- Suppliers quote high prices while holding dispatches

- Selective buying continues for extrusions and taint tabor

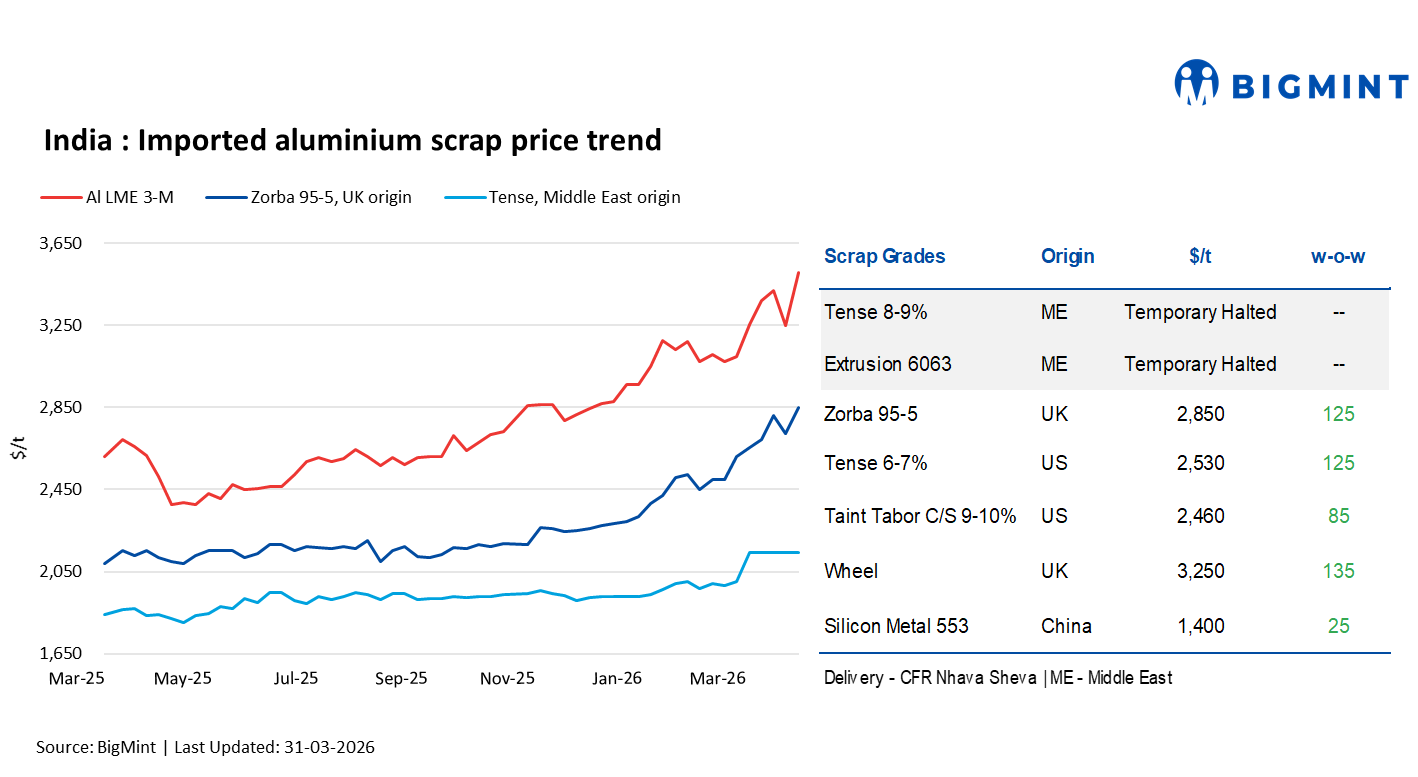

India’s imported aluminium scrap prices recorded a week-on-week increase as of 31 March 2026, tracking firm trends on the London Metal Exchange, supported by ongoing geopolitical tensions, exchange rate fluctuations, and tightened global supply conditions.

As per market assessment for CFR Nhava Sheva deliveries, UK-origin Zorba 95-5 scrap rose by $125/t w-o-w to $2,850/t, while US-origin Tense 6-7% scrap increased by $125/t w-o-w to $2,530/t. Meanwhile, UK-origin Wheel scrap prices climbed by $135/t w-o-w to $3,250/t.

LME aluminium climbs w-o-w

Three-month aluminium closing prices on the LME increased by 8.6% w-o-w to $3,530/t on 30 March, up from $3,251.5/t on 23 March. Meanwhile, LME aluminium inventories declined by 2.1% or 9,000 t over the same period, easing from 427,675 t to 418,675 t.

Aluminium prices surged on 30 March, climbing around 6% to nearly $3,492/t on the LME, driven by Iranian strikes on key Middle East production facilities, including Emirates Global Aluminium and Aluminium Bahrain. The escalation heightened concerns over supply disruptions in a region accounting for about 9% of global output, further strained by ongoing logistical challenges around the Strait of Hormuz. As a result, prices approached multi-year highs amid strong bullish sentiment and rising risk premiums, with continued volatility expected due to potential supply constraints and delayed recovery in the near term.

Market scenario

The imported aluminium scrap market is witnessing mixed conditions, impacted by supply constraints, global disruptions, uncertain demand, and currency fluctuations. The Indian rupee’s sharp depreciation against the US dollar has added pressure on import costs, while LME aluminium prices surged on the morning of 30 March, widening the gap between asking prices and bids. Despite this, overall demand remains slightly slower compared to levels observed two weeks ago.

Selective buying continues for certain grades such as extrusions and taint tabor scrap, while most other variants are resisting elevated LME-linked prices. Reputed and branded manufacturers are continuing to procure imported scrap, but purchases are not at full capacity, and domestic supplies are not being relied upon fully. Suppliers are quoting high prices but are holding back on dispatches amid uncertainty over whether these price levels will sustain.

Market participants noted that no offers were received from suppliers after LME aluminium spiked nearly 6% d-o-d on Monday, following Iranian strikes on key Middle East production facilities, including Emirates Global Aluminium and Aluminium Bahrain. Global disruptions, including supply concerns from major producing regions and logistical challenges around key export hubs, are further intensifying market caution. Even suppliers in the US are reportedly confused due to anxious buyer inquires, adding to the uncertainty.

Domestically, aluminium prices have risen sharply following LME trends, and scrap prices remain elevated due to acute shortages of casting-grade material such as Tense scrap. Secondary producers are facing procurement challenges, leading to cautious buying and reduced operating rates. Many customers and traders are holding back amid fears of potential price drops, though domestic pricing is expected to remain stable at least through Q2.

Overall, the imported aluminium scrap market remains highly volatile, driven by tight global supply, LME price trends, currency fluctuations, and cautious buying behaviour. Market participants are closely monitoring global disruptions and supply dynamics while adopting their procurement strategies to navigate this uncertain environment.

Chinese silicon prices

According to BigMint, China-origin silicon metal 553 prices increased w-o-w by $25/t to $1,400/t from $1,375/t on a CFR Nhava Sheva basis.

Outlook

Imported aluminium scrap is expected to remain firm as geopolitical tensions in the Middle East and tight global supply continue to influence prices. Selective buying for high-demand grades is likely to persist, while overall demand may remain cautious amid elevated price levels and exchange rate fluctuations. Domestic prices are anticipated to hold through Q2, supported by constrained scrap availability, and any further disruptions at key global production hubs could drive prices even higher.

Leave a Reply