- Sellers hold on to material amid falling LME, tightening supply

- Post year-end liquidity expected to improve market activity

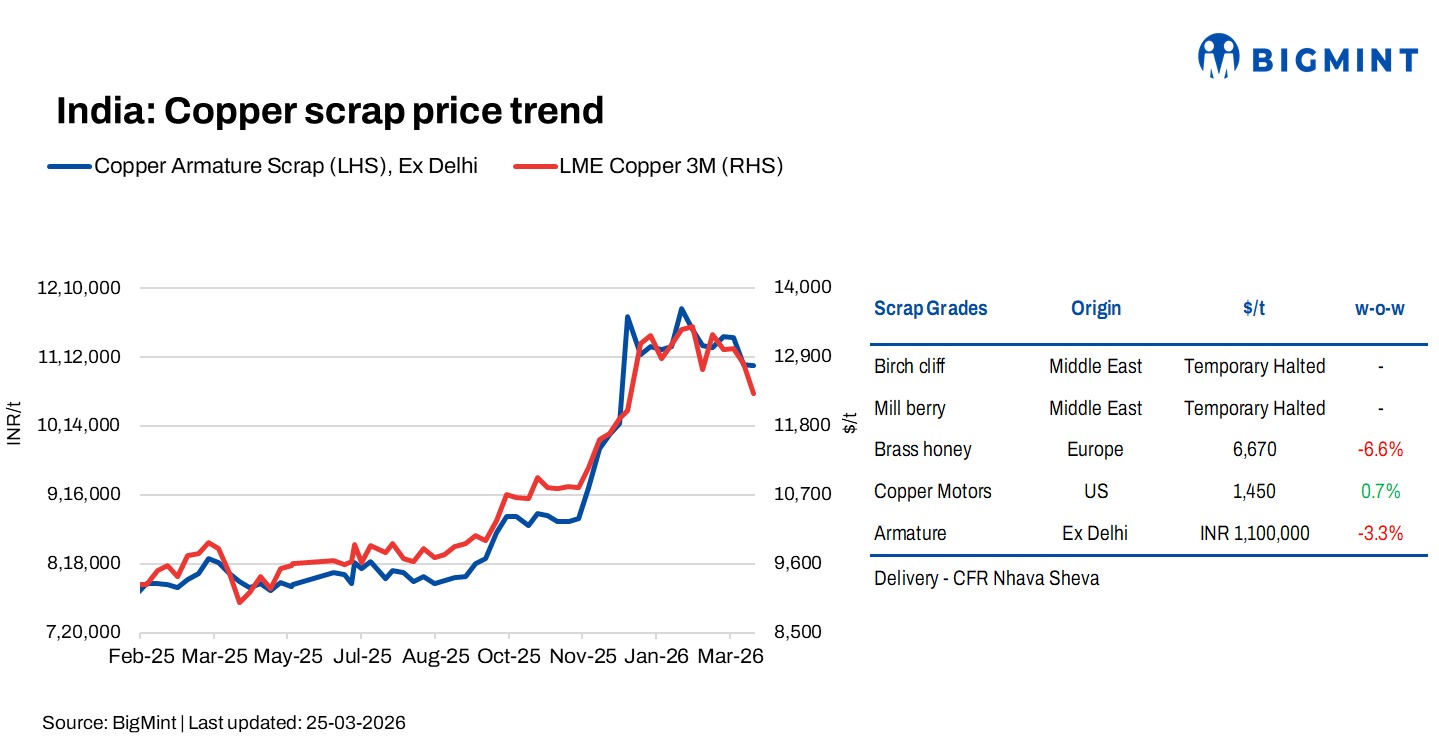

Copper scrap prices showed mixed trends within a narrow range in the week ending 25 March 2026, reflecting a balance between underlying supply concerns and cautious buying interest. While some regions witnessed a shortage of copper scrap, particularly for immediate requirements, this tightness appears to be more situational than structural.

According to BigMint’s assessment, copper armature scrap, ex-Delhi, was assessed at INR 1,100,000/t, down 3% w-o-w. In the imported scrap segment, Brass Honey from Europe was assessed at $6670/t CFR Nhava Sheva, down 6% w-o-w, while copper Motors scrap from the US stood at $1,450/t, 0.7% rise w-o-w.

Market scenario

Market participants indicated that buyers with urgent needs were willing to pay premiums, suggesting short-term supply pressure. However, this “shortage” was largely driven by strategic holding of material by scrap dealers and yard owners. With prices on the London Metal Exchange (LME) recently slipping below the $12,000/t mark, many sellers were reluctant to offload material at lower realisations, expecting a potential rebound. This temporarily restricted spot availability in the market.

At the same time, domestic scrap prices softened, with armature scrap reportedly declining to around INR 1,050,000/t. This further reinforces the cautious stance among sellers. Adding to this dynamic is the financial year-end factor. Several traders highlighted that while there is a need to liquidate inventory before closing books, destocking is being approached gradually due to ongoing payment delays and uncertainty around price direction. Many expect clearer payment cycles and improved liquidity after the year-end, which could normalise trading activity.

In the imported market (CIF Nhava Sheva), pricing remained largely stable with slight variations across grades. Millberry (EU origin) was heard at around a 3% discount to LME, Candy/Berry near 94%, Birch/Cliff (EU) at approximately 91.5%, Meatballs at about $2,350/t, and Motors mix (US) in the range of $1,450-1,500/t.

Some market participants stated “On the demand side, wire rod manufacturers have increased imports, primarily due to billing advantages, while regions such as Mandi Gobindgarh have been witnessing the emergence of small-scale copper units (500-600 t capacity), which is gradually supporting scrap demand”.

Outlook

In the next few weeks, the current artificial tightness may ease as sellers begin to release inventory following the financial year-end. If LME prices stabilise, scrap flows are likely to improve, leading to more balanced pricing. However, steady demand from downstream units and continued import activity should provide underlying support to the market.

Leave a Reply