- Global petcoke prices surge; US FOB crosses $100/t

- Trade activity slows as buyers resist high prices

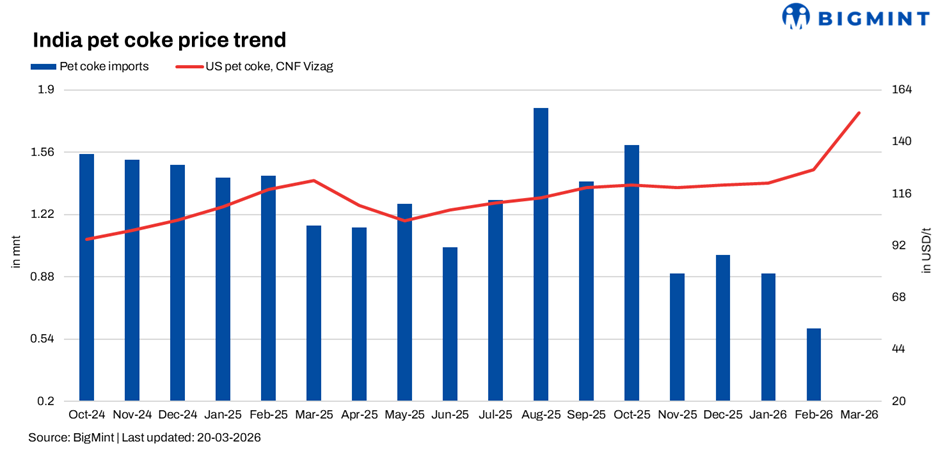

The global petroleum coke market has moved sharply higher over the past two weeks, with prices rising across all major regions and grades. US Gulf Coast high-sulphur coke (6.5%) has crossed $100/t FOB, while delivered prices into key consuming markets such as India and China have moved into the $150/t range.

In India, the rally has been particularly visible. Delivered prices for 6.5% sulphur coke have risen to around $160-165/t CFR, with some offers for prompt cargoes heard even higher. Domestic prices have also followed, with refiners increasing prices multiple times within March, pushing levels above ₹17,000/t.

Despite this strength, actual trading activity has remained muted. Buyers have been reluctant to commit at higher price levels, leading to a widening gap between bids and offers. In several markets, including India and Turkey, consumers are either delaying purchases or turning to alternative fuels.

The current global price structure reflects this divergence:

This pricing environment highlights a market that is firm on paper but increasingly challenged in terms of liquidity and demand.

Supply shock, freight inflation and fuel substitution

The primary driver of the current rally is the disruption caused by the Middle East crisis. Supply from key refining hubs in Saudi Arabia has been affected, particularly from facilities reliant on shipping routes through the Strait of Hormuz. Vessel hesitancy, rerouting, and outright disruptions have reduced the availability of seaborne petcoke into Asia.

At the same time, freight has emerged as a critical factor. Higher crude prices have pushed up bunker fuel costs, while war-risk premiums and operational disruptions have tightened vessel availability. Freight from the US Gulf to India has been hovering around $48-51/t, significantly increasing delivered costs and pushing CFR prices higher even where FOB values have moved more gradually.

Refiners are responding by prioritising margins. US refiners continue to push FOB prices higher, while Indian refiners have raised domestic prices proactively, partly to reflect rising import parity levels and partly to manage demand in a tight market. There is little incentive for refiners to chase volumes in the current environment.

Consumers, particularly in the cement sector, are reacting differently. Faced with rising prices, many are stepping back from the market. Buying activity has slowed, inventories are being drawn down, and procurement strategies are being reassessed. A key development has been the increasing shift toward coal, especially US high-CV NAPP coal, which is now competitive with petcoke on a calorific basis.

This substitution is already visible in India, where cement producers are reducing petcoke usage and increasing coal intake, both domestic and imported. In some cases, planned petcoke procurement for the new financial year is being deferred or replaced altogether.

Traders are navigating a difficult market. While prices are rising, liquidity is thin and volatility remains high. Traders are focusing on short-term opportunities, particularly where coal is displacing petcoke, rather than building long positions.

Prices firm but demand risk building

The petroleum coke market is now at a critical point. Prices remain firm, supported by supply disruptions and rising freight costs, but demand is beginning to show signs of strain.

The key risk to the market is substitution. As petcoke prices move higher relative to coal, especially on a calorific basis, consumers are increasingly willing to switch fuels. This is particularly evident in price-sensitive markets such as India, where the ability to substitute between coal and petcoke is relatively high.

At the same time, supply remains constrained. Disruptions in the Middle East, combined with limited flexibility from US and other exporters, mean that the market is unlikely to see a rapid increase in availability. Freight constraints are further amplifying this tightness, keeping delivered prices elevated.

In the near term, the market is likely to remain firm but volatile. Prices may continue to find support from supply-side factors, but demand destruction and fuel switching will act as a counterbalance.

The next phase of the market will depend on how long the current disruptions persist. If freight remains elevated and Middle East supply continues to be constrained, petcoke prices could stay high. However, if coal continues to gain ground as a substitute fuel, the market may struggle to sustain current price levels.

In this environment, petroleum coke is no longer the default fuel of choice. It is increasingly being priced against coal – and that competition is now shaping the direction of the market.

Leave a Reply