- Surging HRC capacity to fuel transition to value-added products

- Shift aligns with Beijing’s emphasis on higher-margin production

Data Deep Dive: China’s steel industry is increasingly moving away from construction-driven long products towards flat steel, laying the foundation for producing higher, value-added grades, as the country reorients its economy towards advanced manufacturing.

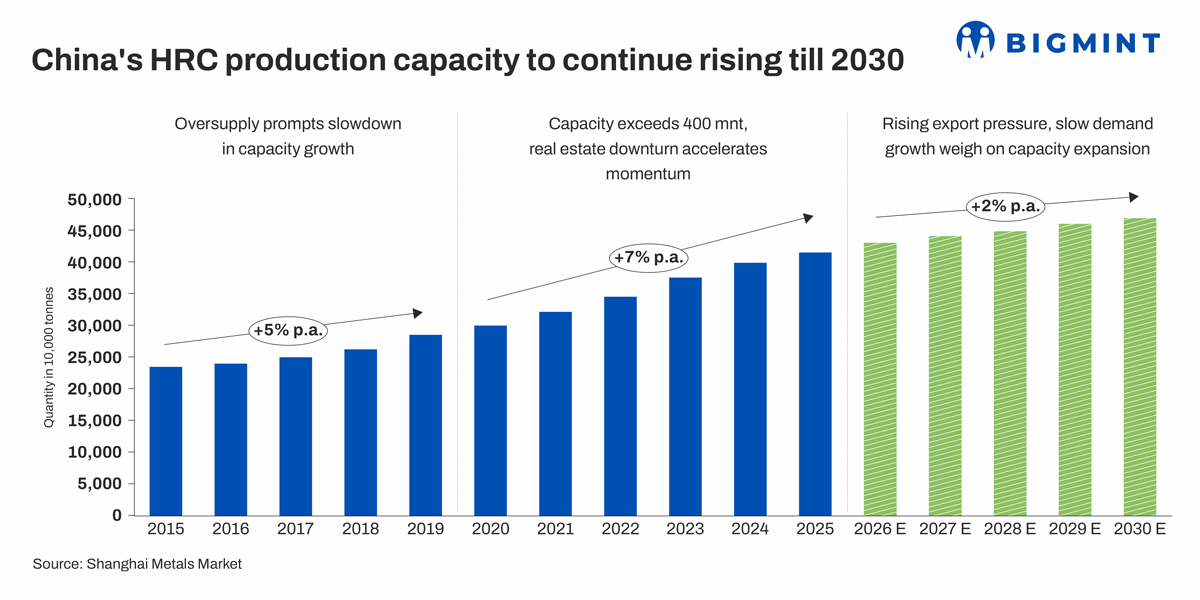

According to data from Shanghai Metals Market (SMM), China’s HRC capacity surged by almost 40% to 410 mnt by end-2025 from 300 mnt in 2020. Annual capacity growth is estimated at a rapid 7% over 2020-25. Although expansion is expected to slow to 2% in the next five years, the peak is yet to be reached. Capacity expansion may finally wind down in 2030.

Accordingly, data obtained from the National Bureau of Statistics and Langesteel also shows that hot-rolled coil (HRC) production has surpassed rebar since 2024. HRC output increased by 24% to 223 million tonnes (mnt) in 2025 from 179 mnt in 2021. Conversely, rebar production decreased by 26% to 186 mnt compared to 252 mnt over the same period.

This divergence coincides with the onset of the property debt crisis in 2021, sparked by the introduction of the “three red lines” policy – borrowing limits aimed at curtailing the heavy debt burden in the real estate sector.

Flat steel output rises as manufacturing takes lead

The shift in production mix aligns with the evolving steel consumption patterns in China, marked by weakening demand from real estate, rising industrial activity, and a broader push by policymakers to upgrade China’s manufacturing base.

From 2021, machinery began to overtake building construction as the primary driver of steel consumption. According to BigMint’s analysis, the share of machinery increased to 28% in 2025 from roughly 20% in 2010.

Manufacturing contributed 25% of China’s gross domestic product (GDP) in 2024, as per the World Bank. While this marks a steep contraction from 2011’s 32% (attributed to the expanding share of the services industry), China’s share is much higher than the worldwide average of 15%.

Strong manufacturing growth reinforces demand for flat steel

Strong growth in key manufacturing sectors has supported increased demand for flat and value-added steel.

To illustrate, exports of mechanical and electrical products climbed higher by 24% y-o-y to $420 billion in January-February 2026, according to China Daily. Rapid industrialisation and urbanisation across emerging economies have allowed China to diversify its export base, reducing reliance on traditional markets such as the US and the EU, where import restrictions have been tightening.

Moreover, in 2025, China remained the global leader in the automotive segment, with both production and sales reaching new highs. New energy vehicles (NEV) drove robust momentum, with sales rising 28% y-o-y to 16.5 million units, according to the China Association of Automobile Manufacturers (CAAM). A further rise of 15% y-o-y to 19 million units is expected in 2026, boosting demand for steel products such as advanced high-strength grades used in vehicles.

Shipbuilding has also emerged as a major source of flat steel demand. China accounted for 69% of global new shipbuilding orders and 56% of vessel deliveries in 2025, according to Mysteel Global. This has supported the consumption of heavy plate and specialised flat steel products.

Similarly, China’s transformer boom, with production capacity reaching more than half of global volumes, is expected to drive demand for cold-rolled grain-oriented (CRGO) steel, a grade of electrical steel used in transformer cores and inductors.

Besides this, HRC demand has strengthened even beyond China. For example, as per SMM data, China’s HRC exports climbed 30% y-o-y to 29.88 mnt in 2024, accounting for nearly one-third of the total. However, while increasing safeguard measures in importing regions pushed down volumes by 18% to 24.44 mnt in 2025, HRC exports still comprise a substantial 20% share.

Transition towards value-added steel accelerates

The latest phase of China’s steel evolution is the shift towards higher-grade, value-added products. While sharp HRC capacity growth has generated concerns of supply outpacing demand, BigMint believes that mounting HRC supply will enable increased upgrade towards higher-grade, specialised products.

This is because HRCs act as a key substrate for downstream processing to create speciality grades such as automotive-grade steel, electrical steel used in motors and transformers, and high-strength and lightweight alloys.

This transition also aligns with Beijing’s policy focus on “anti-involution” and “quality over quantity”: moving away from volume-driven growth towards higher-margin products and technological capability. China’s 2025-2026 steel industry work plan targets around 4% annual growth in value addition, alongside technological upgradation. Commodities highlighted as requiring focus include high-performance bearing steel, gear steel, high-temperature alloys, and tool and die steel.

This industrial transformation is closely aligned with the country’s 15th Five-Year Plan, which outlines its economic strategy till 2030. The plan prioritises industrial innovation and technological leadership, driven by – as Xi Jinping termed – “new quality productive forces”.

Growth engines include advanced manufacturing, clean energy and electrification, aerospace and shipbuilding, and high-end equipment and machinery. Policy support has also been specified for space tech, biotechnology, and quantum technology.

The transition is further supported by China’s dominance in critical materials, such as rare earth processing and magnet production, aluminium smelting, and copper refining. The integration of these with steel production will enable rapid scaling of high-end manufacturing and support the upward shift of the steel value chain.

Outlook

The decline of long steel, the rise of flat products, and the push into value-added grades together signal a structural transformation in China’s steel industry. However, even as China upgrades its steel mix, overall domestic demand growth will remain slow, given that the share of construction steel in total production remains significant.

We expect steel production to decline modestly again in 2026, as construction-oriented longs output continues to shrink as producers redirect resources to manufacturing flats. Demand recovery will hinge on how fast producers adapt to the evolving demand mix, particularly the shift towards manufacturing-led consumption and higher value-added steel requirements.

Leave a Reply