- Weak buying interest amid bunker volatility, geopolitical uncertainty

- Active Australian miners support freight rates through steady fixtures

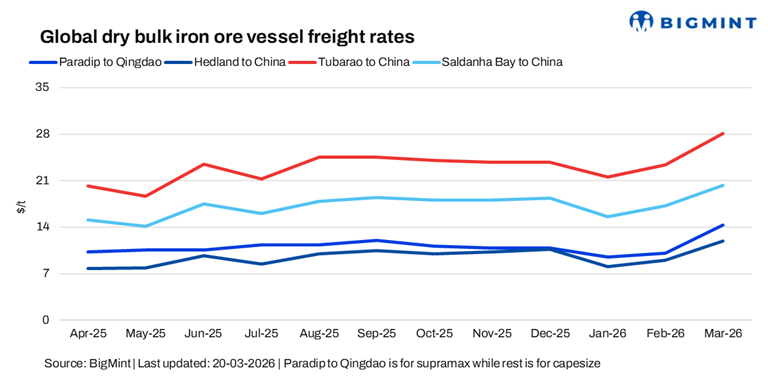

The iron ore freight market showed a mixed picture, with Brazil-China strength supporting sentiment while Pacific routes stayed under pressure amid ample tonnage and cautious demand. Activity was measured as participants stayed watchful amid bunker volatility.

A source informed BigMint: “Capesize and Supramax are showing slight softness, while Panamax remains firm and Handysize largely unchanged. Overall sentiment stays positive, though buyers remain cautious and show limited appetite to engage at current offer levels.”

Route-wise updates

Market highlights

- DCE iron ore futures gain w-o-w: Iron ore futures on the Dalian Commodity Exchange gained by around RMB 17.5/t ($2.54/t) w-o-w to RMB 815.5/t ($118.18/t) on 20 March, supported by improved steel demand expectations in China, restocking activity at mills, and tighter near-term supply from key exporters.

- Baltic index rises w-o-w: The Baltic Index rose 85 points w-o-w to 2,057 on 19 March, supported by stronger Capesize earnings on firm iron ore demand and tighter Atlantic tonnage. Capesize gained 244 points to 2,965 on improved fixtures, while Supramax fell 61 points to 1,229 amid weak minor bulk demand.

- Brent crude futures rise w-o-w: Brent crude oil futures rose by about $8.22/bbl w-o-w to $107.20/bbl (April 2026 contract) on 20 March, driven by escalating Middle East tensions, concerns over potential supply disruptions, and renewed volatility in global energy markets.

- Bunker price volatility: Prices declined by $201/t w-o-w to $1,003/t on 20 March, but remained highly volatile through the week, driven by sharp crude oil fluctuations amid escalating Middle East tensions, supply uncertainty, and cautious market sentiment.

Outlook

Freight rates are likely to edge lower in the near term as ample vessel supply in the Pacific and cautious chartering activity continue to weigh on sentiment. However, uncertainty persists amid ongoing geopolitical tensions and volatile bunker prices, which may lead to sudden shifts in market direction.

Leave a Reply