- Limited availability prevents sharp price fall

- Weak trading activity limits price discovery

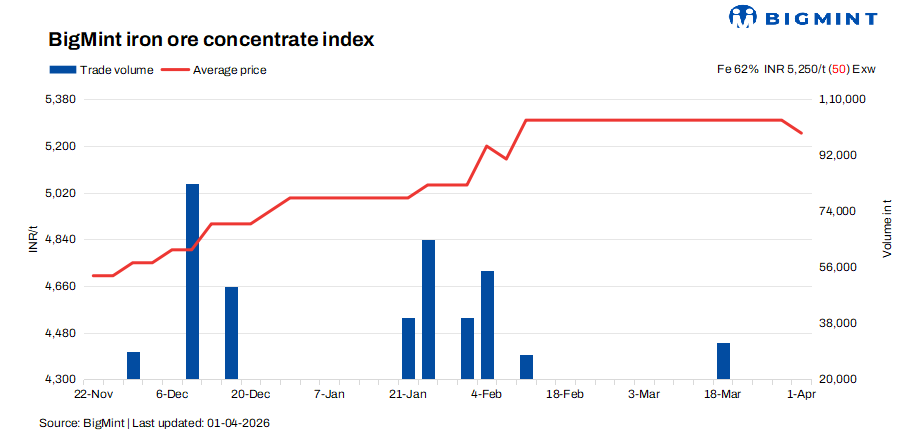

Iron ore concentrate prices witnessed a mild yet notable correction this week, slipping by INR 50/t amid a widening bid-offer disparity across the region. As per BigMint’s latest bi-weekly assessment, Fe 62% concentrate prices eased to INR 5,250/t ($56/t) ex-works, down by INR 50/t ($0.5/t) since 28 March. Despite the price adjustment, market activity remained largely muted, with no fresh deals recorded during the week. Sellers continued to prioritise dispatches of previously concluded orders, while refraining from new transactions due to financial year-end constraints and cautious market positioning.

The prevailing bid-offer gap has emerged as a key factor exerting downward pressure on prices. Buyers are adopting a conservative stance, quoting lower bids in anticipation of further softening, while sellers, though firm in intent, are compelled to revise expectations in the absence of active trade. This disconnect has resulted in a temporary price correction rather than a sentiment-driven downturn.

Adding to the subdued tone, pellet prices have also come under pressure, particularly in the Raipur region, where producers have reduced offers in response to weak buying interest and volatility in the downstream steel segment. Meanwhile, iron ore prices in Odisha have remained largely stable, reflecting a balanced demand-supply equation but still influenced by fluctuations in finished steel prices.

Supply-side constraints, however, continue to provide an underlying cushion to the market. Ongoing maintenance shutdowns at several beneficiation plants have tightened material availability, preventing a sharper fall in prices. This restricted supply scenario is acting as a counterbalance to weak trading activity and is expected to support prices in the near term.

A Jabalpur-based seller informed BigMint, “We are currently focused on executing our existing orders. Given the overall market dynamics, prices are likely to rebound in the near term as they continue to draw support from adjacent sectors.”

Another supplier highlighted operational disruptions, stating, “Our plant remains under maintenance shutdown and will require at least another week to resume operations.”

From the demand side, buyers acknowledged the current stability but raised concerns over escalating input costs and logistical inefficiencies. A Jabalpur-based buyer noted, “While concentrate prices appear steady at present, steel prices are rising due to increased coal and energy costs, largely driven by ongoing geopolitical tensions.” He further emphasized the growing logistical challenges, adding, “There is a significant diesel shortage in the market, causing transportation delays. In some cases, hoarding of diesel has worsened the situation, disrupting supply chains and extending delivery timelines.”

Rationale

- Zero (0) trade was recorded in this publishing window receiving a 0% weightage.

- Eight (8) offers and indicative prices were heard, in which seven (7) are taken into consideration as T2 trades, receiving 100% weightage.

Factors supporting prices

- Pellet prices fall by INR 150/t ($2/t) in Raipur: PELLEX, BigMint’s bi-weekly domestic pellet (Fe 63%) index for Raipur, declined by INR 150/t ($2/t) to INR 10,650/t ($113/t) DAP on 31 March. The dip was mainly driven by buyers restricting purchases to need-based deals ahead of the fiscal year-end. However, the correction came despite a noticeable improvement in buying interest over the weekend, which resulted in some active deal closures by steelmakers.

- Odisha iron ore prices remained steady w-o-w: BigMint’s Odisha iron ore fines (Fe 62%) index remained steady week-on-week at INR 5,850/t ($63/t) ex-mines as of 28 March. The stability was supported by a few bulk deals concluded toward the close of the fiscal year. However, despite ongoing trading activity, market sentiment stayed cautious, influenced by mixed trends in the downstream steel sector.

Outlook

Iron ore concentrate prices are expected to remain firm in the near term, supported by rising steel prices and persistent supply-side constraints. Limited availability due to ongoing maintenance shutdowns and logistical disruptions is likely to keep downside risks restricted. However, the pace of any upward movement may remain gradual, as buyers continue to adopt a cautious, need-based procurement strategy amid cost pressures and market uncertainty.

Leave a Reply