- High supply, weak power demand to exert pressure on prices

- Geopolitical risks, global prices to prevent sharp downside

Mysteel Global: China’s thermal coal market may come under downward pressure this week, after a week-long rebound driven by phased restocking from non-power sectors ahead of scheduled railway maintenance. However, external factors, including ongoing conflicts in the Middle East, are likely to limit the downside, suggesting only mild price corrections going forward.

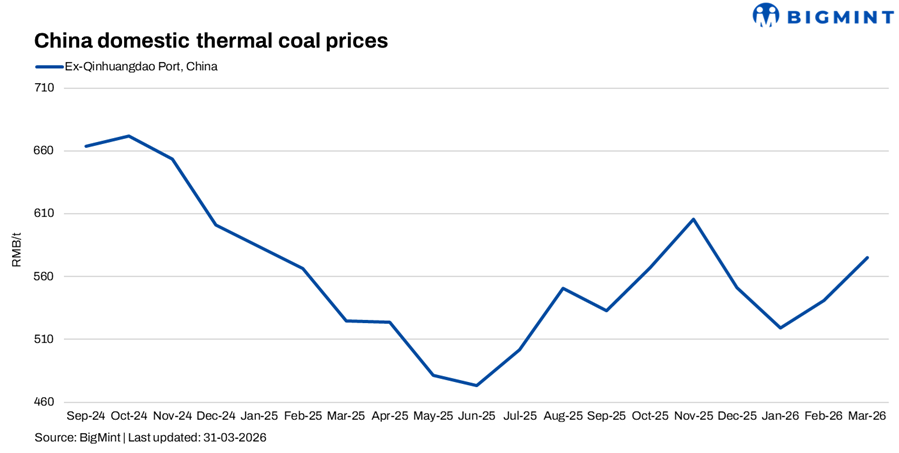

Last week (23-27 March), thermal coal prices at northern transfer ports increased strikingly. As of last Friday, Mysteel’s assessment of benchmark 5,500 kcal/kg NAR grade reached RMB 761/tonne (t) ($110/t) FOB with VAT, up by RMB 24/t on week.

The price rally was mainly driven by increased buying from cement and chemical producers, which are in the middle of the traditional March-April peak season. Meanwhile, some coastal users shifted part of their procurement from imported coal to domestic supply, offering a price floor for the domestic market.

However, the spot buying could be unsustainable, as recent coal purchases by non-power sectors were seen as a proactive move ahead of the 30-day maintenance of the Daqin railway set to start from 1 April, indicating their potential halts in buying in the following period.

Moreover, coal-fired power plants could stay away from the spot coal market as well, as their current coal burn is at a moderate level amid their relatively low operations. During 20-26 March, average daily coal consumption at 493 power plants surveyed by Mysteel stood at 4.01 million tonnes (mnt), down 1% from the previous week. Their total coal inventories fell by 2.1% to 90.49 mnt as of 26 March, equivalent for 22.5 days, still indicating ample supply.

On the supply side, production from major producing regions has been largely at high levels. According to Mysteel data, capacity utilisation rate across 462 thermal coal mines nationwide stood at 92.9% over 20-26 March, up 1.8 percentage points on week, while average daily output increased by 2% on week to reach 5.61 mnt.

In Inner Mongolia and Shaanxi, most mines maintained normal production last week, although some reduced or halted output after completing monthly targets. Improved procurement activity from downstream users supported sentiment, resulting in weekly price gains ranging from RMB 20-50/t.

However, several dozen mines slashed prices last weekend, as transactions slowed after recent price upticks. Some miners anticipated further price cuts this week in a bid to stabilise their sales.

At northern ports, market activity appeared somewhat stalemated in the second half of last week, with only limited transactions concluded for high-quality, low-sulphur coal. Meanwhile, port inventories continued to build, and sentiment softened toward the end of the week, leading to a narrowing of price increases. As of 26 March, total coal stocks at the eight Bohai-rim ports (excluding Huanghua) monitored by Mysteel stood at 27.13 mnt, up 4.5% on week.

In the seaborne market, international thermal coal prices remained broadly stable. Although some tenders for imported coal were released, actual procurement remained cautious.

In South China, the lowest bid for Indonesian 3,800 kcal/kg coal was heard at RMB 533/t, CFR with VAT, down RMB 9/t on week. Meanwhile, the price spread between imported and domestic coal narrowed, with Indonesian 3,800 kcal/kg coal bids at around RMB 549/t compared with approximately RMB 560/t for equivalent domestic coal delivered from northern ports.

Mysteel assessed Indonesian 3,800 kcal/kg NAR coal at $60/t FOB Kalimantan as of Friday, almost unchanged from a week prior.

The conflict between Iran and the US-Israel persisted, with some signs pointing to its further escalation and signalling the elevated global energy prices. The latest Newcastle coal futures on the International Exchange have climbed above $140/t, hovering near the highest levels since October 2024. Against this background, domestic prices are unlikely to fall quickly despite weakened buying.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.

Leave a Reply