- Chinese mills prefer domestic concentrates

- Buyers resist, bids remain below offers

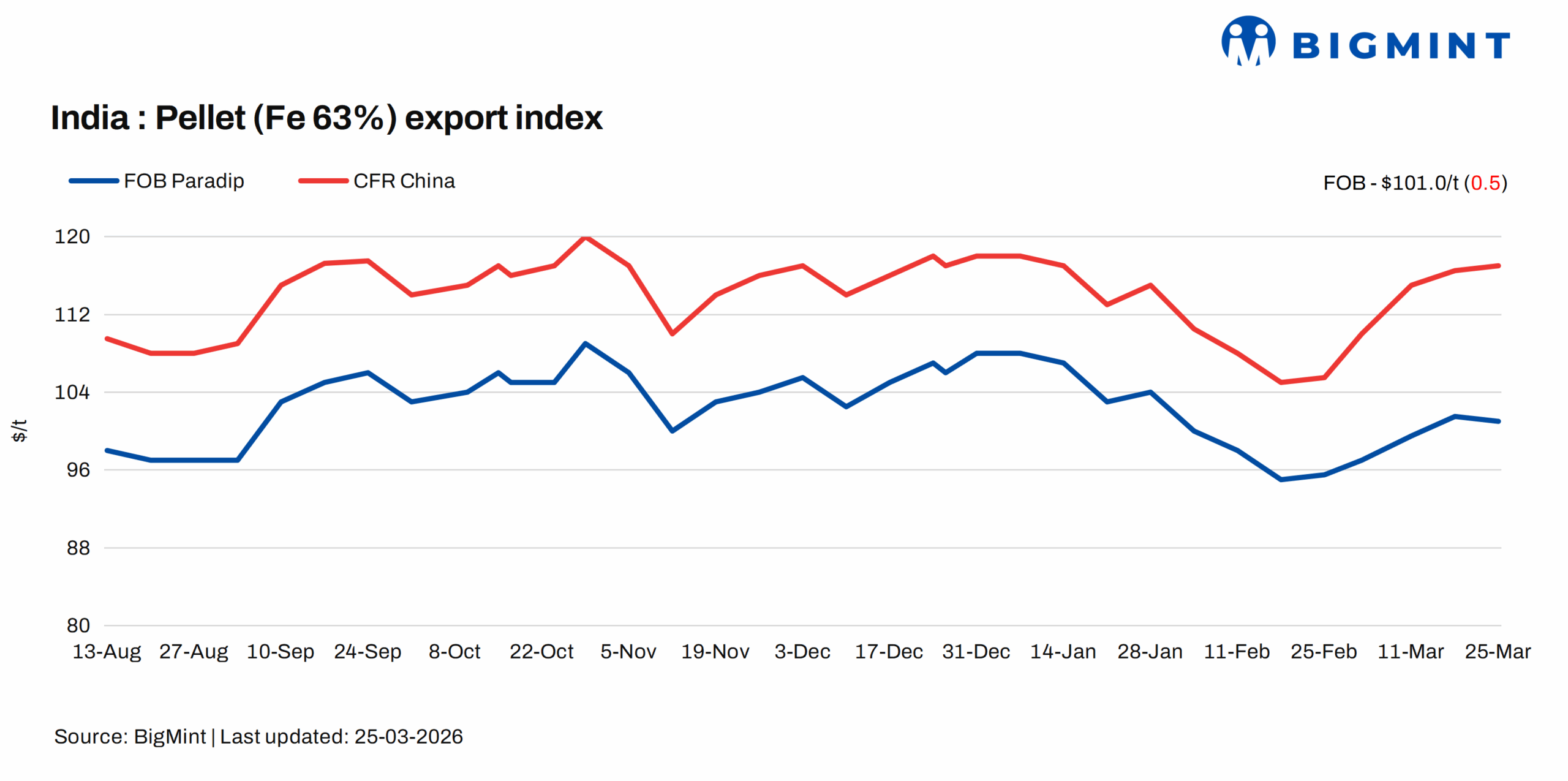

India’s pellet export market saw a slight correction this week, with prices dropping slightly on a w-o-w basis. However, the overall market tone remained cautious, as no confirmed export deals were recorded from the past couple of weeks.

Prices continued to draw support from firm global iron ore fines, even as high freight rates and limited vessel availability lifted CFR levels and dampened buyer interest.

Price and trades update

BigMint’s India pellet (Fe 63%, 3-3.5% Al) export index fell by around $0.5/t w-o-w to $101.0/t FOB east coast on 25 March against 18 March. No export deals were concluded from the east coast in this publishing window, with most buyers staying away from bidding.

The market participants said that pellet demand is weak in sea market amid the current geopolitical tension as Chinese mills are not interested to procure pellets at the current prices.

Market updates

Pellet export FOB prices slipped by half a dollar w-o-w, as demand continued to remain weak, with no fresh vessel activity reported over the past couple of weeks. Elevated portside inventories in China continue to act as a key pressure factor, significantly reducing the immediate need for imports and keeping buyers largely on the sidelines.

Market activity remained subdued, with a clear gap between seller expectations and buyer willingness. Most buyers are not bidding anywhere close to prevailing offer levels, highlighting persistent resistance amid squeezed margins and uncertain downstream demand.

An international trader shared, “Freight is the real concern right now; once you factor it in, CFR prices simply don’t work for most buyers. Mills are cost-effective for the raw material, and they are currently using the existing inventory or buying from the portside.”

On the supply side, sellers are largely adopting a wait-and-watch approach, with many shifting focus toward domestic markets where realizations remain relatively better compared to export parity. This has further limited aggressive selling in the export segment.

There is also a noticeable shift in procurement strategies among Chinese mills. “Mills are increasingly prioritising domestic concentrates over imported pellets and lumps to better manage costs,” an exporter noted.

Overall, the market continues to reflect a cautious and slow tone, though some participants expect that a few deals could start materialising in the near term as negotiations progress.

Domestic vs export market

Domestic pellet prices remained steady over the week, while export realizations moved higher, leading to a narrowing of the domestic-export spread. Export realizations (Fe 63%) decreased to INR 7,500/t on 25 March from INR 7,600/t on 18 March, reflecting a w-o-w fall of INR 100/t. In contrast, domestic realizations (Fe 62.5%) held firm at INR 8,850/t exw, showing a slight uptrend over the same period.

As a result, the spread between domestic and export prices narrowed to INR 1,350/t remaining largely stable.

Rationale

- No confirmed deal from India’s east coast was recorded in this publishing window for T1 trade and was allotted 0% weightage for today’s price calculations. Click here for the detailed methodology.

- Twelve (12) indicative prices were received, and nine (9) were considered for the calculation of the index and given a balance 100% weightage.

Factors impacting pellet exports

Chinese iron ore fines prices held firm w-o-w: The benchmark iron ore fines Fe 61% index remained stable w-o-w at $109/dmt CFR China on 24 March. Trading activity picked up despite stalled negotiations, with prices supported by higher hot metal output, supply concerns, and improved portside trades.

DCE iron ore futures price: Iron ore futures on the Dalian Commodity Exchange (DCE) for the May 2026 contract closed at RMB 816/t ($119/t) on 25 March, increased RMB 5/t w-o-w.

Outlook

The pellet export market is expected to remain muted with continued volatility in the near term. While demand remains subdued, some trade activity is possible only if freight cost cools off or the geo-political picture gets clearer.

Leave a Reply