- Rising pellet prices squeeze sponge iron margins in Bellary

- Domestic melting scrap prices rise on global trends, limited availability

Sponge iron

Sponge iron prices in the Bellary cluster have declined by INR 200/t on a w-o-w basis, primarily due to moderate demand from steel smelters, as most had already secured sufficient volumes in the previous weeks. As per BigMint data, around 13,500 t of PDRI deals were recorded last week, while this week volumes have dropped to approximately 5,000 t as of 10 April.

This price correction is expected to impact the conversion margins of sponge iron manufacturers, as raw material costs continue to remain firm, thereby putting pressure on overall profitability.

Iron ore pellet prices for 6–20 mm (Fe 63%) have witnessed a slight increase of INR 200–300/t w-o-w, reaching around INR 11,300/t as of 10 April. The upward movement is largely attributed to the recent price revision by NMDC for April deliveries, which has supported market sentiment.

KSMCL conducted an auction for high-grade iron ore in which approximately 146,000 t of fines (Fe 61.37–61.90%) was booked in the range of INR 3,352–3,705/t. Additionally, around 90,000 t of lumps (10–40 mm, Fe 61.37–61.90%) was booked at INR 4,521–4,806/t.

Meanwhile, the auction for low-grade iron ore fines and lumps is scheduled for today, which is expected to provide further direction to the market depending on participation and price realisation.

Non-coking coal prices have remained largely stable, with a slight correction observed on a w-o-w basis. Currently, RB2 coal prices are hovering at around INR 11,100/t on an ex-Gangavaram basis, indicating a relatively balanced market with mild downward pressure.

Melting scrap

Melting scrap prices in Chennai have increased by around INR 500–700/t for HMS 80:20 grade, currently hovering at approximately INR 36,000/t as of 10 April. The rise is mainly driven by limited availability of material in the domestic market, with the current material mix in Chennai estimated at a scrap to sponge ratio of 70:30.

Meanwhile, imported HMS 80:20 scrap of Australian origin has also increased by about $14/t w-o-w to around $387/t CNF Chennai. However, no significant trading activity has been observed at the current price levels, indicating subdued buying interest.

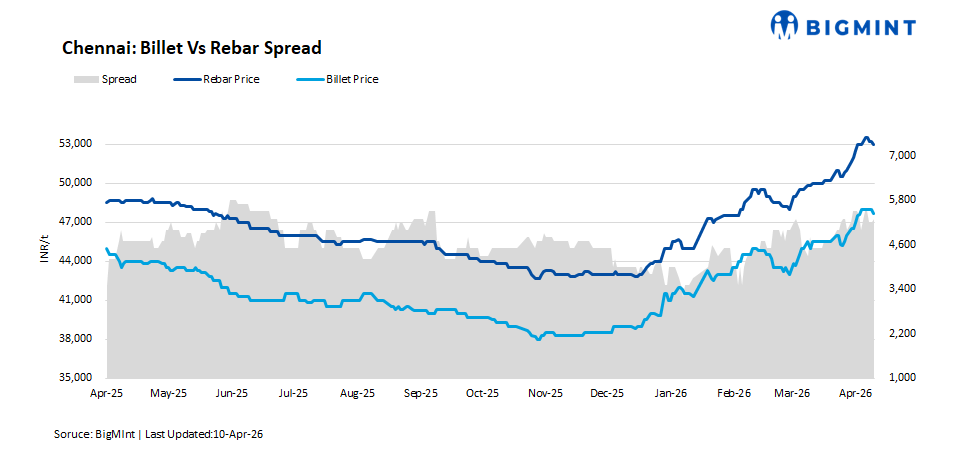

MS billet

Mils steel billet prices in south India, particularly in Chennai and Hyderabad, increased by around INR 400-500/t. The rise is mainly attributed to higher raw material costs, especially melting scrap, amid steady demand from the finished steel segment.

Additionally, the conversion spread from billet to rebar widened significantly compared to previous weeks. The current spread is hovering at around INR 7,000-7,500/t for MS billet to rebar (12–25 mm) on an ex-works basis.

Rebar

Induction route rebar prices in Hyderabad increased by around INR 500–700/t w-o-w, reaching INR 52,000/t ex-Hyderabad as on 10 April. Prices remain supported on strong demand from both project and retail segments.

Current inventory levels remain low at around 5-7 days, while material movement and order bookings are reported to be healthy, particularly in the Hyderabad region.

Meanwhile, blast furnace route rebar prices are hovering at around INR 61,000/t for both Hyderabad and Chennai markets. The current gap between induction route and blast furnace route is around INR 9,000/t exw basis.

Leading steel manufacturers continue to offer induction route rebars in the local market at prevailing price levels, although selective discounts are being extended in offers to attract buying interest of customers :

Outlook

Prices in south India’s steel market are expected to remain either stable or witness a slight correction. This is primarily due to the easing of geopolitical tensions in West Asia, which may lead to smoother trade flows and improved availability of key raw materials such as coal and scrap.

With logistics and supply chain disruptions likely to normalise, input cost pressures may soften, thereby limiting further upside in finished steel prices. Additionally, improved trading activities and better market liquidity could balance demand-supply dynamics, keeping prices range-bound with a marginal downward bias.

Leave a Reply