-

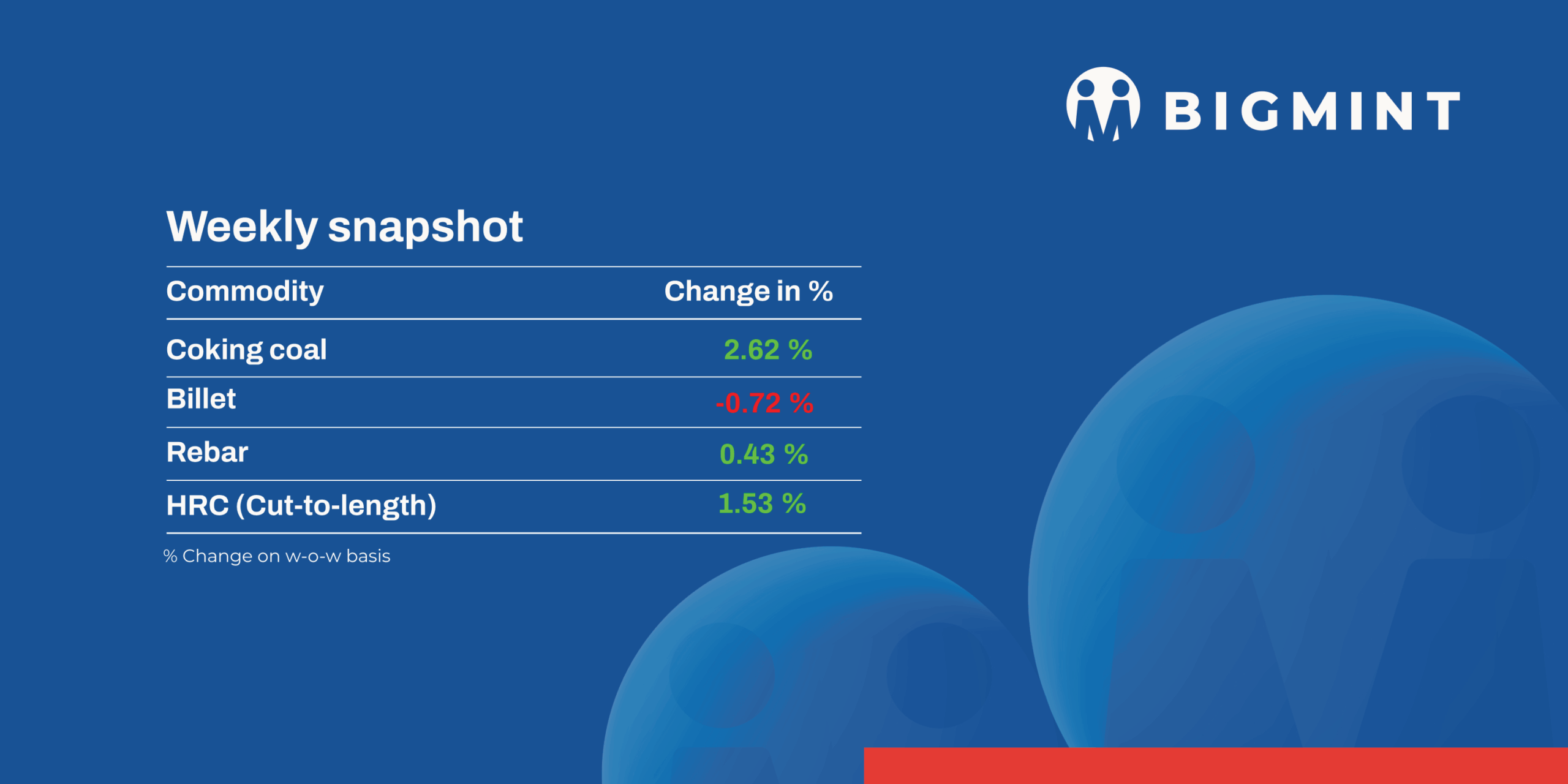

Coking coal prices edge up, iron ore firms up

-

Supply tightness, geopolitical tensions affect market

Steel prices in the domestic market showed mixed trends this week, while semi-finished steel prices edged down. Raw material, such as iron ore, prices firmed on tight supply, while flat steel prices rose on bullish sentiment.

Iron ore and pellet

- In OMC’s iron ore fines auction for 2.04 mnt (Fe 51-65%) on 19 March, around 1.677 mnt (82%) was booked at INR 2,800-6,150/t ex-mines. The majority of the lots received premiums of INR 400-1,000/t. Meanwhile, weighted average bids rose by INR 150/t m-o-m. The lack of offers and limited availability of ore in the merchant market, along with miners’ EC expiration and the hike in steel prices, led to bids rising in the auction.

- In OMC’s auction for 1.57 mnt of iron ore lumps (Fe 60-65%) on 19 Mar’26, 100% material was booked at INR 5,750-7,350/t, with premiums upto 32% over base prices. Weighted average bids rose by INR 50/t m-o-m. Earlier, OMC had lowered the base prices of lumps by INR 50-600/t. The auction witnessed strong demand due to the nearing expiry of some private miners’ ECs, which could tighten supply in March.

- BigMint’s bi-weekly Indian low-grade iron ore fines (Fe 57%) export index increased by $0.5/t w-o-w to $62/t FOB east coast on 19 March against 12 March. However, rising vessel freights and ongoing geopolitical tensions continued to slow down trade and pressure exporter margins, keeping overall market sentiment cautious.

Coal

- South African thermal coal prices at Indian ports declined w-o-w after a sharp rally, with exw-Paradip RB2 (5,500 NAR) falling to around INR 11,800/t and RB3 (4,800 NAR) to INR 10,500/t. The correction was driven by buyer resistance at elevated levels, leading to softer sentiment. However, tight portside availability and lower inventories continue to provide underlying support, keeping the market balanced despite limited trade activity.

- Coal India Limited (CIL) announced a marginal revision in modulated coal prices for the Non-Regulated Sector (NRS), effective 1 April, based on WPI indexation. WPI increased by 0.96% y-o-y, translating into a limited 0.24% price impact after applying the 25% cap. As a result, prices across grades remain largely stable with minor upward revisions, while higher-grade coal will continue to see structured increments. The revision ensures price stability, with modulated prices serving as the base for auctions and e-auctions.

- Metallurgical coke prices in India remained stable w-o-w, with BF-grade coke at INR 35,000/t ex-Jajpur and INR 31,000/t ex-Gandhidham. Foundry coke held at INR 36,000/t ex-Rajkot. Weak steel demand and cautious buying kept activity subdued, while firm coking coal prices at $222/t FOB Australia and import parity near $281/t CFR India continued to support price levels.

- US-origin NAPP thermal coal prices moved higher, with deals concluded at $145-146/t CFR India for April-May shipments. Stronger global benchmarks and rising freight of around $48/t supported delivered prices, while FOB offers stood near $115/t. Improved fuel economics versus petcoke and tight availability kept demand firm, although buying remained selective at elevated price levels.

Ferrous Scrap

- Imported scrap sentiment in India remained on the higher side throughout the week, although trading activity stayed limited as buyers resisted elevated offers amid weak steel demand and financial year-end slowdown. UK/EU-origin HMS 80:20 was heard around $365/t CFR, while shredded scrap was indicated near $375-380/t, with bids continuing to trail offers.

- Supply conditions remained tight due to reduced scrap generation amid gas-related disruptions and a slowdown in domestic industrial activity, while halted Iranian HBI flows further constraining availability. At the same time, a stronger dollar and higher freight rates increased landed costs, prompting sellers to divert cargoes to more active markets like Bangladesh and Pakistan.

- In the last seven days, around 2,500-3,500 t of imported scrap arrived in India, including 1,500 t of HMS 80:20 and 1000 t of turnings/borings from Thailand at $325-330/t CFR Chennai.

Ferro Alloys

- Silico Manganese: Indian silico manganese (60-14) prices went up slightly INR 325/t ($43/t) w-o-w to INR 73,300 -74,500/t ($786-799/t ) across Durgapur, Raipur, Vizag, and Raigarh. The increase was supported by higher-priced deals being accepted in the market, while sellers remained firm in negotiations, offering limited margins on material.

- Ferro Manganese: Indian ferro manganese (70%) prices rose this week, increasing by INR 300/t to INR 74,500/t in Raipur and by INR 400/t to INR 74,500/t in Durgapur. The uptick was supported by elevated manganese ore costs, steady demand from the steel sector, tight supply conditions, and overall firm market sentiment.

- Ferro Chrome: Indian high-carbon ferro chrome (HC 60%, Si 4%) prices dipped slightly by INR 1,100/t ($12/t) to INR 118,700/t ($1,272/t) exw Jajpur. Prices fell due to bid-offers gaps and decreasing bids in OMC’s chrome ore auction.

- Additionally, At OMC’s chrome ore auction today, 67,500 t was sold out of 104,300 t offered. Bids edged down slightly by 1-2% (INR 195-529/t) m-o-m for almost all the grades.

Semi Finished

- India’s semi-finished steel market witnessed a downward trend this week. Domestic billet prices declined by INR 100-700/t ($1-7/t) w-o-w across key regions. However, north India recorded slight gains, supported by tighter material availability and region-specific demand variations. Overall buying interest remained subdued, while limited bookings in the finished steel segment spilled over and weighed on demand for semi-finished steel.

- The sponge iron market reflected mixed sentiments as uneven demand and variations in booking patterns kept market conditions volatile. Pan-India sponge iron prices fell by INR 50-700/t ($0.5-7/t) w-o-w across major regions. In contrast, Mandi Gobindgarh, Durgapur, and Chennai registered price increases of INR 100-400/t ($1-4/t), supported by a slight improvement in bookings at varied price levels.

- On the export front, DRI offers remained firm during the week. Export offers to Nepal eased marginally by $2/t w-o-w to $345/t CPT Raxaul, while offers to Bangladesh held steady at $355/t CPT Benapole. As substantial bookings were already concluded last week at prevailing price levels, buyers refrained from fresh bookings. Additionally, buying interest from Bangladesh remained muted amid Eid-related market slowdown.

Finished Long Steel

- IF-rebar: IF-route rebar prices witnessed a slight decline w-o-w across major Indian markets, reflecting a mild correction. Trading activity remained moderate, with buyers largely continuing need-based procurement and showing resistance at elevated price levels. However, manufacturers maintained higher offer levels, supported by underlying cost pressures, while offering competitive discounts to sustain sales momentum. Despite the recent softening, market dynamics are evolving rapidly amid ongoing geopolitical tensions and elevated raw material and energy costs. These factors are expected to keep the steel sector supported, with prices likely to maintain a positive trend in the near term.

- On a week-on-week basis, rebar prices softened by INR 100-800/t across key regions. However, Chennai and Raipur witnessed a price uptick of INR 200/t, supported by relatively better demand conditions and localized supply dynamics.

- Trade reference prices of Fe 500 grade rebars manufactured via the IF route (10-25 mm size) were assessed at INR 46,000-46,400/t exw Raipur, INR 51,000-51,700/t exw Jalna.

- Trade reference prices of heavy structural steel for the base size 150 mm channel stood at INR 46,700-47,200/t exw-Raipur.

- BF-rebar: Indian primary steelmakers increased rebar prices by INR 500-1,000/tonne (t) ($5-11/t) during this week, sources informed BigMint. Post-revision, list prices stood at INR 59,500-60,500 /t ($637-648/t) on landed basis.

- Trade-level BF-rebar prices (distributor to dealer) rose by INR 200/t ($2/t) w-o-w to INR 60,000/t ($643/t) exy-Mumbai, as per BigMint’s assessment on 17 March 2026. Buying activities in the BF-rebar trade market have slowed down as buyers are showing limited interest due to surge in prices. Also, they are procuring cautiously due to the higher BF-IF price gap.

In the projects segment, prices hovered at around INR 60,000-61,000 /t ($643-653/t) FOR basis.

Flat steel

-

- Trade-level prices of hot-rolled coils (HRC) and cold-rolled coils (CRC) in India remained on an upward trajectory, supported by bullish market sentiment and supply constraints. HRC prices were assessed in the range of INR 55,250-57,000/t ($598-617/t), while CRC prices stood at INR 63,200-64,250/t ($684-695/t), reflecting recent mill price hikes for mid-March sales.

- Indian trade-level sentiment for HRC and CRC remained bullish this week, driven by geopolitical tensions between Iran and Israel, which increased volatility in global markets. This triggered inventory build-up among traders and distributors amid fears of supply disruptions. Tight material availability, particularly in the northern region, further supported the sharp w-o-w rise in HRC prices, although underlying demand remained moderate.

- On a m-o-m basis, trade-level HRC prices increased by INR 1,500/t ($16/t) to INR 55,300/t ($599/t) in March, compared to INR 53,800/t ($583/t) in February. Similarly, CRC prices rose by INR 1,700/t ($18/t) to INR 61,400/t ($665/t) from INR 59,700/t ($647/t).

India’s bulk imports of HRCs reached 47,025 t as of 13 March, based on vessel line-up data, with an additional 166,902 t expected by late March. Meanwhile, bulk exports stood at 61,000 t, with around 144,000 t of additional cargoes currently in transit.

Leave a Reply