- Production quota delays, DMO focus cap Indonesian exports

- Demand remains weak with selective buying by China, India

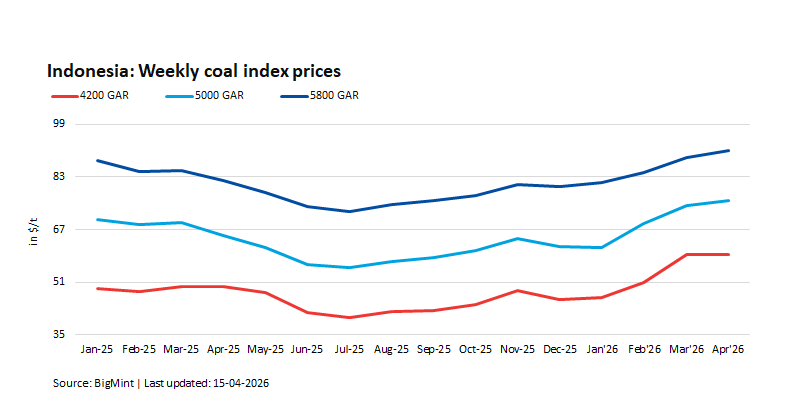

The Asian thermal coal market has remained firm in recent days, but the primary driver has not been a surge in demand. Instead, prices are being supported by significant supply-side constraints originating in Indonesia, the world’s largest exporter of thermal coal. Delays in obtaining government approvals and a focus on domestic obligations are limiting the amount of coal available for international buyers.

The quota bottleneck

A key issue is the delay in issuing annual production quotas, known locally as RKAB, to Indonesian miners for the 2026 calendar year. Several miners have not yet received their full allocations. This uncertainty has made it difficult for producers to commit to large export shipments, as they do not know how much coal they will be allowed to mine for the rest of the year.

The situation is particularly tight for miners of ultra-low and mid-calorific value coal grades, where the absence of quota increases has constrained supply. The daily export rate for Indonesian thermal coal reflects this tightness. Over a recent five-day period, daily exports averaged 890,000 tonnes (t), which was 17% lower than the previous week and 32% below the average export rate for the whole of 2025.

Domestic market priorities

Indonesian miners are also prioritising their domestic market obligation, or DMO. This government regulation requires coal producers to sell a portion of their output to local buyers, including power plants and smelters. A significant share of these DMO volumes must be fulfilled by the middle of the year, giving miners an incentive to allocate coal to the domestic market first.

Selling to the domestic market also offers a strategic advantage. Miners believe that completing their DMO volumes strengthens their case when requesting higher production quotas from the government in the future. As a result, they have little urgency to sell into export channels. Domestic Indonesian smelter demand remains strong, with local buyers reportedly willing to pay a premium over index-linked prices.

Impact on trade and prices

This supply dynamic is shaping trading behaviour across the region. Traders who hold long positions from earlier purchases are finding themselves forced to sell, while miners can release prompt volumes only in small quantities. This has created an uneven liquidity situation, particularly for mid-calorific value grades.

Selective buying

On the demand side, buyers have become selective. China has shifted its interest toward cheaper, ultra-low calorific value Indonesian coal, with power plants switching procurement from 4,200 kcal/kg to lower grades. Indian demand remains subdued as ports and power plants hold large inventories. However, steady demand continues from Japan, South Korea, Taiwan, and Vietnam for mid- to high-calorific value coal.

Until the quota situation is resolved and miners feel confident committing to larger export volumes, the Indonesian supply side is likely to remain the dominant factor supporting thermal coal prices across Asia.

Leave a Reply