- Prices steady, backed by import parity and potential Indonesian supply tightness

- Mixed downstream signals keep market range-bound

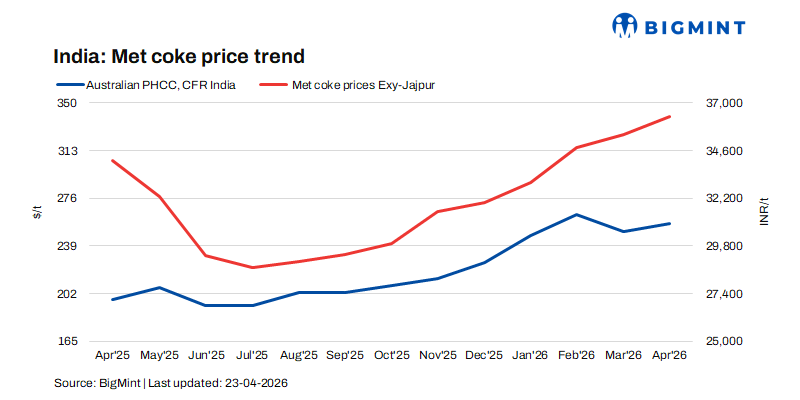

India’s blast furnace (BF)-grade metallurgical coke prices remained stable week-on-week as of 23 April 2026, supported by balanced market conditions. Prices were steady at INR 36,400/t ex-Jajpur in eastern India and INR 33,500/t ex-Gandhidham in the western region.

Foundry-grade (+90 mm) coke prices also held unchanged at INR 36,400/t ex-Rajkot. Market stability was further reflected in recent trade activity, including a concluded deal of around 6,000 t at approximately INR 36,500/t ex-works, indicating firm but not aggressive buying sentiment.

“The market is relatively stable. Not much trades have been concluded in eastern India.”, quoted a market participant.

Import parity anchors price stability

Import parity continues to act as a key support for domestic coke prices. Indonesian-origin BF-grade coke (65/63 CSR) was assessed at $289/t CFR India, slightly higher on a weekly basis, reinforcing the domestic price floor.

A recent bulk transaction of about 30,000 t at $262/t FOB highlights continued reliance on imported material. Expectations of tighter supply from Indonesia in May – due to shifting exports towards markets such as Brazil are likely to sustain price firmness. Stable freight rates (Handymax: $30-35/t; Panamax: $25-26/t) further ensure predictable landed costs.

Raw material trends provide cost support

Upstream cost dynamics remain supportive, with Australian premium hard coking coal (PHCC) prices holding steady at $231/t FOB. Additionally, stable conditions in China’s coking coal and coke market – characterized by steady supply, controlled inventories, and resilient steel demand – are contributing to a stable global pricing environment, limiting downside risks for domestic coke prices.

Pig iron prices edge down w-o-w

Downstream indicators present a mixed picture. Steel-grade pig iron prices in Durgapur declined by INR 900/t week-on-week to INR 39,700/t ex-works, suggesting some softening in spot demand.

Outlook

The near-term outlook for India’s metallurgical coke market remains stable with a slight upward bias. Firm import parity, anticipated tightening in Indonesian supply, and steady steel sector demand are expected to support prices. However, subdued trends in parts of the downstream segment may limit sharp increases. Overall, prices are likely to remain range-bound, with gradual upward pressure in the short term.

Leave a Reply