- Steel mills resist second coke price hike amid high stocks and weak margins

- Falling coking coal costs weaken case for further price increases

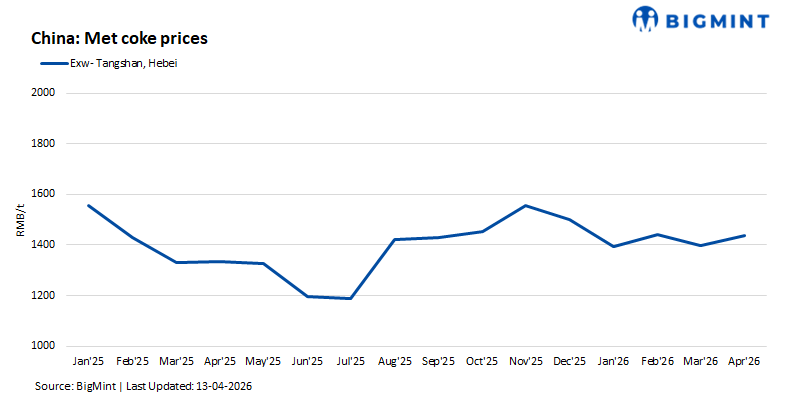

Mysteel Global: China’s independent producers of metallurgical coke are meeting resistance from their steelmaker customers to accept another increase in prices for met coke after the mills had conceded a round of price hikes only a week ago, Mysteel Global has learned. A rise would be the second this month but as of Friday, the mills were still pushing back, leaving the proposal in limbo.

The coke producers this week had proposed another round of price hikes – Yuan 50/tonne ($7.3/t) for wet-quenched coke and Yuan 55/t for dry-quenched coke – identical in size to those the mills had agreed to only on April 1, as Mysteel reported.

One key factor behind the determined resistance of the steelmakers is the comfortable inventory levels of met coke at their works.

As of April 9, the 247 blast furnace (BF) mills regularly surveyed by Mysteel were holding combined coke inventories of 6.79 million tonnes, equivalent to 12.52 days of consumption – well above the annual average. This has reduced any feeling of urgency to restock and strengthened their bargaining position, according to market watchers.

At the same time, weak profitability in the steel sector has further dampened the mills willingness to accept higher coke prices. More than half of the surveyed mills are still operating at a loss while in contrast, the independent coke producers remain profitable, with average margins at around Yuan 40/t as of April 9, Mysteel data shows, despite a slight decline from the previous week.

Another key constraint is the lack of cost support. Prices of coking coal have continued to soften in recent weeks amid ample domestic supply and strong inflows of Mongolian imports, as reported. Lower raw material costs have expanded the coke producers margins, undermining the justification for further price increases.

“With falling input costs, the coke producers profitability has improved, weakening the case for additional price hikes,” a Shanghai-based analyst said.

Some coke producers have also shown they have limited confidence in winning a second price rise so quickly, viewing the proposal more as a defensive move to pre-empt potential price cuts from steelmakers rather than a reflection of strong market fundamentals.

Looking ahead, for the coke makers to achieve another price rise will depend on several key indicators.

The first is hot metal output. During March 3-9, daily output among the 247 BF mills averaged 2.39 million tonnes, up 19,900 tonnes on week. Continued increases could signal stronger coke demand and increase the mills willingness to accept higher prices.

The second is inventory levels of met coke at steel mills. Although stocks have declined for three consecutive weeks, they remain above critical levels. A further drawdown could tighten supply and support price negotiations.

Finally, demand for finished steel will be crucial, as this directly affects mills profitability. However, Mysteel expects limited improvement in the near term, as the supply recovery in finished steel continues to outpace demand, exacerbating the imbalance. A meaningful steel demand recovery is unlikely before May, sources noted.

Overall, despite attempts by coke producers to push for higher prices, ample inventories, weak steel margins, and soft raw material costs are likely to delay or even derail the second round of price hikes in the near term.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.

Leave a Reply