- Demand stays need-based; coking coal drops $7/t w-o-w

- Supply tightens in north India; inventory weighs on prices in west

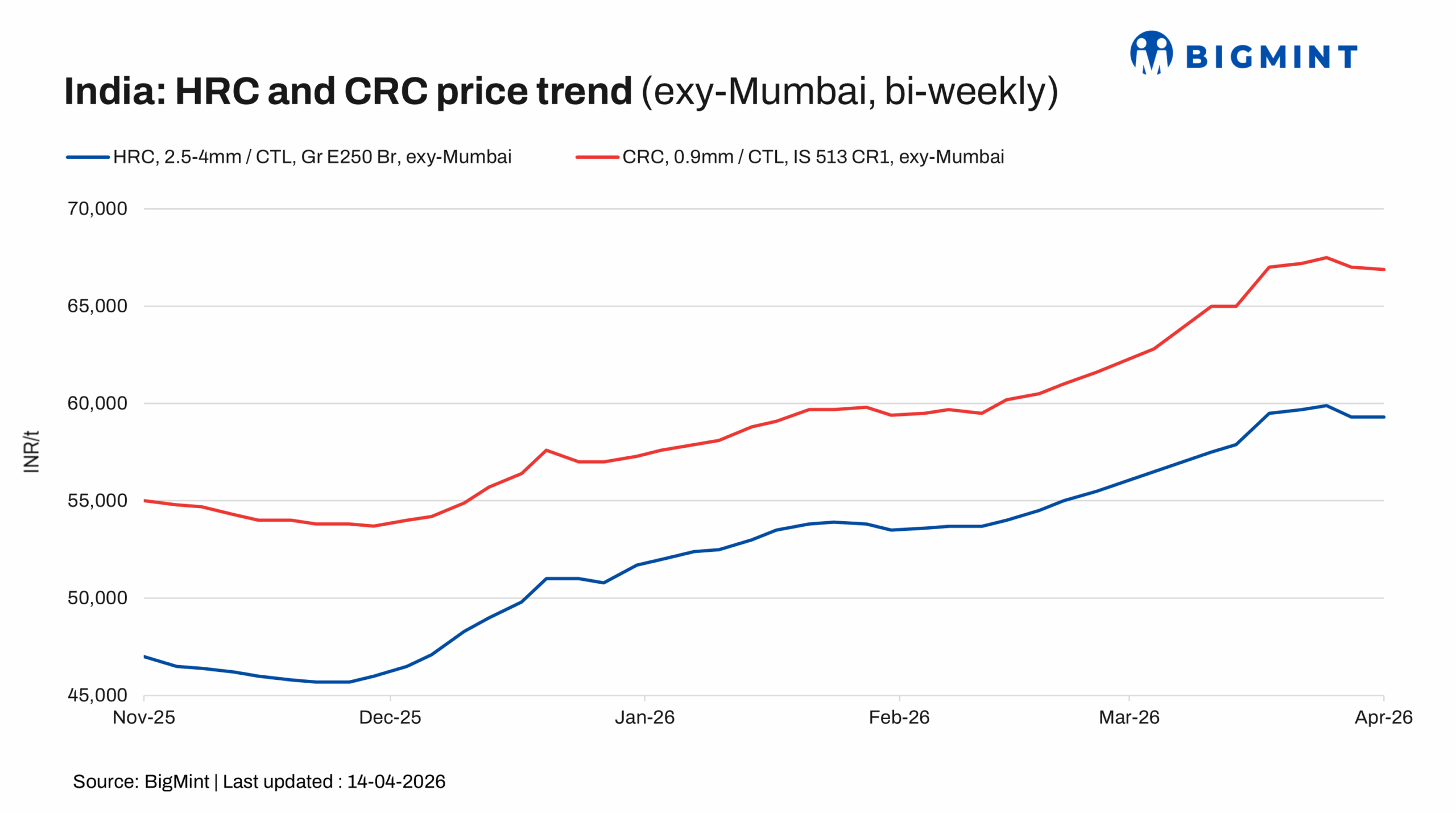

Trade-level prices of hot-rolled coils (HRC) in India remained stable-to-slightly lower this week, with HRC prices assessed in the range of INR 57,300-61,000/t ($616-655/t) and cold-rolled coil (CRC) prices assessed at INR 62,200-69,800/t ($668-750/t), as subdued demand and cautious market sentiment continued to weigh on prices.

BigMint’s bi-weekly benchmark assessment for HRC (IS2062, Gr E250, 2.5-8 mm/CTL) declined by INR 600/t ($6/t) w-o-w to INR 59,300/t ($637/t) as of 14 April, compared to INR 59,900/t ($643/t) on 7 April.

Similarly, CRC (IS513, Gr O, 0.9 mm/CTL) prices were assessed at INR 66,900/t ($719/t) on 14 April, marking a w-o-w decrease of INR 600/t ($6/t) from INR 67,500/t ($725/t) on 7 April. These assessments are ex-Mumbai for the distributor-to-dealer segment and exclude 18% GST.

Market update

Market sentiments remained subdued this week as overall trading activity slowed down. Demand stayed weak to moderate across regions, with buyers purchasing only to meet immediate requirements and avoiding any fresh or bulk procurement. On the raw materials front, coking coal prices dropped by $7/t w-o-w, falling to $255/t as on 10 April from $262/t on 3 April, adding further downward pressure on sentiment.

Supply conditions remained mixed across regions. In the north, a trader informed Bigmint, “Availability in the market remains tight and inventory levels across the chain have been depleting steadily, “though this supply shortage has failed to push prices higher due to the lack of buying momentum.”

In the west, “older inventory at the trader level has led to a price drop”, sources informed Bigmint. South India, however, appears relatively better placed, with a participant saying, “There are no supply constraints as of now. One one mill might shut down for maintenance, but that should not affect supplies significantly.”

Overall, the combination of sluggish demand, softening raw material prices and cautious market participation has kept prices stable to marginally lower this week.

Additional updates

Import volumes: India’s bulk imports of HRCs touched 171,332 t as on 10 April. Around 129,851 t of additional cargoes are expected by early-May.

Export volumes: India’s bulk exports of HRCs touched 14,378 t as on 10 April. Around 35,500 t of additional cargoes are expected.

Outlook

With neither buyers nor sellers willing to make aggressive moves, the market remains in a wait-and-watch mode. Mills are reportedly planning to revise prices upward in the coming week, which could shift market dynamics, though whether this translates into actual transactions will depend on how buyers respond. Overall, the interplay of a supply-short market, need-based demand, and softening raw material costs has kept prices largely stable this week, with the near-term outlook hinging on mill pricing actions and potential revival in buying interest.

Leave a Reply