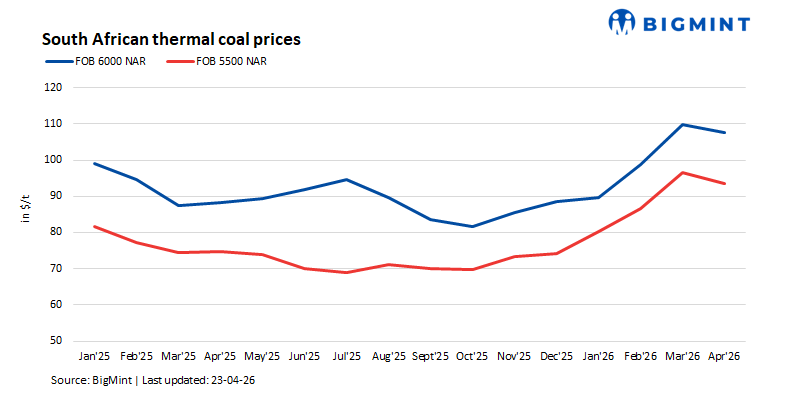

- Coal emerges as only scalable substitute to gas, prices climb higher

- Persistent gas shortage could add 10-20 mnt of coal demand per quarter

A halt in LNG exports from the Persian Gulf following the closure of the Strait of Hormuz is triggering a structural shift in global fuel consumption patterns. Vessel tracking data indicates that shipments from key exporters have stopped entirely, removing a major supply source for Asia and Europe. The disruption is forcing countries to pivot towards coal as the only immediately scalable substitute.

The scale of the disruption

The Persian Gulf is home to major LNG exporters, including Qatar, the UAE, and Saudi Arabia. Together, they supply tens of millions of tonnes of LNG annually to Asia and Europe. That supply has now stopped.

Spot LNG prices have reacted, but not as sharply as one might expect. The spot LNG contract delivered to Northeast Asia decreased to $15.51 per MMBtu — a drop, not a spike. This suggests that the market is still digesting the news or that buyers are holding back.

In Europe, the TTF June contract increased by 4% to EUR 41.85 per megawatt-hour. EU gas storage is at just 30% of capacity, compared to 42% at this time last year. Norwegian gas flows to Europe have also dropped due to planned maintenance on the Troll and Kollsnes fields.

Coal is the only scalable substitute

When gas is unavailable or too expensive, coal is the only fuel that can scale quickly. Power plants that have been idled or converted can be restarted. Import terminals can redirect cargoes. The global coal market is designed for exactly this kind of shock.

The impact will be felt differently across regions:

- Asia: Japan, South Korea, and Taiwan are already increasing coal procurement. Taiwan’s March coal generation was above forecast. South Korea has issued a long-term tender. China’s domestic prices are rising, and imports are expected to rebound.

- Europe: Italy is already talking about restarting coal plants. DES ARA forward prices (for high-CV thermal coal delivered at the ports of Amsterdam/Rotterdam/Antwerp) have jumped, with the June contract rising $3.75/t to $105/t. The Cal 27 contract gained $3.60/t to $111.85/t. The market is pricing in tighter supply later this year.

How much coal demand could be added?

Estimates vary, but a sustained Persian Gulf closure could add 10-20 million tonnes (mnt) of incremental coal demand per quarter across Asia and Europe. That is enough to shift the global balance from surplus to deficit.

The most immediate impact will be on high-CV coals (5,500-6,000 kcal/kg), which are most suitable for replacing gas in power generation. NEWC prices have already bounced back strongly, with spot 6,000 kcal/kg gaining $3.50/t to $128.50/t.

Outlook

The trajectory of the market will depend on several key variables, including the duration of the Strait of Hormuz closure, i.e., whether it extends for days, weeks, or months, as well as Europe’s gas storage levels, which are currently at 30% compared with higher levels a year earlier. In Asia, LNG inventories in Japan and South Korea provide a buffer but remain finite, while China’s procurement strategy could prove definitive, with aggressive buying likely to drive a sharp price response.

Against this backdrop, the halt in Persian Gulf LNG exports stands out as the primary catalyst for gas-to-coal switching in 2026, leaving both Europe and Asia exposed. Coal prices have already begun to rise, and forward curves indicate further tightening, suggesting that a prolonged disruption would force a rapid and sustained increase in global coal consumption.

Leave a Reply