- Supramax rates fall amid limited fresh inquiries

- Rising bunker prices push up Capesize rates

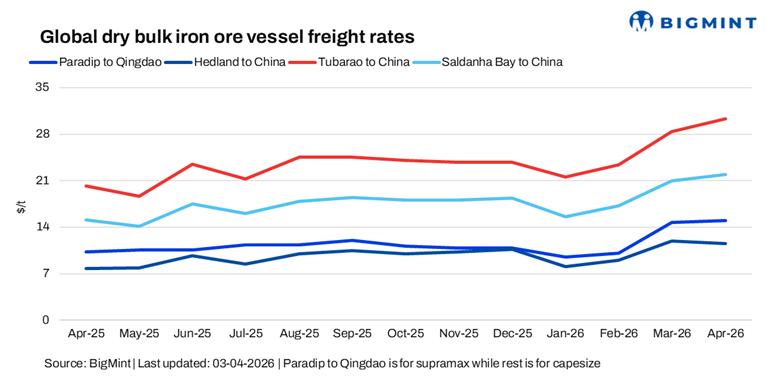

Dry bulk iron ore freights exhibited mixed trends w-o-w. Supramax rates from India softened amid cautious buying activity and limited fresh cargo enquiries. However, Capesize rates on key routes edged higher, supported by rising bunker prices, improving long-haul iron ore fixtures, and relatively tighter vessel availability in select regions.

Cargo volumes remained subdued, while vessel availability continued to build, exerting downward pressure on freight rates. At the same time, elevated bunker prices eroded earnings, keeping overall market sentiment weak. Activity further slowed as participants largely remained out of the market due to the Good Friday and Easter holidays, resulting in limited fixtures.

A shipbroker stated, “Supramax (Paradip-Qingdao) sentiment remains cautious, with indications around $15/t; however, a recent fixture of $15.4/t cargo failed to conclude. Market participants are largely in a wait-and-watch mode, as expectations of a potential easing in geopolitical tensions could lead to softer bunker prices and downward pressure on freight rates.”

Route-wise updates

Market highlights

- Baltic index surges w-o-w: The Baltic Dry Index surged 52 points w-o-w to 2,066 on 2 April, supported by firming Capesize earnings amid increased long-haul iron ore fixtures, tightening vessel availability in key basins, and improved overall chartering activity across the dry bulk market. Additionally, Capesize gained 112 points to 3,086, while Supramax rose by 19 points to 1,224.

- Bunker prices gain w-o-w: Bunker prices gained by $31/t w-o-w to $890/t on 3 April, supported by higher crude oil prices, supply tightness in key bunkering hubs, and firm demand from the shipping sector.

- DCE iron ore futures decline w-o-w: Iron ore futures on the Dalian Commodity Exchange (DCE) declined by around RMB 13.5/t ($2/t) w-o-w to RMB 799.5/t ($116/t) on 3 April, pressured by weakening steel margins and cautious market sentiment amid macro uncertainty and rising energy prices, which weighed on broader metals markets.

- Brent crude futures remain volatile: Brent crude oil (June 2026 contract) was last assessed at $109.03/bbl on 2 April, with no further updates as markets remained closed for the Good Friday holiday. The market remained volatile throughout the week.

Outlook

Iron ore freight rates are expected to remain largely stable with a soft bias in the near term, as weather-related disruptions and Easter holidays continue to limit market activity and delay fixtures. Additionally, a prevailing wait-and-watch approach amid broader market uncertainty is likely to keep sentiment cautious, with any upside capped until cargo volumes improve and trading momentum resumes.

Leave a Reply