- Steel mills’ lean inventory strategies drive port stock build-up

- 86-mnt buffer remains, indicating limited risk of storage saturation

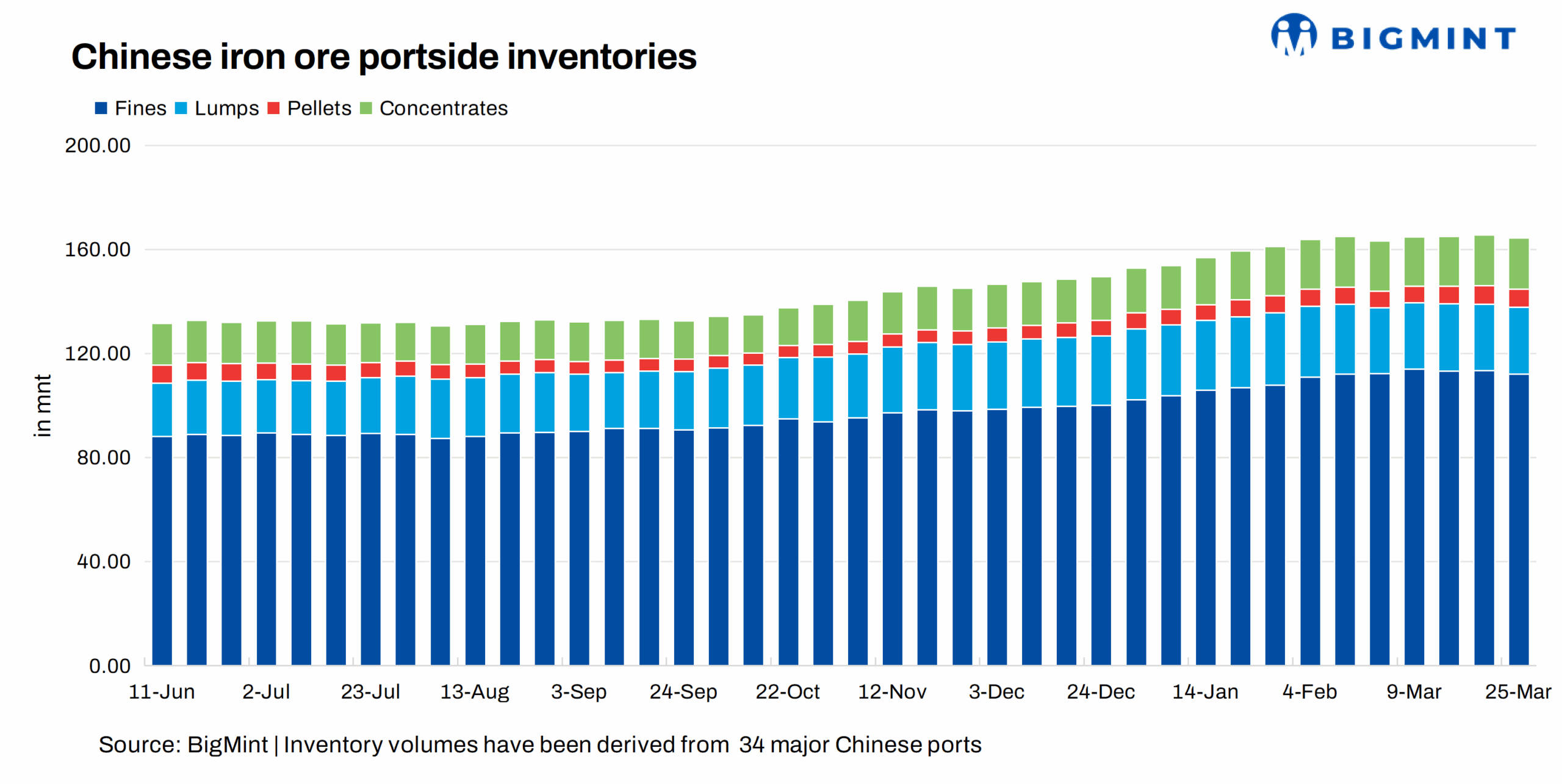

Mysteel Global: With China’s portside iron ore stocks surging to unprecedented levels over the past few months, concerns over port capacity limits have mounted. However, a recent analysis from Mysteel suggests that port inventories still have room to absorb further inflows, with no imminent risk of saturation.

The current accumulation cycle began in early August last year, when inventories across the 47 major Chinese ports under Mysteel’s tracking bottomed out at 142.2 million tonnes (mnt). During the eight months since, stocks have risen steadily, with the volume swelling by 37.3 mnt, or 26.2%, to a record high of 179.5 mnt on 12 March.

A closer look at the composition of this buildup reveals that trader-held inventories were the primary driver. Over the same period, iron ore port stocks held by Chinese traders at these ports climbed by 28.1 mnt to 118.5 mnt, accounting for over 75% of the total increase.

This reflects the sustained adoption of lean inventory strategies by domestic steel mills in recent years, the report points out. By keeping in-plant inventories low to preserve cash flow, mills have come to rely on abundant portside supplies underpinned by robust shipments from overseas mines. This approach has allowed them to shift potential inventory pressure upstream to the ports.

However, the accumulation of portside iron ore since August has been uneven across regions. Ports in South China, the Yangtze River region, and North China have experienced the most pronounced increases, with their stocks rising by 43.2%, 40.1%, and 32.9%, respectively, all well above the national average of 26.2%. In contrast, the increases in East China and Northeast China were modest at 15.1% and 15.4%.

These regional divergences are largely tied to local industry dynamics, the report notes. In South China and along the Yangtze River, rapid development of ore blending and beneficiation operations has accelerated stock growth. Meanwhile, in North China, robust demand for steel plates has given a boost to production activity among local mills, positioning the region as a preferred destination for inbound iron ore cargoes.

In Northeast China, however, production cuts among steelmakers have dampened their appetite for seaborne ore, making the region far less attractive for offloading.

Despite elevated port inventories, Mysteel believes that the risk of storage saturation remains limited in the near term. The combined storage capacity of the 47 major ports is estimated at approximately 265 mnt, leaving a buffer of around 86 mnt against the current inventory level of 179 mnt.

Additionally, looking at historical benchmarks, the sum of the peak inventory levels recorded at these 47 ports over the past five years totals 208 mnt. This also suggests that current stocks could still expand by roughly 29 mnt before hitting those historical highs.

Taken together, both total storage capacity and historical peak levels indicate that China’s portside facilities can accommodate additional iron ore inflows. Mysteel projects that imported iron ore inventories stockpiled at the 47 major ports could rise to around 200 mnt by the end of this year.

Note: This article has been written in accordance with a content exchange agreement between Mysteel Global and BigMint.

Leave a Reply