- Higher coking coal costs and rising import parity are supporting domestic met coke prices

- Weak pig iron and steel demand is limiting further price increases

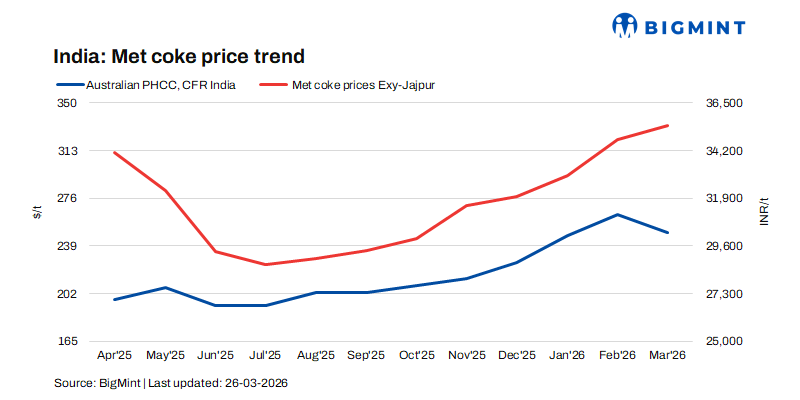

India’s blast furnace (BF)-grade metallurgical coke prices displayed a mixed trend week-on-week as of 26 March 2026, reflecting regional supply dynamics and cost pressures.

According to BigMint’s assessment, BF-grade coke (25-90 mm) prices in eastern India rose by INR 1,000/t to INR 36,000/t ex-Jajpur, supported by tighter availability and firmer offers from suppliers. In contrast, prices in western India remained stable at INR 31,000/t ex-Gandhidham, indicating balanced supply-demand conditions in the region.

Meanwhile, foundry-grade coke (+90 mm) prices also held steady at INR 36,000/t ex-Rajkot, as demand from casting units remained largely unchanged.

Market activity in eastern India remained limited but firm in sentiment. A seller concluded a deal for approximately 17,500 tonnes of metallurgical coke at INR 36,500/t ex-works, suggesting that suppliers are attempting to push for higher price levels.

Market participants attributed the firmness in offers primarily to geopolitical uncertainties and depreciation of the Indian rupee, which have increased import costs and strengthened domestic pricing sentiment. However, despite higher quotations circulating in the market, fresh transactions at elevated levels remain limited.

Rising import costs sustain domestic price floor

Import parity continued to influence domestic coke pricing. As per BigMint’s assessment, Indonesian-origin BF coke (65/63) was assessed at $285/t CFR India, marking a $5/t w-o-w increase. Market participants highlighted limited offers in the market. The rise in import prices has strengthened the cost floor for domestic suppliers, reducing the likelihood of price corrections in the near term.

On the raw material front, Australian premium hard coking coal prices increased by $14/t w-o-w to $236/t FOB, reflecting stronger global demand and supply-side tightness. The continued increase in coking coal costs has elevated production expenses for coke producers, thereby limiting their ability to lower coke prices despite weak downstream demand.

China market signals add to global cost support

Global market developments also provided indirect support to coke pricing sentiment. China’s coking coal market remained broadly stable, with spot prices registering marginal gains amid active auction participation.

In parallel, major Chinese coking plants proposed the first round of coke price hikes of RMB 50-55/t ($7-8/t). However, steel mills have yet to accept these increases, suggesting that negotiations between coke producers and steelmakers remain ongoing.

Weak Indian pig iron demand caps price upside

Despite firm cost support, downstream demand indicators remained subdued, particularly in the pig iron segment. Steel-grade pig iron prices in Durgapur declined by INR 100/t w-o-w to INR 37,500/t ex-works, reflecting cautious procurement by steelmakers and limited improvement in finished steel demand.

In the auction market, SAIL-Bokaro offered 7,000 tonnes of steel-grade pig iron on 25 Mar’26, with the entire quantity booked at a base price of INR 35,750/t. While this indicates healthy participation, the price remains sensitive to raw material costs and steel sector demand trends. Compared with the 12 Nov’25 auction, where 4,200 tonnes were sold at INR 31,450/t, prices have risen by INR 4,300/t, largely driven by higher input costs, including coking coal and coke.

Outlook

Indian met coke prices are expected to remain firm but largely range-bound in the near term, supported by higher coking coal costs, elevated import parity, and rupee depreciation. However, weak pig iron and steel demand may limit further price gains.

Leave a Reply