- Lifting of quantitative restrictions drives surge in met coke imports

- Indonesia emerges as largest supplier amid competitive landed costs

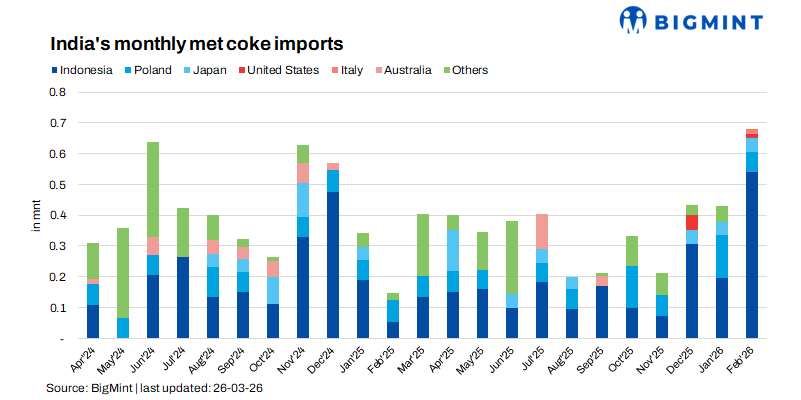

India’s metallurgical coke imports rose sharply to a record 0.7 million tonnes (mnt) in February 2026, according to data maintained by BigMint, reflecting a strong revival in overseas procurement. Import volumes increased 59% m-o-m and surged 906% y-o-y from 0.05 mnt in February 2025.

The significant jump largely indicates aggressive restocking by steelmakers and traders, following a prolonged period of restricted imports last year. Market participants accelerated purchases amid recent policy changes and evolving trade dynamics, which influenced sourcing strategies for metallurgical coke.

Policy shift revives import activity

Import demand had remained subdued for much of the previous year after the Indian government imposed quantitative restrictions on metallurgical coke imports to support domestic producers.

However, in January 2026, the government removed the quantitative cap on imports while imposing anti-dumping duties on shipments from six countries. This effectively reopened the market for higher import volumes.

Despite the duties, imports remained viable as international cargoes offered better price parity compared with domestic material, encouraging buyers to resume overseas bookings. Rather than suppressing imports entirely, the duties redirected procurement towards competitively priced or duty-free origins, leading to a shift in traditional trade flows.

Indonesia emerges as dominant supplier

Indonesia became the largest supplier of metallurgical coke to India, with shipments reaching 0.54 mnt in February, the highest level recorded since tracking began by BigMint. Imports from Indonesia rose 173% m-o-m, supported by competitive prices, geographical proximity to Indian ports, and relatively fewer trade barriers.

Indonesian met coke remained economically attractive even after the anti-dumping duties were implemented. Landed prices were heard in the range of INR 30,000-31,000/tonne (t), compared with domestic BF-grade metallurgical coke (25-90 mm) prices of around INR 32,300/t ex-Jajpur in eastern India.

The price advantage encouraged Indian steelmakers to increase procurement from Indonesian suppliers, with some buyers also front-loading purchases to secure supply amid global market volatility.

India’s coking coal imports fall to 1-year low in Feb’26

Lower coking coal imports, triggered by elevated prices, also prompted a shift to met coke imports, which appeared more cost efficient.

India’s coking coal imports declined 13% m-o-m to 4.4 mnt in February 2026, though remained higher by 10% y-o-y. This marks the lowest level in over one year, driven by cautious procurement by steel mills amid elevated prices.

The decline in February imports reflects booking decisions taken during December-January, when coking coal prices were rising sharply. BigMint’s PHCC index, CNF India, increased from $215.5/t in November to $232/t in December and further to $250/t in January, before rising to $260/t in February, marking multi-year high levels.

Mixed trends among other suppliers

Import trends from other countries were more varied. Shipments from Poland declined significantly to 0.07 mnt in February, down 52% m-o-m, likely due to higher landed costs and policy-related pressures following the anti-dumping duties.

Meanwhile, Italy re-entered India’s import basket with 0.02 mnt, marking the first shipment in FY’26 and the first recorded cargo since August 2018, indicating gradual diversification of supply sources. Imports from Japan remained steady at 0.04 mnt m-o-m, reflecting stable contractual supply and continued demand for higher-quality metallurgical coke from established producers.

Domestic production remains firm despite m-o-m dip

On the domestic front, India’s met coke production increased about 9% y-o-y to 47.56 mnt in 11MFY’26 (April-February), supported mainly by higher captive output from integrated steelmakers. Producers ramped up internal production to secure raw material supply for blast furnace operations and reduce dependence on imports.

However, production declined 8% m-o-m to around 4 mnt in February 2026, largely due to lower operating rates. Despite the m-o-m dip, output remained 4% higher y-o-y compared with 3.86 mnt in February 2025, supported by steady crude steel production and consistent blast furnace utilisation.

Improved utilisation of merchant coke ovens and stable demand from secondary steel producers also contributed to the overall rise in domestic output during the fiscal year.

Outlook

India’s metallurgical coke imports are expected to remain relatively strong in the next few months, supported by robust steel production and the removal of quantitative import restrictions. Indonesian cargoes are likely to continue dominating the import basket due to competitive pricing and logistical advantages.

However, import growth may moderate in the coming months as the market gradually adjusts to anti-dumping duties, evolving trade routes, and improving domestic production levels. Steelmakers may also adopt more balanced sourcing strategies, combining captive production with selective imports depending on price parity and availability in the global market. Higher shipping costs, fuelled by increased bunker prices in the face of the US-Iran conflict, may also weigh on imports.

Leave a Reply