- Pellet exports in FY’26 down sharply y-o-y

- Downtrend continues post FY’24 peak levels

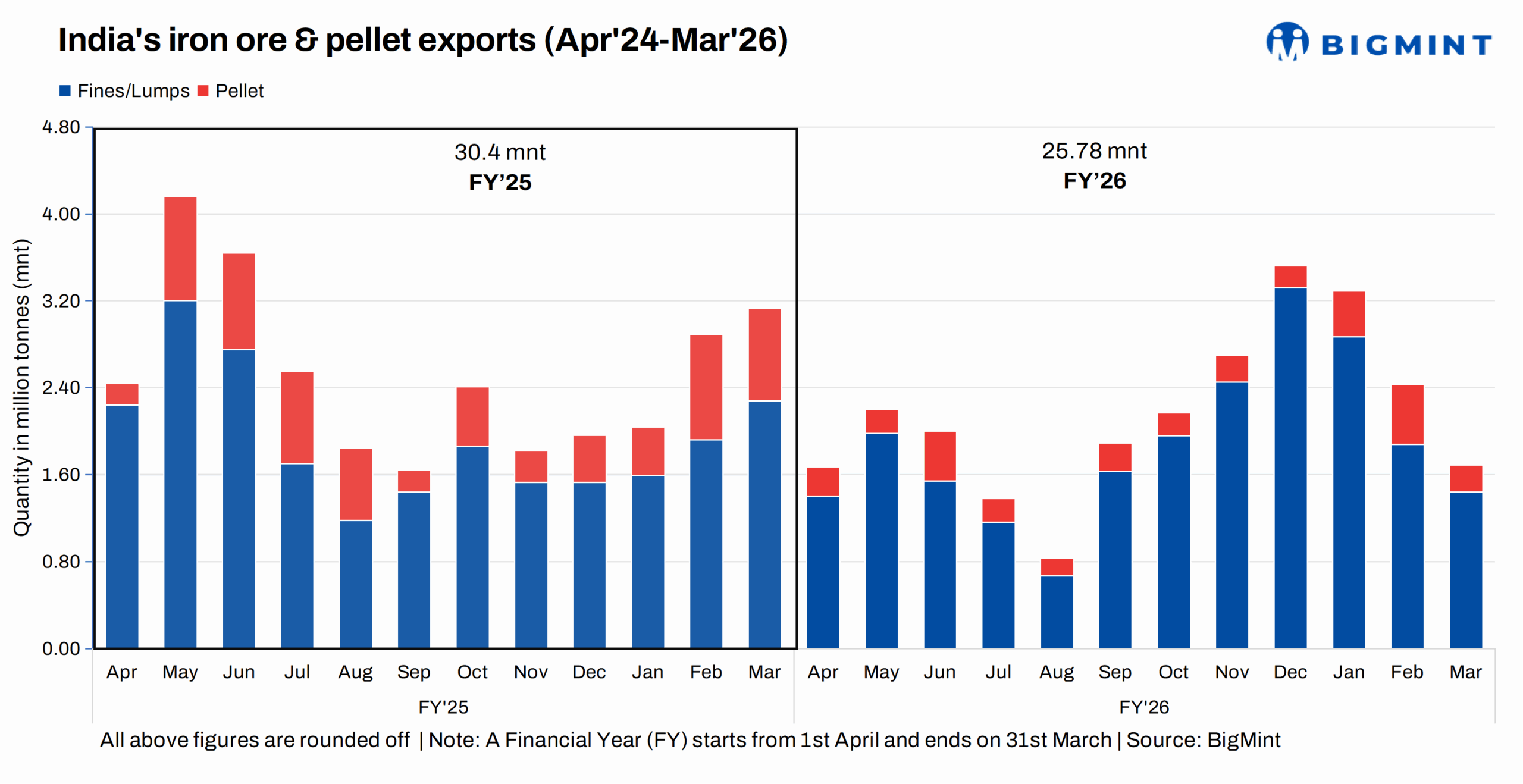

India’s iron ore and pellet exports decreased by 4.61 million tonnes (mnt) y-o-y in FY’26, with total exports declining to around 25.78 mnt against 30.39 mnt. Interestingly, the exports are in a downward trend post the FY’24 high at 47 mnt, as per BigMint data.

Exports of iron ore fines and lumps were recorded at nearly 22.31 mnt, while pellet sales overseas were assessed at 3.47 mnt in the just-concluded fiscal. In FY’25, iron ore exports stood at 23 mnt and pellets over 7.3 mnt. Thus, iron ore exports registered a drop of 3% while pellet down sharply by 53% on a yearly basis.

Country & company-wise exports

India’s exports of the key steelmaking raw materials (including pellets) were predominantly to China which accounted for over 90% of exports in FY’26, although volumes reduced to 24.21 mnt compared with 27.8 mnt in the preceding fiscal. Malaysia and Indonesia were among the other importers but volumes were relatively small receiving 0.85 mnt and 0.32 mnt respectively.

Among Indian suppliers, Rungta Mines was the top exporter of iron ore, at around 8.78 mnt, while Vedanta grabbed the distant second spot with total iron ore exports at around 3.01 mnt in FY’26. While on the next stairs OCL Iron and Steel and KIOCL stood at around 1.41 and 1.36 mnt respectively.

Factors pressuring iron ore, pellet exports

Chinese steel production falls: As India’s largest importer of iron ore, China’s demand determines the trajectory of the market. China’s demand for iron ore and pellets dwindled on declining steel production in FY’25. The country produced 924 mnt of crude steel between April’24 and February’25, a decrease of 1% y-o-y, as per data published by the World Steel Association (WSA). Additionally, portside inventories rose to around 167 mnt in closing FY’26 compared with 137 mnt in end- March FY’25, limiting fresh buying interest and keeping imports largely need-based.

Global iron ore prices drop: Average global iron ore prices declined in CY’25 amid weak Chinese and broader market sentiment, dampening export incentives for Indian suppliers. Benchmark Fe 62% fines prices averaged around $102/t CFR China, down from $109/t in CY’24. From CY’26 onwards, the global benchmark has shifted towards Fe 61% amid grade deterioration. Continued softness in prices, along with widening discounts on lower-grade fines in the seaborne market, has made domestic sales more attractive than exports for many Indian producers.

Rising domestic demand diverting export volumes: India’s iron ore exports were increasingly constrained by strong domestic demand in FY’26. Crude steel production rose by 11% y-o-y to 168 mnt, while steel consumption increased by 7% to 162 mnt, reflecting healthy end-use demand. This led to higher domestic absorption of iron ore, reducing exportable surplus.

Higher domestic realisations for pellets: Sources informed BigMint that domestic pellet ex plant realization in Odisha averaged over INR 8,200/t in FY’26, while pellet export ex plant realisation averaged around INR 6,200-6,400/t; against INR 7,500/t in FY’25, while pellet export ex plant realisation averaged around INR 6,800/t. The realization gap was increased to INR 1,400/t in FY’26 against INR 1,100/t in FY26 with higher domestic demand. Therefore, higher domestic realizations naturally discouraged exports.

Outlook

Steel production cuts in China and a weak global outlook are likely to keep India’s iron ore exports under pressure. Sluggish demand from China amid a property slowdown, coupled with geopolitical tensions and trade barriers, may limit buying interest. Easing global prices could further reduce export viability, prompting Indian suppliers to prioritize domestic demand.

Leave a Reply