- Stronger flows from Indonesia, Colombia and Canada

- Atlantic basin witnesses logistics issues, freight pressure

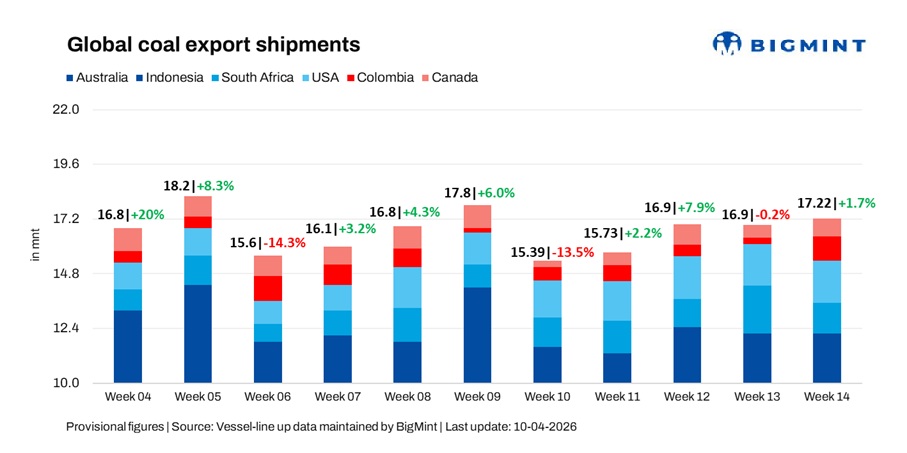

Global seaborne coal shipments rose 1.7% w-o-w to 17.22 million tonnes (mnt) in the week ended 3 April 2026. Gains were supported by stronger flows from Indonesia, Colombia and Canada, while Australia and South Africa faced pressure from maintenance and logistical constraints. US shipments remained largely stable.

Country-wise trends

Port & shipper-wise trends

Pacific flows remain supported by steady Asian demand

- Australian shipments were led by Newcastle (2.23 mnt), Gladstone (1.40 mnt) and DBCT (0.61 mnt), with Japan (1.39 mnt) and China (0.94 mnt) as key destinations. Glencore supported supply with 1.01 mnt.

- Indonesian shipments were led by Taboneo (1.25 mnt) and Samarinda (0.89 mnt), with India (2.35 mnt), the Philippines (0.88 mnt) and China (0.76 mnt) as key buyers.

- Canadian shipments were led by Roberts Bank (0.43 mnt) and Prince Rupert (0.17 mnt), with Japan (0.18 mnt) and China (0.17 mnt) as key destinations. Elk Valley Resources supported supply with 0.16 mnt.

Atlantic flows show mixed momentum

- South African shipments were routed via Richards Bay (1.35 mnt), with India (0.61 mnt) as the key destination.

- US shipments were led by Norfolk (0.56 mnt) and New Orleans (0.50 mnt), with India (0.36 mnt) and the Netherlands (0.24 mnt) among key buyers.

- Colombian shipments were driven by Puerto Nuevo (0.61 mnt) and Puerto Bolivar (0.41 mnt), with the Netherlands (0.32 mnt) as a key destination, while Carbosan supported supply with 0.67 mnt.

Coal freights to India muted

Coal freights to India remained muted, with thin cargo availability and cautious market participation weighing on sentiment. While some support was seen from steady enquiry, fluctuating bunker prices and uneven vessel availability continued to keep rates under pressure.

Outlook

BigMint expects coal flows to remain mixed in the near term. Indonesian shipments may stay firm, while Australian volumes could remain capped by maintenance. Atlantic performance is likely to remain uneven, with logistics constraints and freight dynamics continuing to shape trade flows.

Leave a Reply