- For 2026, proposed allocations represent a reduction of 110 mnt from 2025 levels

- Data shows RKAB quotas have often been exceeded, raising doubts about enforecement

Indonesia, the world’s largest nickel producer, is engineering a sharp contraction in mining output for 2026, proposing ore extraction quotas of 260-270 million tonnes (mnt) – well below both last year’s record 379 mnt and estimated domestic demand of around 330 mnt.

The move marks a significant policy pivot for Indonesia, which for years prioritised volume growth to feed a rapidly expanding domestic processing industry. Officials now appear to be deploying the country’s quota system as an active supply management tool, drawing comparisons to OPEC’s production discipline in oil markets.

Quotas and what they signal

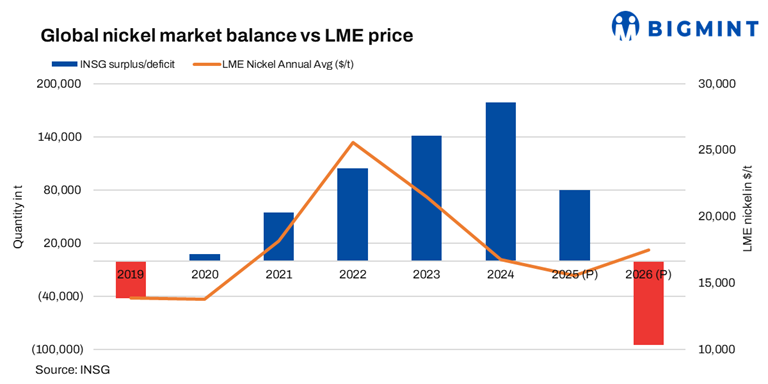

Indonesia allocates annual nickel mining rights through a permitting system known as RKAB – Rencana Kerja dan Anggaran Biaya – which sets company-level extraction ceilings. For 2026, proposed allocations represent a reduction of roughly 110 mnt from 2025 levels, a swing that market participants say would flip the market from a surplus of 70-80 mnt to a deficit of 60-70 mnt within a single year.

A 135 mnt policy-driven reversal in ore availability is an extraordinary intervention in a market that was already struggling with oversupply.

As of March, just over 100 mnt of the 2026 quota had been approved, suggesting Indonesia is deliberately phasing allocations rather than issuing bulk approvals upfront – a mechanism that would allow officials to adjust supply in real time based on market conditions.

Prices under pressure, policy responds

The recalibration follows two years of severe price weakness. London Metal Exchange nickel prices fell from nearly $30,000/tonne (t) in early 2023 to around $15,000/t-16,000/t by late 2024 – a collapse of nearly 50% – driven in large part by Indonesia’s own production surge.

The 2025 quota of 379 mnt, up sharply from 240-250 mnt in 2024, flooded downstream smelters and pushed global inventories sharply higher, compressing margins for nickel pig iron producers and stainless steel mills alike.

Supply chain consequences

The tightening is expected to reverberate across multiple segments of the global nickel supply chain.

Nickel pig iron producers, which use rotary kiln electric furnaces to process Indonesian ore into an intermediate alloy used in stainless steel, face the most immediate feedstock squeeze. Smaller, higher-cost smelters operating on thin margins are considered most vulnerable to output cuts.

Further downstream, China’s stainless steel industry – which absorbs an estimated 60-65% of Indonesian NPI output- could face higher input costs as ore availability tightens, though existing inventory buffers are expected to delay any immediate impact on flat product prices.

The battery supply chain faces a different but related pressure. High-pressure acid leach plants, which process lower-grade nickel ores into mixed hydroxide precipitate for electric vehicle batteries, may see feedstock competition intensify as broader quota restrictions limit available ore volumes.

Risks to the strategy

The policy’s effectiveness is not assured. Historical data shows RKAB quotas have at times been exceeded, raising questions about enforcement. Revenue pressures in nickel-producing provinces, which depend heavily on royalties and extraction fees, could generate political resistance to sustained output restrictions.

The Philippines, the world’s second-largest nickel ore producer, represents a partial offset, though analysts note its ore grades and processing infrastructure are materially weaker than Indonesia’s.

Perhaps the most consequential risk is one of signalling. Global nickel prices on benchmark exchanges are increasingly reactive to Indonesia’s regulatory cadence. Any indication that 2026 quotas may be revised upward – or that mid-year supplementary approvals are being considered – could rapidly unwind the market tightening Indonesia is attempting to engineer.

Is Indonesia’s quota discipline structural or merely tactical-and does the market fully recognise the difference? As supply becomes increasingly policy-driven, another question emerges: does the nickel market need a more robust price discovery mechanism as much as it needs supply control?

To explore these questions and decode the evolving nickel landscape, join us at BigMint’s India Non-Ferrous Week, in Mumbai on 9-10 June.

Leave a Reply