- Refined lead production rises 1.6%, outpacing demand growth

- Market records third consecutive surplus of 70,000 t, reinforcing structural oversupply

- LME lead prices decline 5.3%, remains anchored near $2,000/t

Morning Brief: The global lead market remained in a state of managed surplus in 2025, as steady growth in refined production continued to outpace demand expansion. While the imbalance remained modest in absolute terms, the persistence of surplus conditions for a third consecutive year signals a structural shift in market dynamics.

This shift is being driven by the dominance of secondary, recycled lead, which now accounts for over two-thirds of global refined output. As a result, the market has effectively transitioned from a mine-constrained system to a recycling-driven one, where supply is more flexible and less responsive to price signals. This has allowed production to continue expanding even in a weakening price environment.

At the same time, demand growth has remained stable but capped, particularly in China, where traditional end-use segments are approaching maturity. As a result, even marginal surpluses have proven sufficient to anchor prices lower, reinforcing a structurally loose market.

Overall, the lead market is increasingly characterised by a low-amplitude but persistent imbalance, where incremental supply consistently exceeds absorption, exerting sustained pressure on prices.

Production growth steady, secondary supply anchors expansion

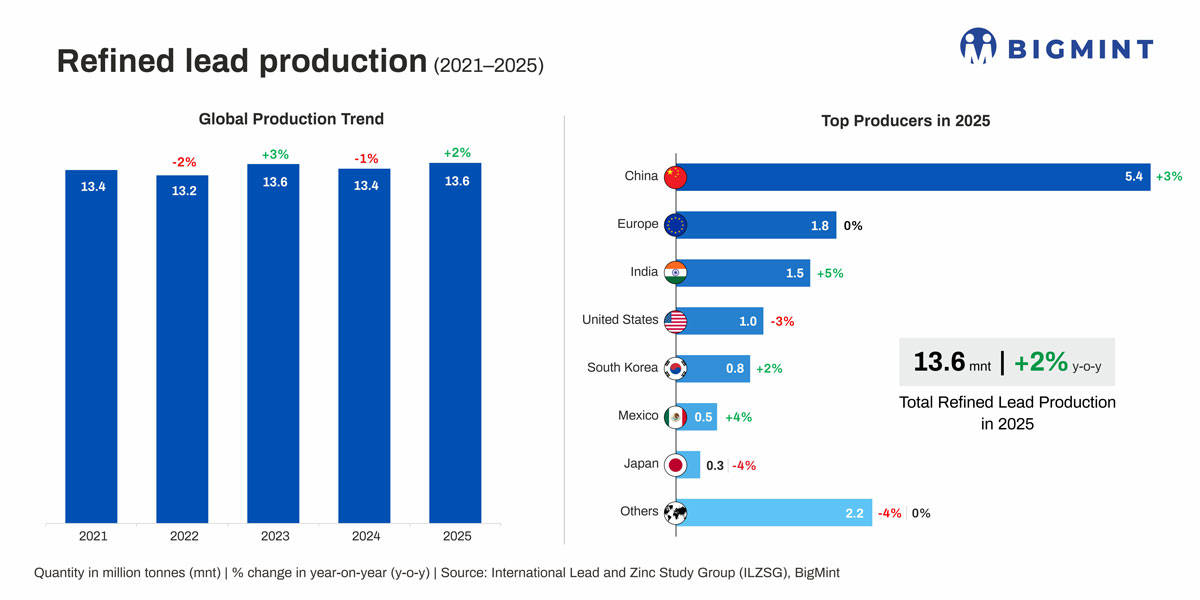

Global refined lead production increased by 1.6% y-o-y to 13,633 kt in 2025, supported primarily by expansion in secondary smelting capacity across key regions. Growth remained highly concentrated, with China and India accounting for the majority of incremental output during the year.

China retained its position as the dominant producer at 5,425 kt, contributing close to 40% of global supply, while India continued its structural growth trajectory with output rising to 1,534 kt. Additional gains were recorded in Canada and Mexico, reflecting capacity additions in recycling-based production systems.

In contrast, production declined across several mature markets, including the United States and Japan, while Kazakhstan recorded a sharp 27.3% contraction, representing the most significant single-country disruption during the year. Despite this, global output continued to expand, underscoring the resilience of secondary supply and the system’s ability to absorb supply shocks without tightening.

The divergence between mine and refined production trends remains notable, with mine output growing at a slower pace. This reinforces the decoupling of refined supply from primary resource constraints, with recycling rather than mining now acting as the primary driver of incremental supply.

Market balance remains persistently surplus

Global refined lead demand rose by 1.5% y-o-y to 13,563 kt in 2025, reflecting steady consumption across both developed and emerging markets. The United States led the recovery among major economies, while India and several smaller markets recorded healthy growth.

China, which accounts for approximately 40% of global consumption, saw demand increase by just 0.4%, highlighting the maturity of traditional demand segments such as lead-acid batteries. While emerging applications such as energy storage, data centres and electric vehicles continue to provide incremental support, these remain supplementary rather than transformative drivers of demand.

Despite this broad-based growth, refined production exceeded consumption for the third consecutive year, resulting in a surplus of 70 kt, compared to 61 kt in 2024. The persistence of surplus conditions, even amid supply disruptions, highlights the structural nature of the imbalance.

This indicates that incremental supply, particularly from secondary sources, is consistently outpacing demand absorption, reinforcing a surplus-biased equilibrium where even small imbalances exert downward pressure on prices.

Trade and inventory dynamics signal underlying shifts

Global trade flows and inventory patterns in 2025 point to deeper structural changes within the lead market. China’s net imports of refined lead declined sharply from 126 kt in 2024 to 52 kt, while imports of lead concentrates increased significantly, reflecting a shift towards domestic refining and greater control over the value chain.

This transition indicates that China is increasingly internalising value addition, importing raw materials while reducing reliance on refined metal imports, with potential implications for global trade flows as surplus material is redirected toward other regions.

Inventory dynamics further reinforce this interpretation. While overall reported inventories saw only a modest increase, underlying trends diverged, with consumer stocks rising significantly even as exchange inventories declined. This suggests precautionary stocking behaviour rather than a meaningful acceleration in end-use demand.

At the same time, price sensitivity to visible inventory movements remained high, with large inflows into exchange warehouses triggering sharp price corrections during the year. This highlights the role of exchange stocks as a key signalling mechanism in an otherwise structurally balanced market.

Prices remain under pressure on oversupply concerns

Lead prices continued to soften in 2025, with the LME average declining 5.3% y-o-y to $1,963/t, extending the downward trend observed since 2021. Price movements during the year remained relatively contained, even as other base metals experienced stronger upward momentum. This divergence indicates that lead is increasingly decoupling from the broader base metals cycle, with its pricing driven more by internal structural dynamics than by macro tailwinds.

The relatively tight price range also suggests subdued volatility and limited speculative participation, reinforcing the view that the market is being driven primarily by fundamentals. At the same time, periodic inventory-driven shocks led to short-term price corrections, particularly during phases of visible stock accumulation.

As a result, prices remained anchored around the $2,000/t level, with limited upside in the absence of stronger demand growth or meaningful supply-side adjustments.

Regional shifts and structural realignment continue

The global lead market is undergoing a clear structural realignment in terms of production geography and supply dynamics. Growth remains concentrated in emerging markets, particularly China and India, while output in developed regions continues to decline due to ageing infrastructure, higher costs, and regulatory constraints.

At the same time, the increasing dominance of secondary production is shifting the industry away from a mine-led model toward a recycling-driven system. This transition is reducing the importance of primary supply constraints and enabling more stable, but structurally higher, levels of output.

In addition, the by-product nature of lead production, which is closely linked to zinc, silver and other metals, further reduces supply responsiveness to lead-specific price signals, reinforcing the structural rigidity of supply.

Outlook

We expect the lead market to remain oversupplied in the near term, with the surplus projected to widen further as refined supply continues to grow modestly. Demand growth is expected to remain subdued, with gains in developed markets and emerging economies likely to be offset by weaker consumption trends in China.

Prices are therefore expected to remain anchored near current levels, reflecting a structurally balanced but surplus-prone system. Any sustained recovery would require either a meaningful acceleration in demand or a slowdown in secondary supply expansion, both of which appear limited in the near term.

Over the longer term, increasing adoption of energy storage systems and continued reliance on lead-acid batteries may provide incremental support to demand. However, the dominance of recycling and the by-product nature of supply are likely to keep the market anchored in a low-volatility, surplus-biased equilibrium.

Leave a Reply