- Absence of fixtures amid uncertainty in market

- Weak sentiment due to higher bunkers, geopolitical tensions

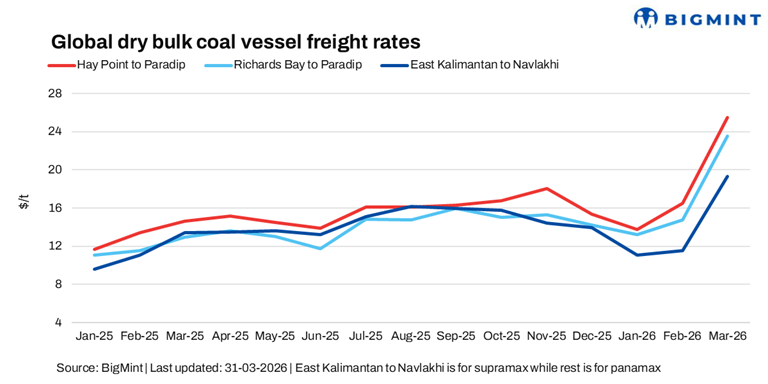

Coal freight remains soft w-o-w, with rates declining across key routes, while South Africa-India remains an exception, showing a slight w-o-w increase. Market activity continues to be subdued, with limited fixtures and a cautious, wait-and-watch approach seen among participants.

Weak cargo availability-particularly on the Indonesia-India route have weighed on rate levels, preventing any meaningful upside. Although firmer bunker prices offer some cost-side support, they have not been sufficient to offset the impact of muted demand and thin trading volumes.

A shipbroker stated, “Market uncertainty is keeping freight rates under pressure, with fixtures remaining tentative and lacking firm momentum.”

In the Indian Ocean and Middle East regions, sentiment remains weak to neutral, pressured by scarce cargo flows and geopolitical uncertainties. Overall, coal freight rates continue to face downward pressure, with isolated gains unable to shift the broader soft market tone.

Heightened market uncertainty continues to weigh on freight rates, keeping them under sustained pressure. Market participants remain cautious, with limited confidence in rate direction, leading to subdued fixing activity. As a result, most fixtures are being concluded on a tentative basis, with hesitancy on both sides preventing any firm upward momentum.

Outlook

In the near term, coal freight rates are expected to remain under pressure amid weak cargo availability and cautious market participation. While firmer bunker prices may offer some support, the lack of fresh demand is likely to limit any meaningful upside, keeping the overall sentiment soft with only occasional route-specific improvements.

Leave a Reply