- Higher output driven by irrigation gains in northern regions

- Export decline reflects timing dynamics rather than demand erosion

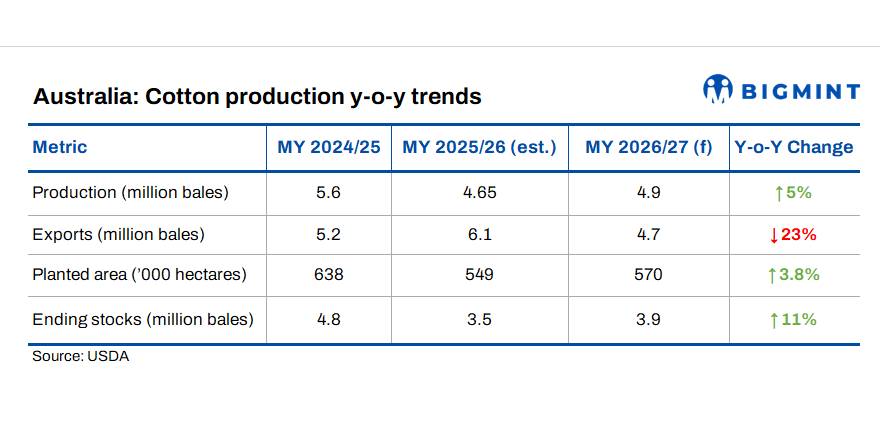

Australia’s cotton market is entering marketing year (MY) 2026/27 with a cautiously balanced outlook, as a modest recovery in production is offset by tightening export availability and persistent cost pressures. Output is forecast at 4.9 million bales, up from 4.65 million bales in MY 2025/26, supported primarily by improved irrigation water availability in northern New South Wales and Queensland. However, reduced water levels in southern regions are expected to cap further expansion, keeping overall growth moderate.

Planted area is projected to rise to 570,000 hectares, largely driven by irrigated acreage, while dryland cotton remains constrained due to yield variability and weaker price signals. Subdued global cotton prices and a stronger Australian dollar continue to weigh on farmgate realisations, limiting growers’ planting incentives despite favorable water conditions in key regions.

Cost pressures and currency weigh on planting decisions

Rising input costs, particularly for diesel and nitrogen-based fertilisers, remain a critical concern. Energy market disruptions have pushed production costs higher, disproportionately impacting dryland cotton, where margins are already thin. At the same time, currency appreciation has reduced export competitiveness, placing additional downward pressure on domestic prices.

Export volumes fall on lower carryover supply

Exports are forecast to decline to 4.7 million bales, down from 6.1 million bales in MY 2025/26. The drop is largely attributed to trade timing effects, as the previous year’s elevated shipments were supported by a larger carryover crop. With lower production in MY 2025/26, exportable surplus in the early months of MY 2026/27 is expected to tighten. Overall, the market reflects a transition phase, where stable production is insufficient to offset cyclical trade and macroeconomic headwinds.

Leave a Reply