- China ranks first in global Mn alloys output and is world’s largest Mn ore importer

- Lower Chinese alloy output may weigh on ore demand

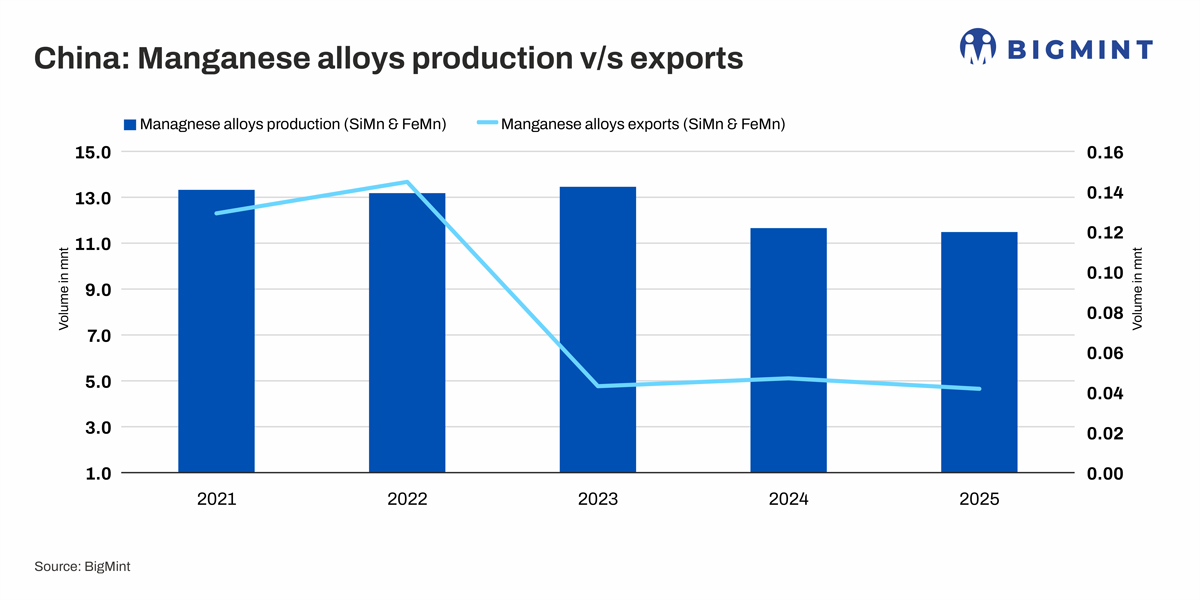

China’s manganese alloys production stood at around 11.5 mnt in CY’25, down about 2% y-o-y from 11.75 mnt in CY’24, according to BigMint data, with volumes declining from 13.3 mnt in CY’21. China continues to anchor the global manganese alloys market, but are recent moves toward coordinated output cuts indicative of a broader shift toward supply-side discipline? This is critical to assess given China’s position as the world’s largest producer, with any change in its output strategy carrying direct implications for global supply, pricing and trade flows.

Effective 1 April, Chinese producers have initiated voluntary production curbs estimated at around 221,000 t per month, or roughly 2.6–2.7 mnt on an annualised basis, according to market sources. The cuts are aimed at rebalancing an oversupplied market, curbing aggressive price competition and stabilising alloy realisations.

Given China’s dominant position in the global manganese alloys market, any coordinated supply response carries broader implications. If sustained, the cuts are likely to tighten global availability and reduce export pressure. China’s manganese alloys exports have already declined from 0.13 mnt in CY’21 to around 0.04 mnt in CY’25, reflecting a shift toward domestic market balancing.

Manganese alloy production cuts in China likely to weigh on ore demand

With alloy output curbs underway, manganese ore procurement is expected to moderate, which could ease cost pressures for alloy producers globally, including in India.

A reduction in China’s alloy production is likely to weigh on imported ore demand, potentially weakening miners’ pricing power in the seaborne market. China’s ore imports stood at around 33 mnt in CY’25, up 12% y-o-y from 29.4 mnt in CY’24, underscoring its dominant role in global trade flows. This may impact the overall tradeflows as China is world’s largest manganese ore importer.

However, any downside in ore prices is expected to be limited. Supply remains structurally tight, while steady underlying demand across key consuming regions is likely to provide support, preventing a sharp correction in the near term.

How could this impact the Indian manganese alloys market?

India, the second-largest producer and a key exporter of manganese alloys, is likely to mirror shifts in global supply dynamics. A reduction in China’s alloy output could redirect manganese ore cargoes toward India and Southeast Asia, improving spot availability across these regions.

However, increased availability does not necessarily translate into lower prices. Ore pricing will remain conditional, influenced by freight rates, grade specifications and long-term contractual linkages, which are likely to limit any sharp correction in landed costs despite softer demand from China.

Export conditions remain weak. Regulatory headwinds in Europe and subdued global demand have weighed on sentiment, raising the risk of higher domestic availability. This is increasing reliance on alternative export markets and a recovery in global prices to support margins.

Other producing regions, including Malaysia, South Africa and CIS countries, continue to play a secondary role in determining market direction. Malaysia benefits from relatively competitive power costs, while South Africa faces persistent power and logistics constraints that limit supply responsiveness. These regions remain dependent on prevailing price signals, with limited influence over global benchmarks, which continue to be driven by Chinese production trends that anchor global benchmarks.

In the near term, manganese alloy prices are expected to remain laregely unchanged with a firm bias, supported by elevated input costs and initial supply tightening. Over the medium term, the sustainability of China’s production discipline will be critical. A consistent and coordinated approach could support gradual market rebalancing, while uneven implementation may keep price volatility elevated.

To know more – join The 6th International Ferro Alloys Conference (IFAC 2026) which focusses on Fueling India’s Steel Surge: The Rising Importance of Ferro Alloys which will take place in Goa from 16–18 September 2026. Organized by the Indian Ferro Alloy Producers’ Association (IFAPA), with BigMint as knowledge partner.

Leave a Reply