- Imports decline 13% m-o-m as mills delay purchases

- Softening prices, improved supply keep sentiment cautious

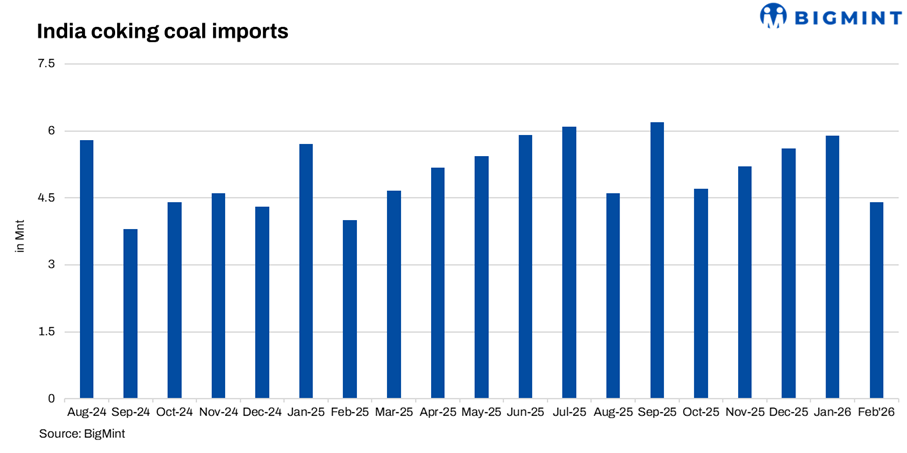

India’s coking coal imports declined to 4.4 million tonnes (mnt) in February 2026, down 13% m-o-m from 5.1 mnt in January but higher by 10% y-o-y compared with 4 mnt in February 2025, marking the lowest level in over one year. The drop reflects cautious procurement by steel mills amid improved supply conditions.

Why imports declined

PHCC prices surge since Nov, impacting booking decisions

The decline in February imports reflects booking decisions taken during December-January, when coking coal prices were rising sharply. BigMint’s PHCC index, CNF India, increased from $215.5/t in November to $232/t in December and further to $250/t in January, before rising to $260/t in February, marking multi-year high levels.

This reflects a consistent increase in FOB Australia prices from $197/t in November to $211/t in December, $233/t in January, and $247/t in February.

Elevated prices significantly impacted import economics, discouraging bulk bookings. Additionally, a weaker INR and firm freights added to cost pressures, making imports less attractive for Indian mills during the booking period.

Limited buying interest despite rising offers

Despite firming prices in December, buyer acceptance remained limited, with persistent bid-offer gaps. Indian mills were unwilling to match higher CFR offers ($230-238/t), resulting in restricted deal activity and delayed procurement decisions.

Supply disruptions initially supported prices, later eased

Weather-related disruptions in Australia during December also tightened supply while pushing prices higher. However, as supply conditions improved in January-February, along with muted Chinese demand during the Lunar New Year, sentiment shifted towards expected price corrections, leading buyers to defer purchases.

Shift from restocking to cautious procurement

After active restocking in earlier months, Indian steelmakers moved to a wait-and-watch strategy, focusing on inventory optimisation. Even as steel prices improved, mills avoided aggressive procurement due to high raw material costs and uncertain downstream demand.

Expectation of price correction delays buying: Despite high prices in early February, the market showed signs of softening toward the latter half, with FOB Australia declining to $237-243/t. This led buyers to adopt a wait-and-watch approach, delaying fresh purchases in anticipation of further corrections.

Supply disruption due to adverse weather: Supply conditions was disrupted and kept the availability tight at portside in Australia. Additionally, muted Chinese participation during Lunar New Year reduced global demand pressure, further softening sentiment and reducing urgency among Indian buyers.

Shift toward diversified sourcing: The decline in Australian volumes, alongside increased imports from the US, Russia, and Mozambique, indicates a gradual shift away from single-origin dependence, allowing buyers to remain flexible and opportunistic amid volatile pricing.

Imports from Australia drop 28%

Australia remained the largest supplier, but shipments declined sharply to 1.9 mnt from 2.7 mnt, reflecting reduced reliance at higher prices.

Meanwhile, US and Russia volumes increased to 0.9 mnt each, while Mozambique rose to 0.5 mnt, highlighting diversification in sourcing. Canada declined to 0.1 mnt, while Indonesia remained stable.

Top buyers

SAIL increased imports to 1.1 mnt (vs 0.9 mnt), while JSW Steel remained stable at 1.1 mnt, indicating selective procurement.

In contrast, Tata Steel reduced imports sharply to 0.4 mnt from 0.9 mnt, emerging as the key driver of the overall decline.

Other buyers largely maintained stable or marginally higher volumes, with Bengal Energy increasing to 0.3 mnt, indicating opportunistic buying amid softening sentiment.

Overall sentiment in February remained cautious and price-sensitive, with buyers balancing high price levels against expectations of correction. The market shifted from restocking-led demand in January to optimisation-driven procurement, resulting in lower import volumes despite stable underlying steel demand.

Leave a Reply