- Muted buying interest continues to keep fixing activity limited

- Firm bunker prices offering underlying support to freight levels

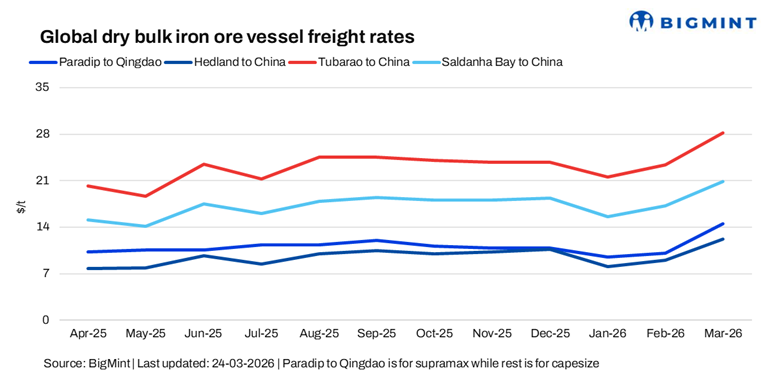

Dry bulk iron ore freight rates showed a mixed trend w-o-w across key basins, with relative resilience on select Pacific and South African routes, while Brazil declined amid softer sentiment. Weak FFA cues, thin tonnage demand, and limited fixtures across both Pacific and Atlantic, keeping market momentum subdued and largely rangebound.

A source mentioned, “Mixed market conditions persist as easing oil prices offer some cost-side relief, but sentiment remains cautious with fixing activity largely negligible. Limited cargo visibility and subdued chartering interest continue to weigh on momentum, keeping the market rangebound.”

“Sentiment is unlikely to shift overnight, as seaborne routes need to stabilize and prove consistently safe before confidence returns. With no confirmed ceasefire between Israel and Iran, vessel movement remains restricted and selective, with only limited flows (including crude, LNG, and LPG) gradually resuming. A meaningful recovery will only be visible once stranded vessels resume normal transit across key routes”, another source told.

Route wise updates:

Another source informed, “Freight sentiment is gradually softening across segments, except Panamax, with easing tonnage demand reflecting a demand-supply driven correction.”

Outlook

In near term, iron ore freight rates are expected to remain weak, weighed by weak FFA sentiment, limited fixtures, and thin tonnage demand. While bunker price volatility and geopolitical tensions may offer intermittent support, cautious buying interest and resistance to higher rate levels are likely to cap upside, keeping overall sentiment fragile.

Leave a Reply